ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Assume the consumers face

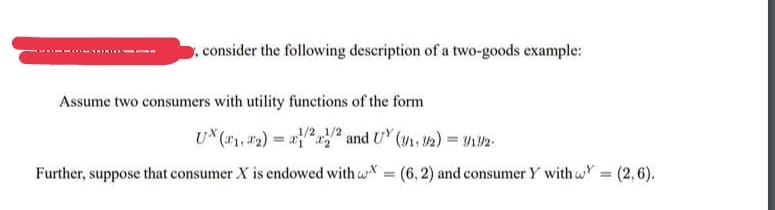

Transcribed Image Text:,consider the following description of a two-goods example:

Assume two consumers with utility functions of the form

U* (*1, #2) = 2r2

and UY (V. 2)

Further, suppose that consumer X is endowed with w = (6, 2) and consumer Y with wY

= (2,6).

Expert Solution

arrow_forward

Step 1

Given,

Consumer X= (6,2)

Consumer Y= (2,6)

prices P = (1, 1)

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose your income is 200, the price of good x is 2, and the price of good y is 3. You know that your utility function is U= 2(xy)^3. (A) What amounts of x and y do you choose? (B) Can you generalize your choices to demand curves for x and y for any prices and income?arrow_forwardFrom the demand function Qdx = 12 – 2Px (Px is given in dollar), derive:(a) the individual’s demand schedule and demand curve, and(b) what is the maximum quantity this individual will ever demand of commodity X per time period?arrow_forwardSuppose the price of good X decreases. The new consumer equilibrium level of good X will be: higher than before the price change. lower than before the price change. indeterminate without more information. the same as before the price change.arrow_forward

- (b) U(x, y) = min [ax, y]arrow_forwardSuppose you have the following indirect utility function: V(Pa, Py, I) = In PxPy What are marshallian demands for x and y? I (a) (9x9y) = (22) (b) (9,9y) = (In, In 2) (c) (9, 9y) = (exp(2p/py), exp(2ppy)) I (d) (9x, gy) = (2pr+py' px+2py) What is the expenditure function for the associated expenditure minimization problem? (a) E(pa, Py, U) = (P + Py) ln(U) (b) E(pa, Py, U) = √exp(U)Papy (c) E(pa, Py, U)= (p²+p²) In(U) (d) E(pa, Py, U) = exp(U)²papy What are the individual's Hicksian demands for goods x and y? (a) (h₂, hy) = ((BU)¹/², (PU) ¹/²) (b) (ha, hy) = (RU, DU) (c) (ha, hy) = ((2 exp(U))¹/², (exp(U))¹/²) -1/2 (d) (hx, hy) = ((P₂PzU)−¹/², (P₂PzU)-¹/2) Are x and y complements or substitutes?arrow_forwardProblem 2 Joan has the following utility function: u(x, y) = 5x + 3y. (a) Find Jane's marshallian demands. (b) Find Jane's hicksian demands. Consider that income is I = $8, and prices are given as p = $4, Py = $2. (c) Does Jane have enough money to attain a utility level of 20? Justify your answer. (d) Assume thè price of y marginally increases. Find the total, income and substitution effect for r due to the change in py.arrow_forward

- Mary has the following utility function: u(x, y) = 3 ln(x) + 2y. Her income is given by I = 10 and the prices originally are p = 1 and py = 2 (b) How much of each good is Mary currently consuming?arrow_forwardConsumer equilibrium exists when: P/MU of all goods is the same MU/P for all goods is the same TU/P for all goods is the same the MU for all goods is the samearrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education