Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

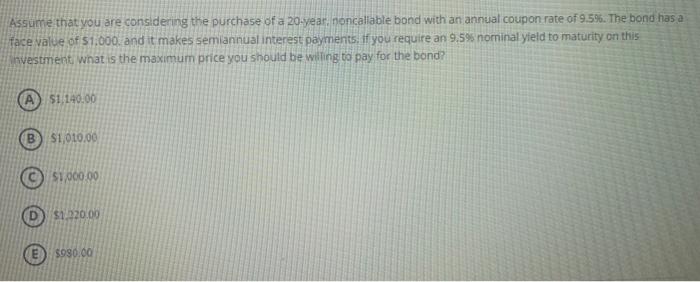

Transcribed Image Text:Assume that you are considering the purchase of a 20-year, noncallable bond with an annual coupon rate of 9.5%. The bond has a

face value of $1,000, and it makes semiannual interest payments. If you require an 9.5% nominal yield to maturity on this

investment, what is the maximum price you should be willing to pay for the bond?

A $1,140.00

B $1,010,00

$1,000.00

$1,220.00

$980.00

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Bond X is noncallable and has 20 years maturity, a 9% annual ciupon, and a $1,000 par value. Your required return on bond X is 10% and if you buy it, you plan to hold it for 5 years. You (and the market) have expectations that in 5 years, the yield to maturity on a 15— year bond with similar risk will be 8.5%. How much should you be willing to pay for Bond X today? Please show formula and computation, not in spreadsheetarrow_forwardA one-year zero coupon bond costs $99.43 today. Exactly one year from today, it will pay $100. What is the annual yield-to-maturity of the bond? (1.e., what is the discount rate one needs to use to get the price of the bond given the future cash flow of $100 in one year?) 1.0057 0.0057 2.0057 -0.0057arrow_forwardFind the price a purchaser should be willing to pay for the given bond. Assume that the coupon interest is paid twice a year. $19,000 bond with coupon rate 6% that matures in 4 years; current interest rate is 5% The purchaser should be willing to pay $ (Simplify your answer. Round to the nearest cent as needed.)arrow_forward

- If you are issuing a bond that will make an annual (once per year) coupon payment of $30 for 20 years, will return a face value payment of $1000 in year 20, and the going interest rate is 2%, then the bond will fetch roughly $___________ in the market. 1160 1600 1000 1240arrow_forwardAssume that you are considering the purchase of a 30-year, noncallable bond with an annual coupon rate of 9.0%. The bond has a face value of $1,000, and it makes semiannual interest payments. If you require an 9.0% nominal yield to maturity on this investment, what is the maximum price you should be willing to pay for the bond?arrow_forwardAssume that you are considering the purchase of a 25-year, noncallable bond with an annual coupon rate of 9.0%. The bond has a face value of $1,000, and it makes semiannual interest payments. If you require a 10.8% nominal yield to maturity on this investment, what is the maximum price you should be willing to pay for the bond?arrow_forward

- Suppose that you want to construct a 2-year maturity forward loan commencing in 3 years. The face value of each bond is $1,000. Maturity (Years) 1 2 3 4 5 Price $ 996.04 895.89 833.92 772.80 675.18 Required: a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those 5-year zeros)? b. What are the cash flows on this strategy in each year? c. What is the effective 2-year interest rate on the effective 3-year-ahead forward loan? d. & e. Confirm that the effective 2-year forward interest rate equals (1 + f4) ×(1 + f5)-1. You therefore can interpret the 2-year loan rate as a 2-year forward rate for the last two years. Alternatively, show that the effective 2-year forward rate equals (1 + y5) 15 + (1+y3) ³. - 1arrow_forwardSuppose your firm issues a €100,000,000 5-year bond with a coupon rate of 8% per annum (assume annual compounding). The bond will sell at face value to investors. The underwriting spread is an up-front fee of 2%. What is the actual cost of this debt? Please enter your answer as % -- e.g. if your answer is 2.34% type in 2.34.arrow_forwardConsider a bond (with par value = $1,000) paying a coupon rate of 10% per year semiannually when the market interest rate is only 4% per half-year. The bond has three years until maturity. Required: a. Find the bond's price today and six months from now after the next coupon is paid. b. What is the total (6-month) rate of return on the bond? Complete this question by entering your answers in the tabs below. Required A Required B Find the bond's price today and six months from now after the next coupon is paid. Note: Round your answers to 2 decimal places. Current price Price after six months $ $ 1,052.42 1,044.52arrow_forward

- Give typing answer with explanation and conclusionarrow_forwardHow much would you pay for a perpetual bond that pays an annual coupon of $200 per year and yields on competing instruments are 10%? You would pay $ 2000. (Round your response to the nearest penny) If competing yields are expected to change to 12%, what is the current yield on this same bond assuming that you paid $2,000? The current yield is 10%. (Round your response to the nearest integer.) If you sell this bond in exactly one year, having paid $2,000, and received exactly one coupon payment, what is your total return if competing yields are 12%? Your total return is %. (Round your response to two decimal places)arrow_forward1 Imagine that the market yield to maturity for three-year bonds in a particular risk class is 12 per cent. You buy a bond in that risk class which offers an annual coupon of 10 per cent for the next three years, with the first payment i one year. The bond will be redeemed at par (£100) in three years. How much would you pay for tl*bond? b If you paid £105 what yield to maurity would you obtain? aarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education