FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

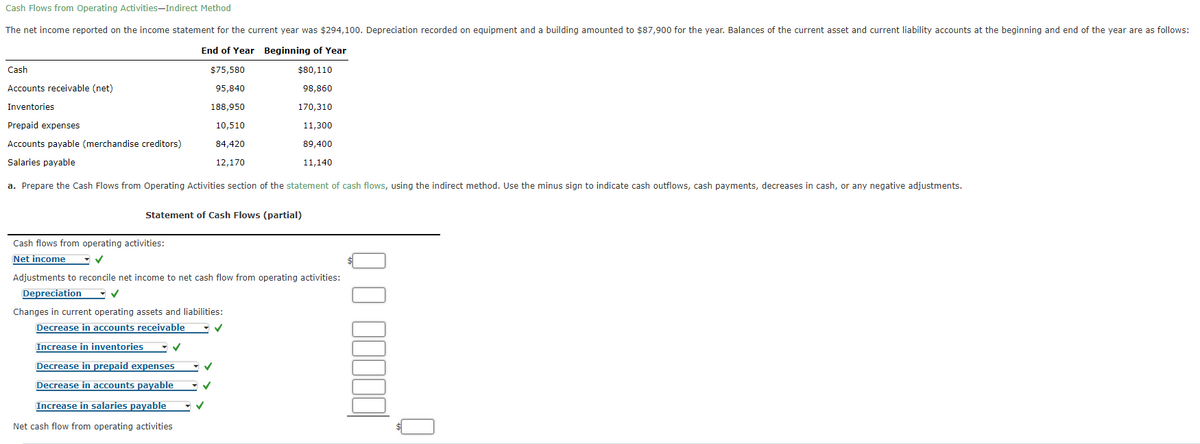

Transcribed Image Text:Cash Flows from Operating Activities-Indirect Method

The net income reported on the income statement for the current year was $294,100. Depreciation recorded on equipment and a building amounted to $87,900 for the year. Balances of the current asset and current liability accounts at the beginning and end of the year are as follows:

End of Year Beginning of Year

Cash

$75,580

$80,110

Accounts receivable (net)

95,840

98,860

Inventories

188,950

170,310

Prepaid expenses

10,510

11,300

Accounts payable (merchandise creditors)

84,420

89,400

Salaries payable

12,170

11,140

a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments.

Statement of Cash Flows (partial)

Cash flows from operating activities:

Net income

Adjustments to reconcile net income to net cash flow from operating activities:

Depreciation

Changes in current operating assets and liabilities:

Decrease in accounts receivable

Increase in inventories

Decrease in prepaid expenses

Decrease in accounts payable

Increase in salaries payable

Net cash flow from operating activities

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Reporting changes in Equipment on Statement of Cash Flows An analysis of the general ledger accounts indicates that office equipment, which cost $202,500 and on which accumulated depreciation totaled $84,375 on the date of sale, was sold for $101,250 during the year. Using this information, indicate the items to be reported on the statement of cash flows. Transaction Section of Statement of Cash Flows Added or Deducted $202,500 cost of office equipment $84,375 accumulated depreciation $101,250 sales price $16,875 loss on sale of equipment (assume the indirect method is used)arrow_forward14arrow_forwardRequired information [The following information applies to the questions displayed below.] Lansing Company's current-year income statement and selected balance sheet data at December 31 of the current and prior years follow. LANSING COMPANY Income Statement For Current Year Ended December 31 Sales revenue Expenses Cost of goods sold Depreciation expense Salaries expense Rent expense Insurance expense Interest expense Utilities expense Net income At December 31 Accounts receivable $ 97,200 LANSING COMPANY Selected Balance Sheet Accounts Current Year $ 5,600 1,980 4,400 880 220 260 220 Inventory Accounts payable Salaries payable Utilities payable Prepaid insurance Prepaid rent 42,000 12,000 18,000 9,000 3,800 3,600 2,800 $ 6,000 Prior Year $ 5,800 1,540 4,600 700 160 280 180arrow_forward

- Exercise 16 - 5 (Algo) Indirect: Cash flows from operating activities LO P2SFitz Company reports the following information.Selected Annual Income Statement DataNet incomeDepreciation expenseAmortization expenseGain on sale of plant assetsSelected Year - End Balance Sheet Data$ 376,000 Accounts receivable decrease 44,200 Inventory decrease 7,300 Prepaid expenses increase6, 100 Accounts payable decreaseSalaries payable increase$ 122, 40042, 5005, 8008, 8002, 400Use the indirect method to prepare the operating activities section of its statement of cash flows for the year endedarrow_forwardPrint Item Cash Flows from Operating Activities—Indirect Method The net income reported on the income statement for the current year was $149,000. Depreciation recorded on store equipment for the year amounted to $24,600. Balances of the current asset and current liability accounts at the beginning and end of the year are as follows: End of Year Beginning of Year Cash $58,710 $53,430 Accounts receivable (net) 42,100 39,480 Merchandise inventory 57,480 60,110 Prepaid expenses 6,460 5,080 Accounts payable (merchandise creditors) 55,010 50,540 Wages payable 30,060 33,020 a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. Statement of Cash Flows (partial) Cash flows from operating activities: $ Adjustments to reconcile net income to…arrow_forwardCash Flows from Operating Activities—Indirect Method The income statement disclosed the following items for year: Depreciation expense $36,900 Gain on disposal of equipment 21,510 Net income 222,200 The changes in the current asset and liability accounts for the year are as follows: Increase(Decrease) Accounts receivable $5,740 Inventory (3,270) Prepaid insurance (1,230) Accounts payable (3,890) Income taxes payable 1,230 Dividends payable 860 a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash out flows, cash payments, decreases in cash, or any negative adjustments. Statement of Cash Flows (partial) For the year ended xxx Cash flows from operating activities: Net income $fill in the blank edc573f62020fa6_2 Adjustments to reconcile net income to net cash flow from operating activities: Depreciation fill in the blank…arrow_forward

- it is about constructing cash flow statement using indirect method, how is it get the 45? And please explain the calculation.arrow_forwardCash Flows from Operating Activities—Indirect Method Selected data derived from the income statement and balance sheet of National Beverage Co. for a recent year are as follows: Income statement data (in thousands): Net income $149,774 Loss on disposal of property (149) Depreciation expense 13,226 Other items involving noncash expense 837 Balance sheet data (in thousands): Increase in accounts receivanle 13,041 Increase in inventory 7,565 Increase in prepaid expense 10,548 Increase in accounts payable and other current liabilities 17,464 a. Prepare the Cash Flows from (used for) Operating Activities section of the statement of cash flows, using the indirect method for National Beverage Co. Use the minus sign to indicate cash out flows, cash payments, decreases in cash, or any negative adjustments. Enter the amounts in thousands of dollars, as shown above. National Beverage Co. Cash Flows from Operating Activities (in thousands) Cash flows…arrow_forwardtermining Net Income from Net Cash Flow from Operating Activities Curwen Inc. reported net cash flow from operating activities of $216,400 on its statement of cash flows for the year ended December 31. The following information was reported in the “Cash flows from operating activities” section of the statement of cash flows, using the indirect method: Decrease in income taxes payable $4,200 Decrease in inventories 10,400 Depreciation 16,000 Gain on sale of investments 7,200 Increase in accounts payable 2,900 Increase in prepaid expenses 1,800 Increase in accounts receivable 7,800 a. Determine the net income reported by Curwen Inc. for the year ended December 31.$fill in the blank 1 b. Curwen’s net income is different than net cash flow from operating activities. Which of the following could possibly be the reason for such difference? Because depreciation expense which has no effect on cash flows from operating activities. Changes in current operating assets and…arrow_forward

- Fitz Company reports the following information. Selected Annual Income Statement Data Net income Depreciation expense Amortization expense Gain on sale of plant assets Cash flows from operating activities Selected Year-End Balance Sheet Data $373,000 Accounts receivable decrease 45,600 Inventory decrease 7,900 Prepaid expenses increase 6,400 Accounts payable decrease Salaries payable increase Use the indirect method to prepare the operating activities section of its statement of cash flows for the year ended December 31. Note: Amounts to be deducted should be indicated with a minus sign. Statement of Cash Flows (partial) Changes in current operating assets and liabilities Adjustments to reconcile net income to net cash provided by operating activities Income statement items not affecting cash $ 95,500 46,000 5,900 9,500 1,900arrow_forwardssarrow_forwardCash Flows from (Used for) Operating Activities The income statement disclosed the following items for the year: Depreciation expense Gain on disposal of equipment Net income The changes in the current asset and liability accounts for the year are as follows: Accounts receivable Inventory Prepaid insurance Accounts payable Income taxes payable Dividends payable Increase (Decrease) $5,190 (2,950) (1,110) (3,520) 1,110 780 $33,300 19,440 225,100 a. Prepare the Cash Flows from (used for) Operating Activities section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. Statement of Cash Flows (partial) Cash flows from (used for) operating activities: 27 Adjustments to reconcile net income to net cash flows from (used for) operating activities: Changes in current operating assets and liabilities: Net cash flows from operating activities b. Why is net cash flows from operating…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education