ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

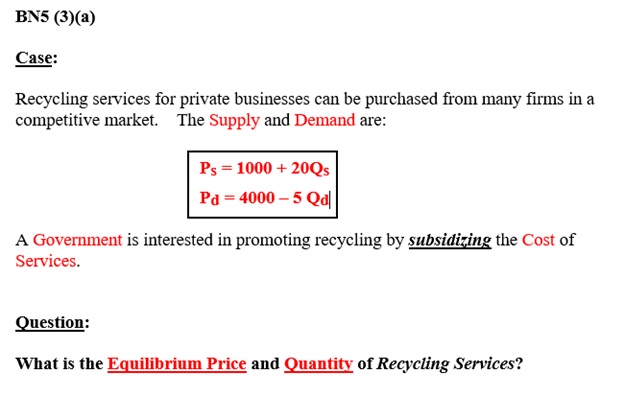

Transcribed Image Text:BN5 (3) (a)

Case:

Recycling services for private businesses can be purchased from many firms in a

competitive market. The Supply and Demand are:

Ps = 1000 + 20Qs

Pd=4000-5 Qal

A Government is interested in promoting recycling by subsidizing the Cost of

Services.

Question:

What is the Equilibrium Price and Quantity of Recycling Services?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- CON101 section(2,3 &5)Dr. Abdulhadi Ibrahim / Bonus Quiz (Section 5) 8am Market failure can be caused by of Select one: tion O a. government intervention and price controls O b. externalities and market power O c. high prices and foreign competition O d. low consumer demandarrow_forwardWk 2 - Apply: Market Dynamics and Efficiency [due Day 7] 6 Help Save & Exit Saved Submlt $ Price S $ Price S2 S2 7 E2 E1 P=P2 ---------- E, P=P2 F------X- D2 D. polnts \D Q2 Q Quantity Graph (1) Quantity Graph (2) eBook $ Price $ Price S2 References P. KE, P. --XE, P D1 'D- P2F------- KE2 ------ D2 Q=Q2 Q=Q2 Quantity Quantity Graph (4) Rectangular Snip Graph (3) Select the graph that best shows the changes In demand and supply In the beef market If a new diet fad favoring beef consumptlon becomes hugely popular, while cattle producers see steeply rising costs of cattle feed. Multiple Choice graph (1) graph (2) graph (3) graph (4)arrow_forwardimg' (a If po increases, what happens to the demand and supply of public transportation (shifts left/shifts right/doesn’t change) What happens to the equilibrium quantity and price for public transportation? (increase/decrease) (b)At a given price p, as oil becomes more expensive (po increases), does the (own) price elasticity of demand for public transportation increase / decrease / stay the same? (c) Calculate the cross-price elasticity of public transportation demand with respect to the oil price po, at the point p = 1 and po = 2. Are the two goods (public transportation and oil) substitutes or complements, or unrelated?arrow_forward

- (a). Identify and distinguish the functions of price. (b). what is price legislation? (c). Explain the condition under which price legislation is employed in an economy. using diagrams, show the relevance of price elasticity of demand in business pricing strategiesarrow_forwardGRAPH ($) Price 90 $90.00 80 70 60 50 $50.00 40 30 20 10 Surplus Measures off SETTINGS S Tax imposed on: Supply Demand Excise Tax (0-$20) Demand Perfectly Inelastic Supply 0.00 Reset Relatively Elastic Relatively Elastic Elastic Perfectly Elastic Perfectly stic D CALCULATIONS 0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 19.0 Quantity (thousands per week) Price Paid Quantity No Tax $50.00 4,000 With Tax $50.00 4,000arrow_forwardDue to a sales tax, the sale of gameboys decrease from 80 to 70. This tax is a tax on sellers when they receive the units from suppliers. How would the curve look due to this change?arrow_forward

- apter 16 Problems LO ? eBook Refer the figure given below to answer the question. ¹2 Wage rate ($ per hour) 9 8 7 6 LD 5 Mc Graw Hill Type here to search 4 M 3 2 1 0 S₁ D 10 20 30 40 40 50 60 70 80 90 100 O ○ 발 Number of people employed (in millions) Tools 7 dropline 2 O **********arrow_forwardPlease let me know seftuon A) if the input price would rise or fallarrow_forwardSOME S&D PROBLEMS 1. A. Find Pe and Qe Price per unit (dollar 8 8 2 2 2 2 2 2 2 2 100 90 80 70 60 50 40 30 20 10 0 200 400 600 Quantity B. What is the effect of a ceiling price of $40? 800 Do 1,000arrow_forward

- 1. Suppose market demand for gasoline is given by QD = 60-2P where QD is quantity demanded and P is the market price. Market supply is given by Qs = 4P where Qs is quantity supplied and P is the market price. (a) Find the equilibrium price and quantity in this market. (b) What is the consumer surplus and producer surplus? (c) Suppose that the government imposes a $3 tax on the good, to be included in the posted price (i.e. tax paid by suppliers). What is new equilibrium posted price? How much of that price do producers keep? What is the new market equilibrium quantity? What is the change in surplus for consumers? What is the change in surplus for producers?arrow_forwarddo fastarrow_forwardNote:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism.Answer completely.You will get up vote for sure.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education