Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

{kind=link}

Concept explainers

Question

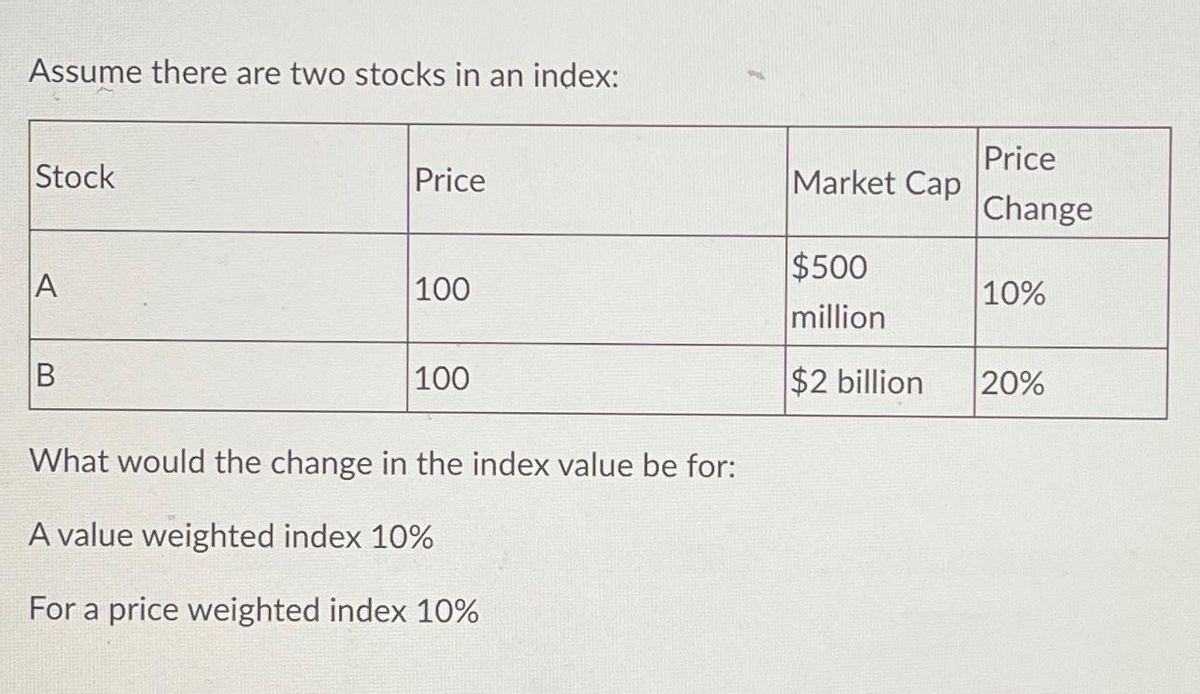

Transcribed Image Text:Assume there are two stocks in an index:

Stock

A

B

Price

100

100

What would the change in the index value be for:

A value weighted index 10%

For a price weighted index 10%

Market Cap

$500

million

$2 billion

Price

Change

10%

20%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- D Given the following data and assume the margin listed, what will be your equity position in the stock? Shares Price Margin New Price O 17% O 40% 2500 O 100% $10 50% O None of these are correct O 25% $6.0arrow_forwardThe return of stock B is __% The volatility of stock A is __% The volatility of stock B is __%arrow_forwardА ABC Po 91 51 102 Rate of return Q0 100 200 200 P1 96 46 112 Rate of return 3.78 % b. An equally weighted index Required: Calculate the first-period rates of return on the following indexes of the three stocks: (Do not round intermediate calculations. Round your answers to 2 decimal places.) a. A market value-weighted index 91 100 200 200 % P2 96 46 56 92 100 200 400arrow_forward

- Consider the following information on two stocks: P(State) Stock A Stock B Boom 20% 30% 20% Normal 50% 12% -5% Slow 15% 4% 8% Recession 15% -10% 10% $Investment Beta Asset A $35,000 1.45 Asset B $15,000 0.85 Q1. Calculate the weight of A in the portfolio. (Enter percentages as decimals and round to 4 decimals) Q2. Calculate the expected return on the portfolio. (Enter percentages as decimals and round to 4 decimals) Q3. Calculate the standard deviation of the portfolio. (Enter percentages as decimals and round to 4 decimals).arrow_forwardCovariance with Mean Return Stock AOL Microsoft Intel AOL .002 .001 15% Microsoft .001 .002 .001 12 Intel 001 .002 10 5.2. Compute the tangency portfolio weights assuming a risk-free asset yields 5 percent.arrow_forwardneed answer pleasearrow_forward

- es The following three defense stocks are to be combined into a stock index in January 2022 (perhaps a portfolio manager believes these stocks are an appropriate benchmark for his or her performance): Douglas McDonnell Dynamics General International Rockwell Index value Shares (millions) 420 450 250 2022 return 2023 return a. Calculate the initial value of the index if a price-weighting scheme is used. 1/1/22 $ 63 53 82 Price 1/1/23 $ 67 47 71 % % b. What is the rate of return on this index for the year ending December 31, 2022? For the year ending December 31, 2023? Note: A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places. 1/1/24 $ 84 61 87arrow_forwardStock Expected Return Dollar Invested Microsoft 12.00% 25000 IBM 11.50% 25000 GE 10.00% 25000 Exxon 9.50% 25000 10.75% 100000 What is the portfolio's return?arrow_forwardReview the following market information: Current Stock Market Return 11.25% Current T-Bill Price $979.43 Historic T-Bill Average Return 2.80% Historic Stock Market Average Return 8.10% Stock Beta 1.23 What is the required return (rounded to two places)?arrow_forward

- What is the expected return of a portfolio consisting of $6,000 stocks G and $4,000 stock H ? State of Probability of Returns if State Occurs Economy State of Economy Stock G (" Stock H ")/(11%) Boom 22% 14% 1% Normal 78% 7% 9% a. 7.2% b. 7.6% c. $7.9% d. 8.3% e. $8.9% 33. Joel Foster is the portfolio manager of the SF Fund, a $1 million hedge fund that contains the following stocks. The required rate of return on the market is 10% and the risk-free rate is 4%. What rate of return should investors expect (and require) on this fund? Stoo Amount bar(A) 270,000 B 330,000 1.4 bar(C) 400,000 0.7 $1,000,000 a. 8.756% b. 9.382% c. 9.921%arrow_forwardColonel Motors (C) Separated Edison (S) Expected Return 10% 8% Standard Deviation 6% 3% Please represent graphically all potential combinations of stocks C and S, if the correlation coefficient between the returns of stocks C and S is: A) 1 B) 0 C) -1 Please report these investment opportunity sets in the corresponding Excel sheets.arrow_forward4 Skipped Use the following data for Questions 3-5: Value 12500 17500 20000 Stock A B C Exp. Return 8.5% 9.2% 10.6% Beta 0.8 1.2 1.4 Question 4: What is the portfolio's Beta? ENTER YOUR ANSWER ROUNDED TO 2 DECIMAL PLACESarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education