ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Plz answer a and b

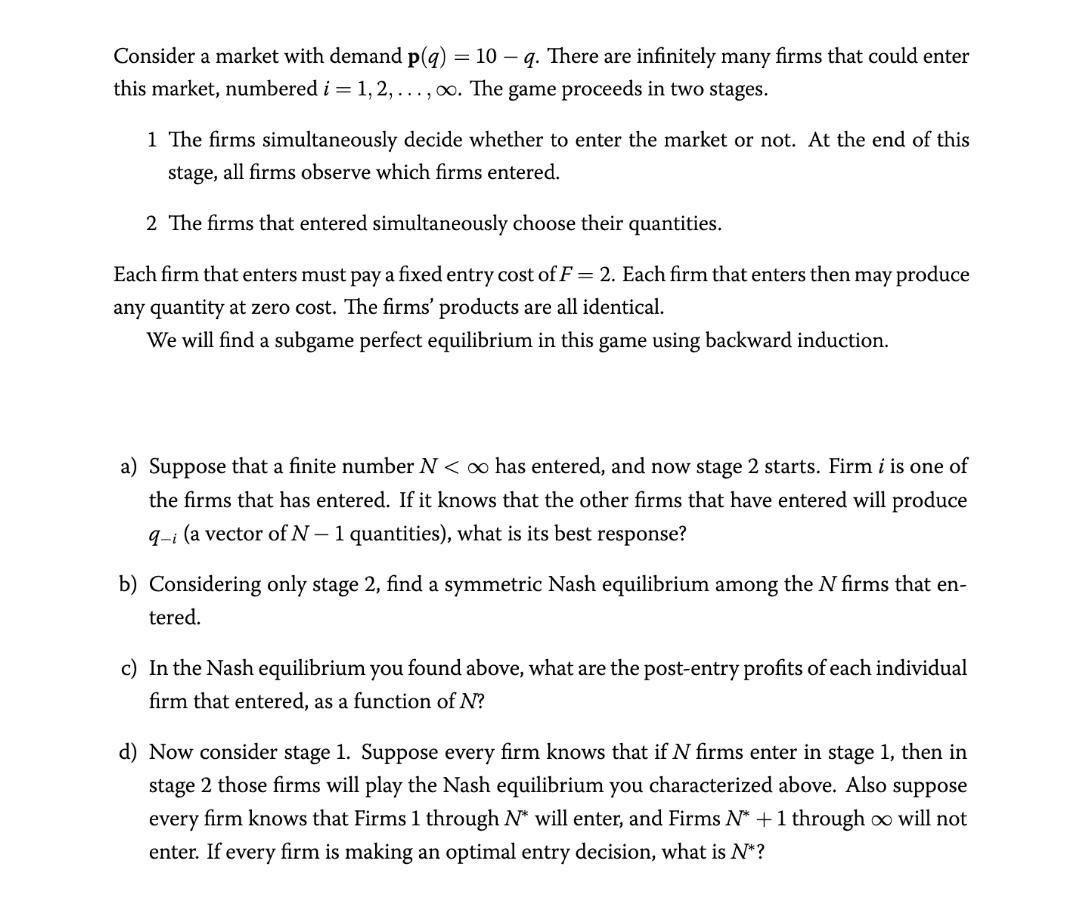

Transcribed Image Text:= 10 – q. There are infinitely many firms that could enter

Consider a market with demand p(g)

this market, numbered i = 1, 2,..., o. The game proceeds in two stages.

1 The firms simultaneously decide whether to enter the market or not. At the end of this

stage, all firms observe which firms entered.

2 The firms that entered simultaneously choose their quantities.

Each firm that enters must pay a fixed entry cost of F = 2. Each firm that enters then may produce

any quantity at zero cost. The firms' products are all identical.

We will find a subgame perfect equilibrium in this game using backward induction.

a) Suppose that a finite number N< o has entered, and now stage 2 starts. Firm i is one of

the firms that has entered. If it knows that the other firms that have entered will produce

q-i (a vector of N-1 quantities), what is its best response?

b) Considering only stage 2, find a symmetric Nash equilibrium among the N firms that en-

tered.

c) In the Nash equilibrium you found above, what are the post-entry profits of each individual

firm that entered, as a function of N?

d) Now consider stage 1. Suppose every firm knows that if N firms enter in stage 1, then in

stage 2 those firms will play the Nash equilibrium you characterized above. Also suppose

every firm knows that Firms 1 through N* will enter, and Firms N* +1 through oo will not

enter. If every firm is making an optimal entry decision, what is N*?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Please no written by hand and no emagearrow_forwardquestion part c should contain a grapharrow_forwardA doctor's office staff studied the waiting times for patients who arrive at the office with a request for emergency service. The following data with waiting times in minutes were collected over a one- month period. a. Fill in the frequency values below. Waiting Time Frequency 49 11 16 4 2 3 18 11 7 9 8 12 24 7 8 7 13 19 5 4 0-4 5-9 8 4 10-14 15-19 3 20-24 1 Total 20 b. Fill in the relative frequency (2 decimals) values below. Waiting Time Relative Frequency 0.2 0-4 5-9 0.4 0.2 10-14 15-19 0.15 20-24 0.05 Total 1arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education