FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

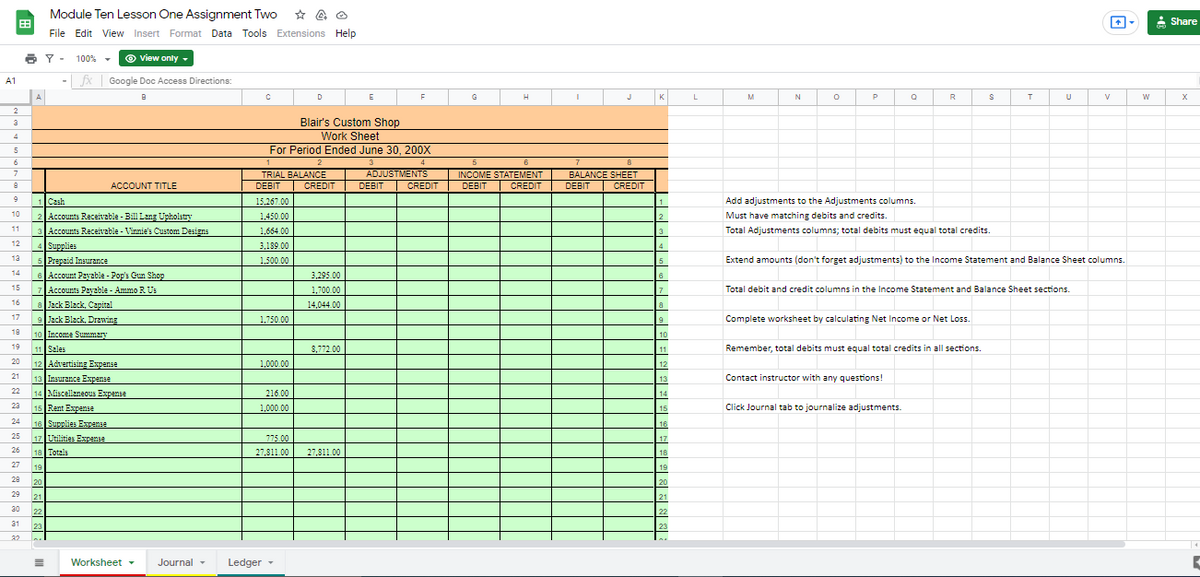

Adjustments are:

Blair’s Custom Shop performed a count of supplies at the end of the accounting period (June 30, 20XX) and determined that value of supplies "on hand" (not used) was $1,700.00. The value of prepaid insurance coverage "on hand" (not used) at the same time was $750.00. Calculate the adjustment amount for Supplies and Prepaid Insurance and enter those amounts on the worksheet.

Remember, for each adjustment you should have one entry in the Adjustments DEBIT column and a matching entry in the Adjustments CREDIT column.

- Extend the adjusted balances for the Supplies and Prepaid Insurance accounts and their related expense accounts to the appropriate columns on the worksheet.

- Total the Adjustment columns to ensure the debits equal the credits.

- Total the Income Statement columns and determine net income or net loss to balance debits/credits.

- Total the

Balance Sheet columns and use net income/net loss amount to balance debits/credits. - Single and double rule all totals. SAVE

- Journalize the Adjustments from the worksheet onto the Journal tab. SAVE

Post the journal entries onto the Ledger tab. SAVE

Transcribed Image Text:Module Ten Lesson One Assignment Two * a

A Share

File Edit View Insert Format Data Tools Extensions Help

O Y -

100% -

© view only-

A1

- fx Google Doc Access Directions:

K

P.

A.

D

E

G

J

L

M

N

R

U

X

2

Blair's Custom Shop

Work Sheet

For Period Ended June 30, 200X

5.

6.

7.

5

ADJUSTMENTS

TRIAL BALANCE

DEBIT CREDIT

INCOME STATEMENT

BALANCE SHEET

CREDIT

ACCOUNT TITLE

DEBIT

CREDIT

DEBIT

CREDIT

DEBIT

1Cash

2 Accounts Receivable - Bill Lang Upholstry

15,267.00

Add adjustments to the Adjustments columns.

10

1,450.00

12

Must have matching debits and credits.

11

3 Accounts Receivable - Vinnie's Custom Designs

4 Supplies

5 Prepaid Insurance

6 Account Payable - Pop's Gun Shop

7 Accourts Payable - Ammo R Us

a Jack Black, Capital

9 Jack Black, Drawing

1,664.00

3

Total Adjustments columns; total debits must equal total credits.

12

3,189.00

14

13

1,500.00

5

Extend amounts (don't forget adjustments) to the Income Statement and Balance Sheet columns.

14

3,295.00

15

1,700.00

Total debit and credit columns in the Income Statement and Balance Sheet sections.

16

14,044.00

17

1,750.00

19

Complete worksheet by calculating Net Income or Net Loss.

19

10 Income Summary

10

19

11 Sales

8,772 00

11

Remember, total debits must equal total credits in all sections.

20

12 Advertising Expense

13 Insurance Expense

14 Miscellaneous Expense

15 Rent Expense

16 Supplies Expense

17 Utilities Expanse

1,000.00

12

21

13

Contact instructor with any questions!

22

216.00

14

23

1,000.00

15

Click Journal tab to journalize adjustments.

24

16

25

775.00

17

26

18 Totals

27,811.00

27,811.00

18

27

19

19

29

20

20

29

21

21

30

22

22

31

23

23

22

Worksheet -

Journal -

Ledger -

Transcribed Image Text:Module Ten Lesson One Assignment Two

Module Ten Lesson One Assignment Two

* Share

File Edit View Insert Format Data Tools Extensions Help

File Edit View Insert Format Data Tools Extensions Help

6 Y- 100% -

© View only

aY. 100% -

O View only -

A1

- fx ||

fx |

A B

D

E

F

H

K

L

M

A

F

12

13

GENERAL JOURNAL

PAGE 8

14

ACCOUNT Prepsid Insurance

ACCOUNT NO.

140

1

15

DOC. POST.

REF

GENERAL

CREDIT

POST.

BALANCE

16

DATE

ACCOUNT TITLE

NO.

DEBIT

17

DATE

ITEM

REF.

DEBIT

CREDIT

DEBIT

CREDIT

Adjusting Entries

18

Jan

1

2

19

1

1.500.00

1.500.00

20

21

4

22

5

23

6

24

7

25

26

27

ACCOUNT Insurance Expanse

ACCOUNT NO

530

10

10

28

11

11

29

POST.

BALANCE

12

12

30

DATE

ITEM

REF

DEBIT

CREDIT

DEBIT

CREDIT

31

32

33

34

35

36

37

39

40

ACCOUNT Succlies Expense

ACCOUNT NO.

560

41

42

POST.

BALANCE

43

DATE

ITEM

REF.

DEBIT

CREDIT

DEBIT

CREDIT

44

45

46

47

48

50

%3D

Worksheet

Journal -

Ledger

%3D

Worksheet

Journal -

Ledger -

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- On decmeber 31, the trial balance indicates that the supplies account has a balance, prior to the adjusting entry,pf $320. A physical count of the supplies inventory shows that $90 of supplies remain. Analyze this adjustment for the supplies using T accounts and then formally enter this adjustment in the generaljournal.arrow_forwardReviewing insurance policies revealed that a single policy was purchased on October 1st, for one year's coverage, in the amount of $1,200. There was no previous balance in the prepaid insurance account at that time. Based on the information provided: Make the December 31st adjusting journal entry to bring the balance to correct Insurance Expense?- Prepaid Insurance?- What is the remaining balance for the prepaid insurance on December 31st?arrow_forwardChabon Corp. purchased a six-month insurance policy on December 1, 20X1 for $600 in cash. The policy period begins on December 1. Part 1: Record the December 1 transaction as well as the year-end adjusting entry. Part 2: Answer the following questions: How much of the December 1 cash payment is still prepaid on December 31? Where should the amount still prepaid at year-end be reported on the financial statements?arrow_forward

- Could anyone explain this question: Washington Corp. purchased a 24-month insurance policy on March 1, 20X6 for $480. At the time of the purchase, the "Insurance Expense" account was debited and the "Cash" account was credited for the full $480. How would you write this journal entry?arrow_forwardComplete the following adjusting entry for Mookie The Beagle Concierge.Mookie The Beagle Concierge purchased $426 of supplies during January 2018. At the end of the accounting period on January 31, Mookie The Beagle Concierge still had $236 of unused supplies on hand. The $236 of Supplies is an asset with future benefit. Since Mookie The Beagle Concierge recorded the entire $426 as Supplies Expense, an adjusting entry is needed to bring accounts up to date at January 3.arrow_forwardLancaster Company must make three adjusting entries on December 31, 20X1. a. Supplies used, $9,200 (supplies totaling $14,400 were purchased on Decem b. Expired insurance, $6,400; on December 1, 20X1, the firm paid $38,400 for s debited Prepsid Insurance for this amount. c. Depreciation expense for equipment, $4,000. Required: Prepare the journal entries for these adjustments and post the entries to the gerarrow_forward

- Wilson Company paid $6,300 for a 4-month insurance premium in advance on November 1, with coverage beginning on that date. The balance in the prepaid insurance account before adjustment at the end of the year is $6,300, and no adjustments had been made previously. The adjusting entry required on December 31 is: Multiple Choice O O O Debit Prepaid Insurance, $1,575; credit Insurance Expense, $1,575. Debit Cash, $6,300; Credit Prepaid Insurance, $6,300. Debit Prepaid Insurance, $3,150; credit Insurance Expense, $3,150. O Debit Insurance Expense, $1,575; credit Prepaid Insurance, $1,575. Debit Insurance Expense, $3,150; credit Prepaid Insurance, $3,150.arrow_forwardReviewing insurance policies revealed that a single policy was purchased on August 1, for oneyear’s coverage, in the amount of $6,000. There was no previous balance in the Prepaid Insurance account atthat time. Based on the information provided:A. Make the December 31 adjusting journal entry to bring the balances to correct.B. Show the impact that these transactions had.arrow_forwardThe Allowance balance is a $200 credit before adjustment. Uncollectible accounts are estimated to be $2,000. The adjusting entry to record uncollectible accounts is: GENERAL JOURNAL 1 2 1 2 Date Chapter 8-Receivables Now, the adjusting entry to record uncollectible accounts is: GENERAL JOURNAL Description a. Description If the Allowance balance started with a $200 DEBIT balance and uncollectible accounts are estimated to be $2,000. Date с. Post ref Debit Post ref Note: Bad Debt Expense estimate in the prior year was wrong, it was not an error. It was still a good faith estimate and the apparent violation of the matching principle is allowed under GAAP. Age Interval Not Past Due 1-30 days past due Debit At the end of the current year, the accounts receivable account has a debit balance of $1,400,000 and sales for the year total $15,350,000. Determine the amount of the adjustment needed. Page Credit The allowance account before adjustment has a debit balance of $23,000. Bad debt expense…arrow_forward

- How to adjust and write this on general journal? The prepaid insurance account amounts to $12,000. Of this amount, $8,500 has expired as of December 31.arrow_forwardThe balance in the Prepaid Insurance account before adjustment is $16,500 (assume normal balance). As of 10/31 the amount of insurance that has expired is $6,500arrow_forwardThe prepaid insurance account had a beginning balance of $3,755 and was debited for $6,755 of premiums paid during the year. Journalize the adjusting entry required at the end of the year, assuming the amount of unexpired insurance related to future periods is $2,640. Refer to the Chart of Accounts for exact wording of account titles.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education