ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

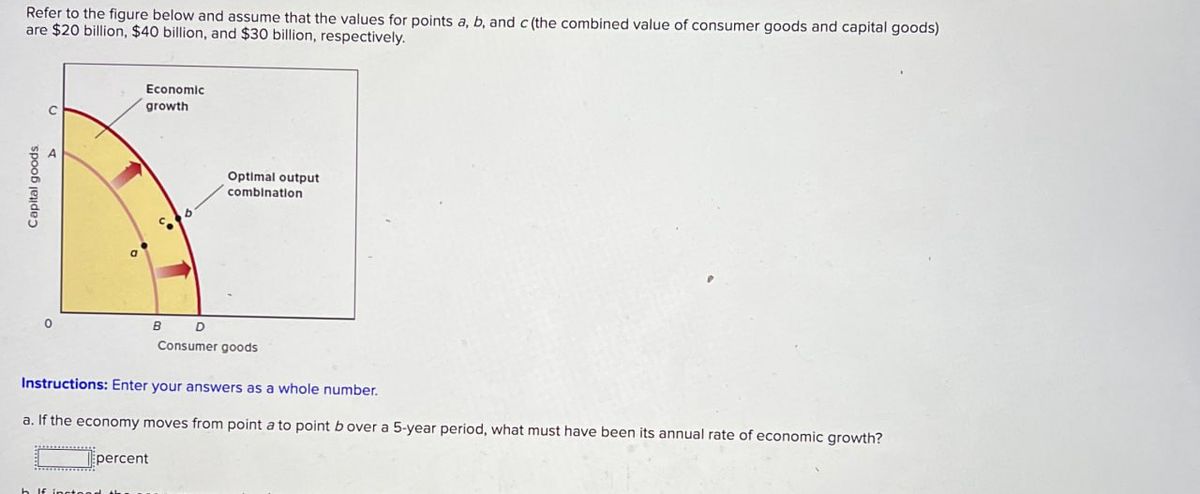

Transcribed Image Text:Capital goods.

Refer to the figure below and assume that the values for points a, b, and c (the combined value of consumer goods and capital goods)

are $20 billion, $40 billion, and $30 billion, respectively.

Economic

growth

B

D

Optimal output

combination

Consumer goods

Instructions: Enter your answers as a whole number.

a. If the economy moves from point a to point b over a 5-year period, what must have been its annual rate of economic growth?

percent

b If inste

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- 1. Many endogenous growth models feature so called scale effects: per capita growth rises when population growth rises. Some economists have criticized these models for this reason, since countries with faster population growth do not in general appear to also experience faster per capita income growth. Consider an economy that has access to a production technology Y = AKª L¹-a where Y is output, A is the level of technology, K is capital and L is the amount of labor in the economy. Capital evolves according to K = SY (thus, the depreciation rate 6 = 0). The population growth rate is n. (Throughout, gx, where x can be any of the variables in the model). i. Assume that technology is determined by A =BK What sort of endogenous growth model is this? Find gk in terms of the K, L, and other parameters of the model. ii. Write an expression for gy in terms of gk and g₁. What must be true for a balanced growth path to exist in this model? Solve for the balanced growth path value of gy and gy,…arrow_forwardA. Investment in "infrastructure" represents spending on: O roads, bridges, canals, etc. O human capital (education) O government institutions O innovation to physical capital B. Which of the following was not one of Thomas Malthus' assumptions regarding population and economic growth? O Per-capita income would increase. O The economy was agriculturally based O The supply of land was fixed O The population would continue to increasearrow_forwardQuestion 7 What is meant by economic growth and why is it one of the most important goals macroeconomists seek to achieve? In your explanation, show the relationship between production, consumption, and investment in periods of economic growth?arrow_forward

- QUESTION 28 1. Production Possibilities (alternatives) A B с D Capital goods Consumer goods E 5 0 F 4 5 3 2 9 Is unobtainable in this economy 1 0 12 14 15 Refer to the above table. A total output of 3 units of capital and 4 units of consumer goods: Would involve an inefficient use of the economy's scarce resources Will result in the maximum rate of growth available to this economy Is irrelevant because the economy is capable of producing a larger total outputarrow_forwardOne of the classic theories of economic growth is Rostow’s Stages of economic growth. Use the article, The Stages of Economic Growth to summarise the four stages outlined by Rostow and how they develop on each other.arrow_forwardBased on article "Technology and economic growth: From Robert Solow to Paul Romer" by Rui Zhao, Romer has successfully opened the black box and explained how technology can be produced by an economy without having to rely on external (exogenous) technology. Using the central equations of the Romer’s model, technology (At) can grow to At + 1 due to efforts in R&D and technology spillover. Explain the role of three key sectors in the economy to drive technological-based economic growth.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education