ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

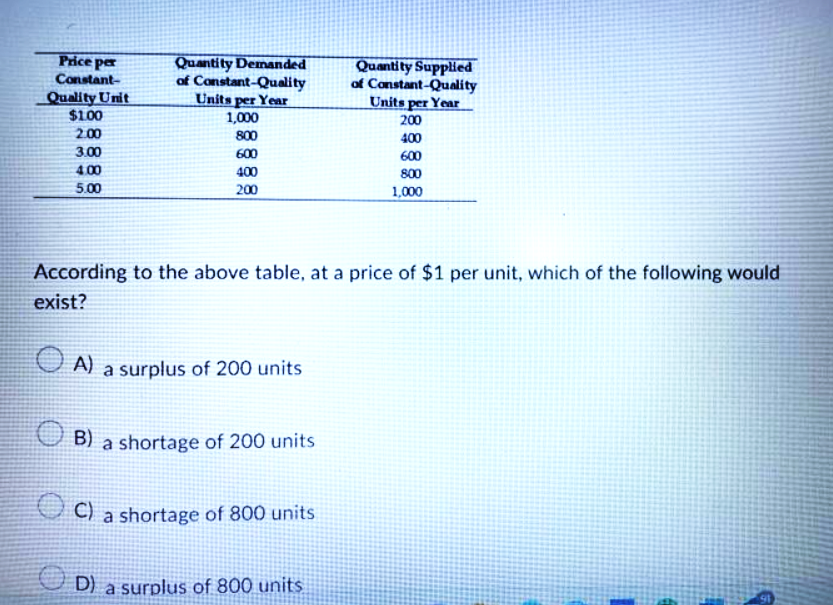

Transcribed Image Text:Price per

Constant-

Quality Unit

$1.00

2.00

3.00

4.00

5.00

Quantity Demanded

of Constant-Quality

Units per Year

1,000

800

600

400

200

According to the above table, at a price of $1 per unit, which of the following would

exist?

A) a surplus of 200 units

Quantity Supplied

of Constant-Quality

Units per Year

200

400

600

800

1,000

OB) a shortage of 200 units

OC

C) a shortage of 800 units

ⒸD) a surplus of 800 units

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Demand and Supply Schedule for Good Y: Unit price of y Quantity demanded of y Quantity supplied of y Price elasticity of demand of y (2 decimals) Price elasticity of supply of y (2 decimals) $100 10 40 n/a n/a $90 11 35 $80 12 30 $70 13 25 $60 14 20 $50 15 15 $40 16 10 $30 17 5 $20 18 1 $10 19 0arrow_forwardNonearrow_forwardAssuming an increase in Demant and decrease in Supply, which of the following statements is TRUE? The price of the good will decrease. The quantity of the good will definitely decrease. The price of this good will definitely increase. There will be a permanent shortage of this good. The new equilibrium quantity may increase, decrease, or stay the same. A surplus of this good will result from these changes in Supply and Demand. What new equiLibrium quantity will result depends on the relative magnitude of the changes and the shapes of the Demand and Supply curves. We cannot determine what will happen to price.arrow_forward

- There is a hypothetical market for bottled water. The market demand and supply are QD = 1150 – 100P and QS = -100 + 40OP. a) Find the equilibrium price and quantity.arrow_forwardwhich of the following does not directly influence the demand for a good? the size of the population consumer preferences the cost of producing the good average consumer incomearrow_forwardWhich of the following is most likely to have a low price elasticity of demand? A good that is very expensive. A good with no close substitutes. A good that most people consider a luxury. All are equally likely to have a low price elasticity of demand.arrow_forward

- Complete the following table showing a supply schedule by calculating the elasticity coefficient for each price interval. (Hint: The first numeric entry field in the "Elasticity Coefficient" column corresponds to the interval between $10 and $9, and so on, until the very last interval between $6 and $5. Use the midpoint method.) Price Quantity Supplied Elasticity Coefficient $10 50 $9 40 $8 30 $7 20 $6 10 $5 MAMAarrow_forwardQUESTION 4 For the following demand function: Q(P) = 36,500-5P Calculate the price where the quantity demanded falls to zero 7,300 8,300 7,400 9,400arrow_forwardCalculate the producers' surplus (in dollars) for the supply equation at the indicated unit price p. (Round your answer to the nearest cent.) p = 7 + 2g p = 20 ,1/3.arrow_forward

- Which of the following will not shift the supply curve to the left? a) an increase in wages paid to workers b) a decrease in the number of sellers C) an increase in the cost of production d) a decrease in cost of productionarrow_forwardIf, at the current price, there is a surplus of a good, then: A) the quantity demanded is greater than the quantity supplied. B) the market must be in equilibrium C) the price is above the equilibrium price D) Both A and C.arrow_forwardSuppose that the percentage change in supply is 15%, the price elasticity of supply is 3, and the percentage change in the equilibrium price is 3%. What is the price elasticity of demand? A) 3 B) 0 C) 1 D) 2 Suppose that the percentage change in supply is 25%, the price elasticity of demand is 1, and the percentage change in the equilibrium price is 5%. What is the price elasticity of supply? A) 2 B) 5 C) 4 D) 0 Suppose that the percentage change in demand is 16%, the price elasticity of demand is 1, and the percentage change in the equilibrium price is 4%. What is the price elasticity of supply? A) 2 B) 1 C) 3 D) 0arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education