ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

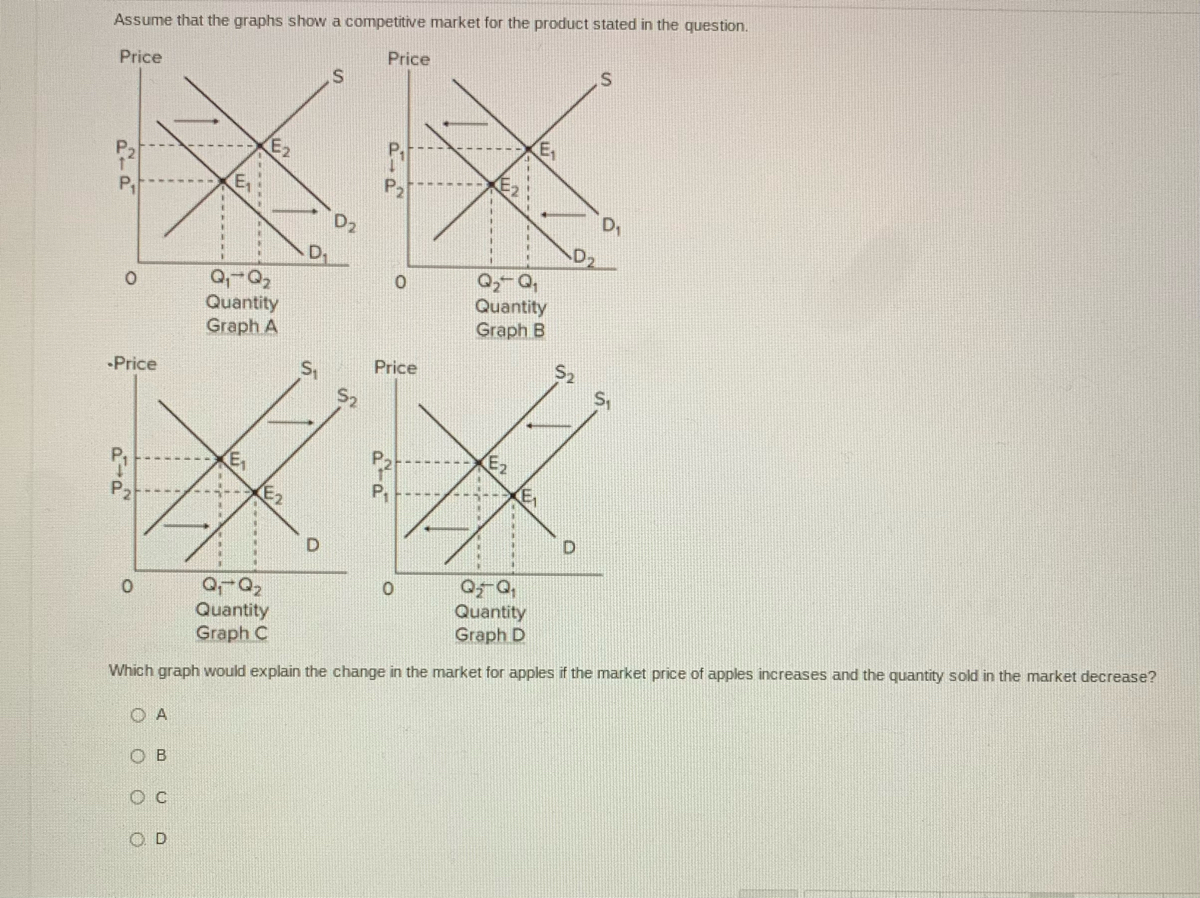

Assume that the graphs show a competitive market for the product stated in the question.

Which graph would explain the change in the market for apples if the market price of apples increases and the quantity sold in the market decrease?

Transcribed Image Text:Assume that the graphs show a competitive market for the product stated in the question.

Price

Price

P2

P2

P,

D1

D2

D.

Quantity

Graph A

Quantity

Graph B

52

Price

Price

S2

P.

Ev

P2

E2

Quantity

Graph C

Quantity

Graph D

Which graph would explain the change in the market for apples if the market price of apples increases and the quantity sold in the market decrease?

O A

OB

O D

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- You own a hot dog stand that you set up outside the student union every day at lunch time. Currently, you are selling hot dogs for a price of $3, and you sell 30 hot dogs a day (point A on the diagram). You are considering cutting the price to $2. The graph shows two possible increases in the quantity sold as a result of your price cut. Use the information in the graph (new quantities are given on the horizontal axis) to calculate the price elasticity between these two prices on each of the demand curves. Use the midpoint formula to calculate the price elasticities. A On the demand curve containing the points "A" and "B", the price elasticity of demand for a price cut from $3 to $2 is|. (Hint: Include the negative sign and enter your response rounded to two decimal places.) D2 On the demand curve containing the points "A" and "C", the price elasticity of demand for a price cut from $3 to $2 is. (Hint: Include the negative sign and enter your response rounded to two decimal places.) :37…arrow_forwardSuppose you go to Trader Joe's to buy fruit for the week. You only like apples (A) and bananas (B) and your weekly fruit budget is $11. When you arrive at Trader Joe's you notice that the price of an apple is $1.00 and the price of a banana is $0.25. QUESTION #1: How many apples and bananas should you buy? QUESTION #2: When you have found the answer, draw a diagram that shows the outcome. Step #1. Determine your preferences. Let's suppose that your preferences can be represented by the following utility function: U(A, B) = AªBß = A0.40 B0.60 FYI: This utility function is known as a Cobb-Douglas utility function. It is the most commonly used function used in economics! The reason we like it so much is that it has: 1. Constant returns (double your consumption of A and B and your utility doubles); a + B = 1 2. Diminishing marginal utility (the extra utility gained from consuming A (or B) decreases as you consume more of the A good (or B good); a 0.40); B > a. Step #2: Determine your…arrow_forwardPlease provide an explanation so I can do it my own. Thanks!arrow_forward

- The following graph shows the market for hamburgers in Detroit, where there are over 1,000 burger joints at any given moment. Suppose an innovation in meat processing technology makes it possible to produce more hamburgers at a lower cost than ever before. Show the efect of this change on the market for hamburgers by shifting one or both of the curves on the following graph, holding all else constant. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. Supply Demand Supply Demand QUANTITY (Hamburgers) PRICE (Dolars per hamburger)arrow_forwardWhat does the demand curve shows the relationship between?arrow_forwardSam is a skilled toy maker who is able to produce both cars and balls. He has 8 hours a day to produce toys. The following table shows the daily output resulting from various possible combinations of his time. Choice Hours Producing Produced (Cars) (Balls) (Cars) (Balls) A 8 0 4 0 B 6 2 3 8 C 4 4 2 14 D 2 6 1 16 E 0 8 0 17 On the following graph, use the blue points (circle symbol) to plot Sam's initial production possibilities frontier (PPF). Initial PPFNew PPF012345678302520151050BALLSCARS Suppose Sam is currently using combination D, producing one car per day. His opportunity cost of producing a second car per day is per day. Now, suppose Sam is currently using combination C, producing two cars per day. His opportunity cost of producing a third car per day is per day. From the previous analysis, you can determine that as Sam increases his production of cars, his opportunity cost of producing one more car .…arrow_forward

- Suppose the market demand for a cup of cappuccino is given by Qp = 24-4P and the market supply for a cup of cappuccino is given by Qs = 8P - 12, where P = price (per cup). Graph the supply and demand schedules for cappuccino. 1.) Using the line drawing tool, draw the demand curve for cappuccino. Label your line 'D'. 2.) Using the line drawing tool, draw the supply curve for cappuccino. Label your line 'S'. 3.) Using the point drawing tool, plot the equilibrium price and quantity. Label your point 'E'. Carefully follow the instructions above and only draw the required objects. Price per cup ($) 10.50- 웅 9.00- 7.50 6.00 4.50 3.00+ 1.50- 3 Market for Cappuccino 6 9 12 15 Cups of cappuccino 18 21 24arrow_forwardExplain using words and graphs where an individual demand curve is derived(where do they come from)?arrow_forwardPlease answer all parts of the question. Thank You!arrow_forward

- The following graph shows the market for cereal in San Diego, where there are over 1,000 stores that sell cereal at any given moment. Suppose a new scientific study shows that San Diego is the most polluted city in the world. Due to health concerns, a significant number of families move out of the city. *graph Now suppose Congress passes a new tax that decreases the income of San Diego residents. If cereal is a normal good, this will cause the demand for cereal to increase or decrease?arrow_forwardConsider the market for chocolate ice cream. Suppose the price of chocolate pudding (a substitute for consumers) decreases. Choose which one of the following diagrams best illustrates how the market for chocolate ice cream will change. C ***K **** To answer the question write the letter of the diagram only. A Answer: D₁ B F G D Harrow_forwardThis problem involves solving demand and supply equations together to determine price and quantity. a. Consider a demand curve of the form QD=-2P+20, where QD is the quantity demanded of a good and P is the price of the good. Graph this demand curve. Also draw a graph of the supply curve Qs =2P-4, where Qs is the quantity supplied. Be sure to put P on the vertical axis and Q on the horizontal axis. Assume that all the Qs and Ps are nonnegative for parts a, b, and c. At what values of P and Q do these curves intersect-that is, where does QD = Qs ? b. Now, suppose at each price that individuals demand four more units of output-that the demand curve shifts to QD - 2P+24. Graph this new demand curve. At what values of P and Q does the new demand curve intersect the old supply curve-that is, where does QD = Qs ? c. Now finally, suppose the supply curve shifts to Q's=2P-8. Graph this new supply curve. At what values of P and Q does QD=Q's? Show all working calculations and label garph with…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education