ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

Please help with the incorrect and unanswered questions. If someone can help I will give a thumbs up. I included all the info I was given. Thanks! :)

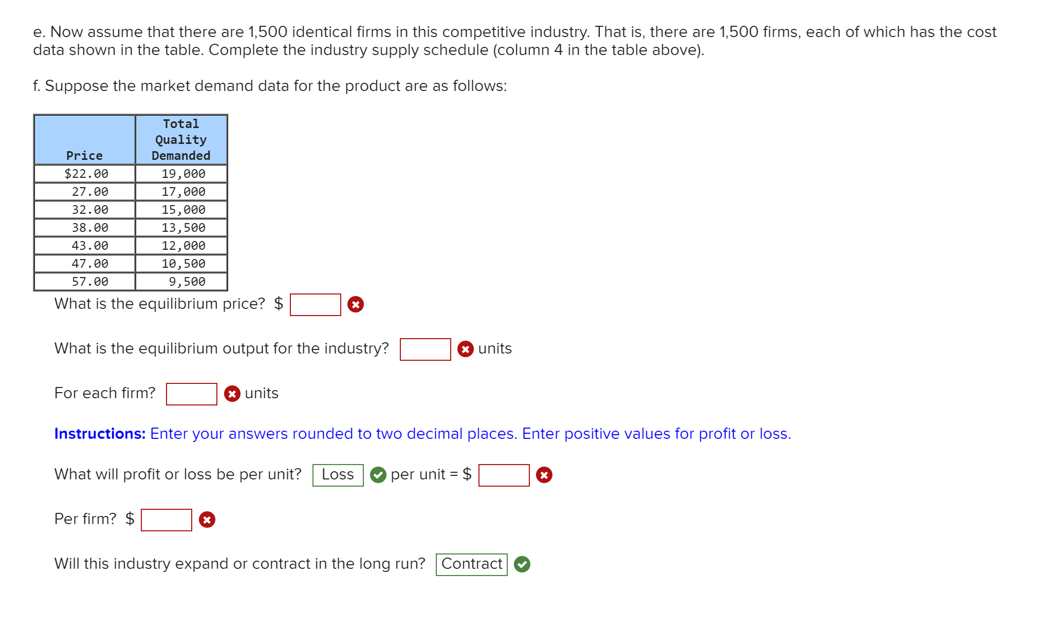

Transcribed Image Text:e. Now assume that there are 1,500 identical firms in this competitive industry. That is, there are 1,500 firms, each of which has the cost

data shown in the table. Complete the industry supply schedule (column 4 in the table above).

f. Suppose the market demand data for the product are as follows:

Total

Quality

Price

Demanded

$22.00

19,000

17,000

15,000

13,500

27.00

32.00

38.00

43.00

12,000

47.00

10,500

57.00

9,500

What is the equilibrium price? $

What is the equilibrium output for the industry?

units

For each firm?

units

Instructions: Enter your answers rounded to two decimal places. Enter positive values for profit or loss.

What will profit or loss be per unit?

Loss

per unit = $

Per firm? $

Will this industry expand or contract in the long run? Contract

Transcribed Image Text:Assume that the cost data in the following table are for a purely competitive producer:

Average Average Average

Variable

Total

Fixed

Total

Marginal

Product

Cost

Cost

Cost

Cost

$60.00

$45.00

$105.00 $45.00

2

30.00

42.50

72.50

40.00

20.00

40.00

60.00

35.00

4

15.00

37.50

52.50

30.00

5

12.00

37.00

49.00

35.00

6.

10.00

37.50

47.50

40.00

7

8.57

38.57

47.14

45.00

8

7.50

40.63

48.13

55.00

6.67

43.33

50.00

65.00

10

6.00

46.50

52.50

75.00

Instructions: If you are entering any negative numbers be sure to include a negative sign (-) in front of those numbers. Select "Not

applicable" and enter a value of "O" for output if the firm does not produce.

a. At a product price of $66.00

(i) Will this firm produce in the short run?

(ii) If it is preferable to produce, what will be the profit-maximizing or loss-minimizing output?

Profit-maximizing

O output =

9 O units per firm

(iii) What economic profit or loss will the firm realize per unit of output? Profit

per unit = $

16

b. At a product price of $41.00

(i) Will this firm produce in the short run?

Yes

(ii) If it is preferable to produce, what will be the profit-maximizing or loss-minimizing output?

Loss-minimizing O

output = |

6

units per firm

(iii) What economic profit or loss will the firm realize per unit of output?

Loss

O

per unit = $

-39

c. At a product price of $32.00

(i) Will this firm produce in the short run?

No

(ii) If it is preferable to produce, what will be the profit-maximizing or loss-minimizing output?

Not applicable

output =

0 O units per firm

(iii) What economic profit or loss will the firm realize per unit of output? Total loss O per unit = $

60 0

Instructions: Enter your answers as a whole number. If you are entering any negative numbers be sure to include a negative sign (-) in

front of those numbers.

d. In the table below, complete the short-run supply schedule for the firm (columns 1 and 2) and indicate the profit or loss incurred at

each output (column 3).

(1)

(2)

(3)

(4)

Quantity

Supplied,

Single Firm

Profit (+) or

Loss (-)

Quantity Supplied,

1,500 Firms

Price

$22.00

27.00

32.00

38.00

43.00

47.00

57.00

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- B Spreadsheet A bank's mortgage department must process the following six jobs to maximize client satisfaction. Processing Time (days) 14 12 16 11 18 22 Mortgage 1 2 3 4 5 6 55 17 80 22 39 60 What sequencing rule should you use? For the rule you selected, find the best sequence using the Excel Sequencing template. The most appropriate sequence rule is -Select- The best sequence is -Select- ✔ -Select- ✓ -Select- ✓ Due Date -Select- ✓ -Select- ✔ -Select- ✓arrow_forwardTyped plz and Asap Please give me a quality solution thanksarrow_forwardDefine the term Expenses?arrow_forward

- Pls help ASAParrow_forwarduestion 3 If you want to minimize interest payments on a loan, you'll need one that has a simple interest rate so that yo John opened an account, and knew exactly how much it would be worth at the end of the year, because it used year. What is simple interest? Oa. Interest only on original amount saved or borrowed Ob. interest on original amount saved, borrowed and other interest earned Oc. a fee paid for the use of someone else's money Od. taxes on the original amount saved or borrowed L A Moving to another question will save this response. →arrow_forwardWhat cultural aspects (language, religion, customs) a company must have in the area of technologyarrow_forward

- ctors) on of es 1. Relationship of data usage and bill Data Usage(GB/month) 0 10 20 30 Bill($/month) 10 30 50 70 A. Draw the graph, placing data usage horizontally(on the X axis) and bill vertically(On the Y axis). B. How much is the monthly fixed fee? C. How much is the charge per GB? D. What is the Equation that describes the relationship, where data usage is denoted by D, and bill by B? E. How much would be the charge for 50 GB use per month?arrow_forwardhow you know what c value to look atarrow_forwardB. The late Anne Collins had 3 children, Mary, John and Hana who unfortunately all predeceased Anne leaving several Anne's grandchildren and great grandchildren. Unfortunately, Anne died intestate without a will or trust. She is survived by: Mary's daughters Emma and Joan John's son Patrick who has 2 children Joe and Frank; Frank has 1 child Eddy. Hana's daughter Elizabeth is also deceased leaving 2 children Jim and Eva. (i) Please fill in the table taking into consideration that Anne died without a will/trust and therefore the distribution shall be according to the CA intestacy laws (Modified Per Stirpes PC 240). Each Emma and Joan Mary's spouse Each of Patrick's 2 children Joe and Frank Each of Elizabeth's 2 children Jim and Eva Patrick's grandchild Eddy Patrick MPS Øarrow_forward

- Which type of graph will be suitable for representing the above sales revenue by regionsarrow_forwardTyped plz and asap please provide me a quality solution for better ratings and take care of plagiarism also ( please I need it asap I will up vote thanks )arrow_forwardExercise: 01 Issue a promissory note: ⑴Amount £3,026.00 ⑵Date and place of issue 8/August/2009,Guangzhou, China ⑶Tenor At 90 days after date ⑷Maker Guangdong Imp. & Exp. Co., Guangzhou ⑸Payee Chemicals Import & Export Company London ⑴Drawer Thames Enterprises Ltd., London ⑵Drawee The National Westminster Bank Ltd., London ⑶Payee Philips Hong Kong ⑷Date and place of issue 07/01/2001,London ⑸Amount GBP79,014 Exercise: 02 Issue a check:arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education