ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

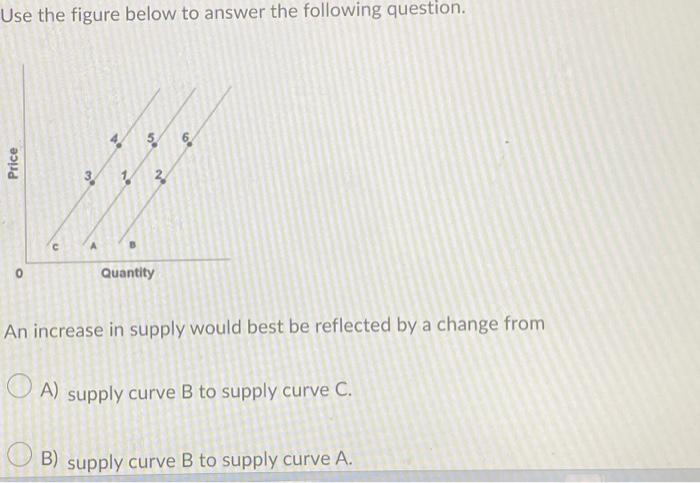

Transcribed Image Text:Use the figure below to answer the following question.

Price

0

C

A

50

1 2

Quantity

6⁰

An increase in supply would best be reflected by a change from

A) supply curve B to supply curve C.

B) supply curve B to supply curve A.

Transcribed Image Text:Price

0

Quantity

An increase in supply would best be reflected by a change from

A) supply curve B to supply curve C.

B) supply curve B to supply curve A.

C) supply curve A to supply curve C.

OD) supply curve A to supply curve B.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- If products A and B are substitutes, products B and C are complements and the markets for products A and B are unrelated, which one of the following statements regarding the markets for products A, B and C is true? a) A decrease in the price of product A will result in an increase in the demand for product B b) A decrease in the price of product A will result in an increase in the demand for product C c) An increase in the price of product B will result in an increase in the demand for product C d) An increase in the price of product B will result in an increase in the demand for product Aarrow_forwardHow would the equilibrium price (P) and equilibrium quantity (Q) for a good be affected if there was a simultaneous increase in demand along with a decrease in supply? P would increase while Q would decrease OP would increase but the impact on Q would be ambiguous Q would increase but the impact on P would be ambiguous Both P and Q would increasearrow_forwardDeterminants of supply What causes the supply curve to shift left or right? This could include, amongst other thingsarrow_forward

- Assume the demand curve for gasoline is downward sloping and the supply curve is upward sloping. Start by considering the gasoline market in 2020. Draw a graph that shows supply and demand analysis for gasoline in this city. Label the supply curve as S0; demand curve as D0; the equilibrium price as P0; and equilibrium quantity as Q0.arrow_forwardAnalyze the effects of changes in demand and supply on market equilibrium.arrow_forwardNearly all supply curves share a basic similarity: they slope ________________.arrow_forward

- The primary difference between a change in demand and a change in the quantity demanded is a change in demand is a movement along the demand curve and a change in quantity demanded is a shift in the demand curve. a change in quantity demanded is a movement along the demand curve and a change in demand is a shift in the demand curve. both a change in quantity demanded and a change in demand are shifts in the demand curve, only in different directions. both a change in quantity demanded and a change in demand are movements along the demand curve, on in different directions.arrow_forwardWhat are the determinants of supply? What happens to the supply curve when any of these determinants changes? Distinguish between a change in supply and a change in the quantity supplied, noting the cause(s) of each.arrow_forwardWhich of the following will produce a price increase for Good X? For each case, plot a chart with supply and demand curves to show your idea. Demand rises while Supply falls. Demand falls while Supply is constant. Supply falls while Demand is constant. Demand falls faster than Supply falls. Supply rises while Demand falls. Demand rises faster than Supply rises.arrow_forward

- Find the market equilibrium point for the following demand and supply functions. Demand: 2p= -q+45 Supply: 3p-q=20arrow_forwardIf supply is upward sloping, a decrease in demand with no change in supply will lead to a(n) _____ in equilibrium quantity and a(n) _____ in equilibrium pricearrow_forwardHurricane Erica is expected to hit central Florida hard. This is a major orange-growing region. Which of the following choices best describes the effect on the supply curve for oranges? A Shift the supply curve right B Shift the supply curve left C Movement along the supply curve upward D Movement along the supply curve downwardarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education