MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

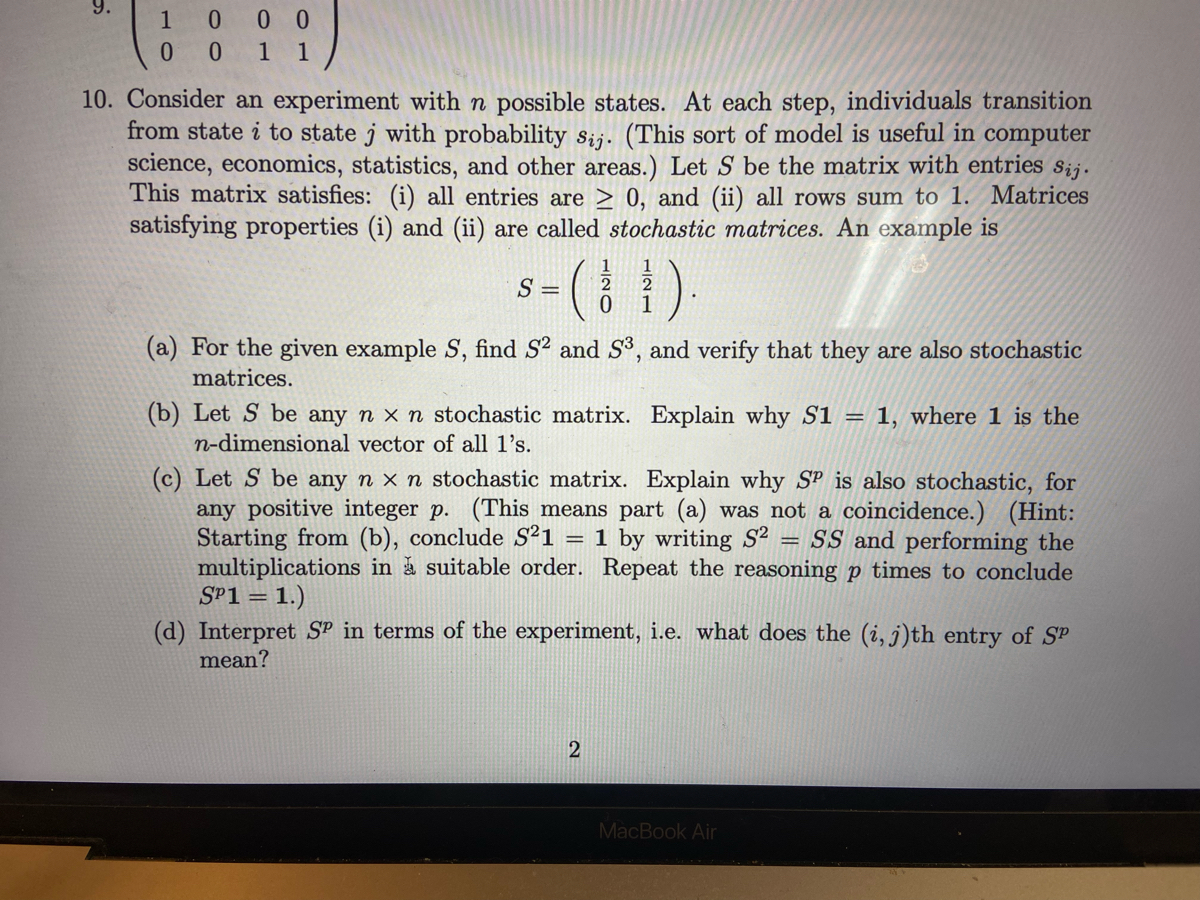

Transcribed Image Text:1

0

000

0 1 1

10. Consider an experiment with n possible states. At each step, individuals transition

from state i to state j with probability sij. (This sort of model is useful in computer

science, economics, statistics, and other areas.) Let S be the matrix with entries sij.

This matrix satisfies: (i) all entries are ≥ 0, and (ii) all rows sum to 1. Matrices

satisfying properties (i) and (ii) are called stochastic matrices. An example is

S =

(

0

(a) For the given example S, find S² and S³, and verify that they are also stochastic

matrices.

Explain why S1 = 1, where 1 is the

(c) Let S be any n x n stochastic matrix. Explain why SP is also stochastic, for

any positive integer p. (This means part (a) was not a coincidence.) (Hint:

Starting from (b), conclude S²1 1 by writing S² = SS and performing the

multiplications in a suitable order. Repeat the reasoning p times to conclude

SP1 = 1.)

=

(b) Let S be any n x n stochastic matrix.

n-dimensional vector of all 1's.

2

2

(d) Interpret SP in terms of the experiment, i.e. what does the (i, j)th entry of SP

mean?

MacBook Air

Expert Solution

arrow_forward

Step 1

Hello! As you have posted more than 3 sub parts, we are answering the first 3 sub-parts. In case you require the unanswered parts also, kindly re-post that parts separately.

10

a.

From the given information,

Consider,

Here, all the entries are >=0 and the sum of the row elements is equal to 1.

That is, the conditions for the stochastic matrix are satisfied.

Hence, the matrix S^2 is also stochastic matrix.

Here, all the entries are >=0 and the sum of the row elements is equal to 1.

That is, the conditions for the stochastic matrix are satisfied.

Hence, the matrix S^3 is also stochastic matrix.

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

- What is the second row of the matrix A, if A is stochastic? Second row: 0.8 The steady state vector for A is If v= 0.5 [15] 26 then Av approaches as n gets large. A = [0.2 ? 0.5] ?arrow_forwardwhat does the equation, d/dt Π = MΠ calculate for where Π is population vector describing the overall state probability distributions and M is a 4x4 transition rate matrix?arrow_forwardLet X Є pxn denote a zero mean observation matrix matrix of obser- vations, P be a pxp orthogonal matrix, and Y = PTX. (a) Show that if C is the covariance matrix of X then PTCP is the co- variance matrix of Y = PT CP. (b) It can be verified that tr (FG) = tr (GF) for any two n x n matrices F and G. Use this fact to show that the total variance of the data in Y is equal to the total variance of the data in X.arrow_forward

- 7arrow_forwardAn investor is developing a portfolio of stocks. She has identified 3 stocks in which to invest. She wants to earn at least 11% return but with minimum risk. The average return for the stocks is: Annual Return A Average 10.72% 10.68% 11.87% The covariance matrix for the stocks is: A A 0.00009 -0.00009 -0.00011 -0.00009 0.00032 -0.00007 -0.00011 -0.00007 0.00122 Formulate the NLP for this problem by writing the decision variables, objective function and constraints.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman