Advanced Engineering Mathematics

10th Edition

ISBN: 9780470458365

Author: Erwin Kreyszig

Publisher: Wiley, John & Sons, Incorporated

expand_more

expand_more

format_list_bulleted

Related questions

Question

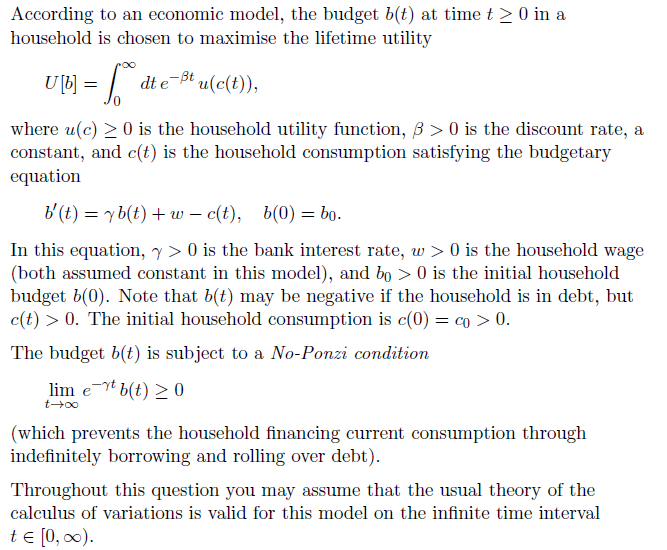

Transcribed Image Text:According

household

to an economic model, the budget b(t) at time t ≥ 0 in a

is chosen to maximise the lifetime utility

UM = [ die

₁

dt e-ßt u(c(t)),

where u(c) ≥ 0 is the household utility function, ß> 0 is the discount rate, a

constant, and c(t) is the household consumption satisfying the budgetary

equation

b'(t) = yb(t) + wc(t), b(0) = bo.

In this equation, y> 0 is the bank interest rate, w> 0 is the household wage

(both assumed constant in this model), and bo > 0 is the initial household

budget b(0). Note that b(t) may be negative if the household is in debt, but

c(t) > 0. The initial household consumption is c(0) = co > 0.

The budget b(t) is subject to a No-Ponzi condition

lim et b(t) ≥ 0

t-→∞

(which prevents the household financing current consumption through

indefinitely borrowing and rolling over debt).

Throughout this question you may assume that the usual theory of the

calculus of variations is valid for this model on the infinite time interval

t = [0, ∞).

Transcribed Image Text:(c) Hence show that the budget on the stationary path is given by

-) ert.

ekt

W

b(t) = | bo+ ~ +

Y

K

CO

W

Y

CO

K-Y

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 16 images

Knowledge Booster

Similar questions

- 4. Monthly sales of a particular computer are expected to decline at a rate of d(t) = −25t 2/3 computers per month, where t is time in months. Currently, monthly sales are 2,000 computers. Determine monthly sales 8 months from now.arrow_forwardThe total sales of a company (in millions of dollars) t months from now are given by S(t) = 0.04t³ + 0.5t² + 2t + 5. (A) Find S'(t). (B) Find S(5) and S'(5) (to two decimal places). (C) Interpret S(14)=240.76 and S'(14) = 39.52. (A) S'(t) =arrow_forwardA research group developed the following mathematical model relating systolic blood pressure and age: P(x) = a + bln(x + 1), where P(x) is pressure, measured in millimeters of mercury, and x is age in years. By examining Guilford County hospital records, they estimate the values for Guilford County to be a = 37 and b = 25. Using this model, estimate the rate of change of pressure with respect to time after 15 years. Round to the nearest hundredth (2 decimal places). millimeters per yeararrow_forward

- 15. The table gives the motor vehicles registered in the United States, C = f(t), in millions,23 in the US in the year t. (a) Do f'(t) and f"(t) appear to be positive or negative during the period 2011–2017? (b) Do f'(t) and f"(t) appear to be positive or negative during the period 2005–2009? (c) Estimate f'(2017). Using units, interpret your an- swer in terms of passenger cars. t 2005 2007 2009 2011 2013 2015 2017 C 247.4 254.4 254.2 253.1 255.9 263.6 272.5 Q > Result 12 of 14arrow_forwardCan someone help mearrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Advanced Engineering MathematicsAdvanced MathISBN:9780470458365Author:Erwin KreyszigPublisher:Wiley, John & Sons, Incorporated

Numerical Methods for EngineersAdvanced MathISBN:9780073397924Author:Steven C. Chapra Dr., Raymond P. CanalePublisher:McGraw-Hill Education

Numerical Methods for EngineersAdvanced MathISBN:9780073397924Author:Steven C. Chapra Dr., Raymond P. CanalePublisher:McGraw-Hill Education Introductory Mathematics for Engineering Applicat...Advanced MathISBN:9781118141809Author:Nathan KlingbeilPublisher:WILEY

Introductory Mathematics for Engineering Applicat...Advanced MathISBN:9781118141809Author:Nathan KlingbeilPublisher:WILEY  Mathematics For Machine TechnologyAdvanced MathISBN:9781337798310Author:Peterson, John.Publisher:Cengage Learning,

Mathematics For Machine TechnologyAdvanced MathISBN:9781337798310Author:Peterson, John.Publisher:Cengage Learning,

Advanced Engineering Mathematics

Advanced Math

ISBN:9780470458365

Author:Erwin Kreyszig

Publisher:Wiley, John & Sons, Incorporated

Numerical Methods for Engineers

Advanced Math

ISBN:9780073397924

Author:Steven C. Chapra Dr., Raymond P. Canale

Publisher:McGraw-Hill Education

Introductory Mathematics for Engineering Applicat...

Advanced Math

ISBN:9781118141809

Author:Nathan Klingbeil

Publisher:WILEY

Mathematics For Machine Technology

Advanced Math

ISBN:9781337798310

Author:Peterson, John.

Publisher:Cengage Learning,