ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

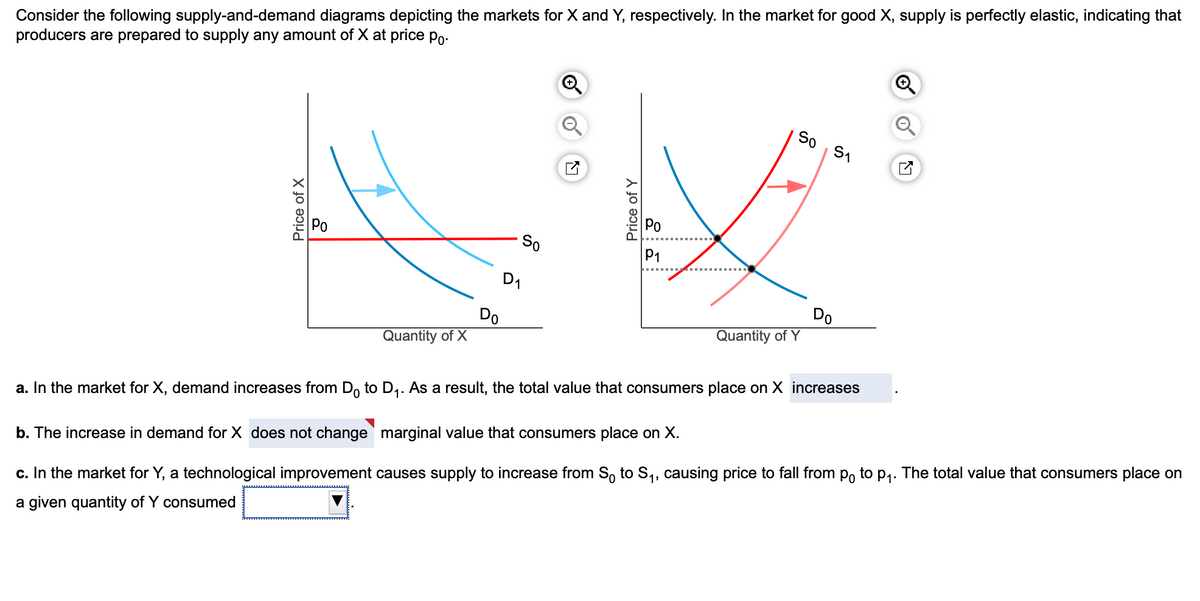

Transcribed Image Text:Consider the following supply-and-demand diagrams depicting the markets for X and Y, respectively. In the market for good X, supply is perfectly elastic, indicating that

producers are prepared to supply any amount of X at price po-

So

Po

So

P1

D1

Do

Quantity of Y

Do

Quantity of X

a. In the market for X, demand increases from Do to D,. As a result, the total value that consumers place on X increases

b. The increase in demand for X does not change marginal value that consumers place on X.

c. In the market for Y, a technological improvement causes supply to increase from So to S4, causing price to fall from p, to p,. The total value that consumers place on

a given quantity of Y consumed

Price of X

Price of Y

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- The diagram illustrates the demand for MQ2020, a luxury car manufactured by MQ Motors Which statement correctly describes the demand for MQ2020? 8,000 Price, P: WTP (5) 6,000 4,800 4,000 3,200 2,000 0 0 40 60 80 100 Quantity, Q: number of consumers per day 120 Select one O a. There are 99 consumers per day who are willing to pay money for MQ2020. O b. If MQ Motors sets the price at $4,800, there will be 60 consumers who are willing to buy MC22020 Oc MQ Motors will need to raise the price up to $8,000 in order to maximise its profit Od. There are 59 consumers who are willing to pay more than $4,800 for MQ2020. Oe. The demand curve shows that points A and C are feasible options for MQ Motors.arrow_forwardHow do i figure this one out?arrow_forwardO X₁ V -IC, IC₂ IC, X₂ B X, X, B, B₂ (a) Are goods X and Y substitutes or complements? Explain. B₂ X (b) Let Y refer to all other goods. Is the demand for good X elastic or inelastic? Explain.arrow_forward

- Suppose that the market demand for Turkey is given by: Q_(T)=2-8P_(T)+2P_(C)+0.0015I Where Q_(T) is annual quantity demanded of turkey in million pounds, P_(T) is the price of turkey per pound, P_(C) is price of chicken per pound, and I is the average household income in dollars per year. a. Find the annual quantity demanded of turkey if the price turkey is $2.00 per pound, price of chicken is $1.50 per pound and the annual household income is $30,000.arrow_forward1. Consider the market for Widgets. Suppose that the equation for the supply curve is: Qs = 1,000P – 10,000, and the equation for the demand curve is: Qa = 50,000 – 2,000P. It turns out that the equilibrium price is 20, while the equilibrium quantity is 10,000. a. Use a 10% increase in quantity to estimate (crudely) both the elasticity of supply and the elasticity of demand at the equilibrium quantity. i) Categorize supply and demand as elastic or inelastic at the equilibrium quantity. ii) Is supply or demand relatively more inelastic at the equilibrium quantity? b. If the government enacted a tax of $3, the loss in consumer surplus would be 9,000, while the loss in producer surplus would be 18,000 (see Homework 2, question #2.) Compare this information to your answer to part (a). Explain. c. Now estimate (crudely) the elasticity of demand at a quantity of 11,000 by decreasing quantity by 1,000. Compare your estimate of elasticity to the estimate in part (a). Comment.arrow_forwardWhen income rises by 10%, the demand for Good A falls by 3%. From the above, we know Good A is O a complement a normal good O an inferior good O a substitutearrow_forward

- i need the answer quicklyarrow_forwardsuppose there is a spring producing 100 gallons of water each day, without cost to smith, who owns the land around the spring. nearby farmers need the water due to a recent drought a.) show the resulting equilibrium b.) what is the price elasticity of demand at the equilibriumarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education