Principles of Economics 2e

2nd Edition

ISBN: 9781947172364

Author: Steven A. Greenlaw; David Shapiro

Publisher: OpenStax

expand_more

expand_more

format_list_bulleted

Related questions

Question

Solve d please

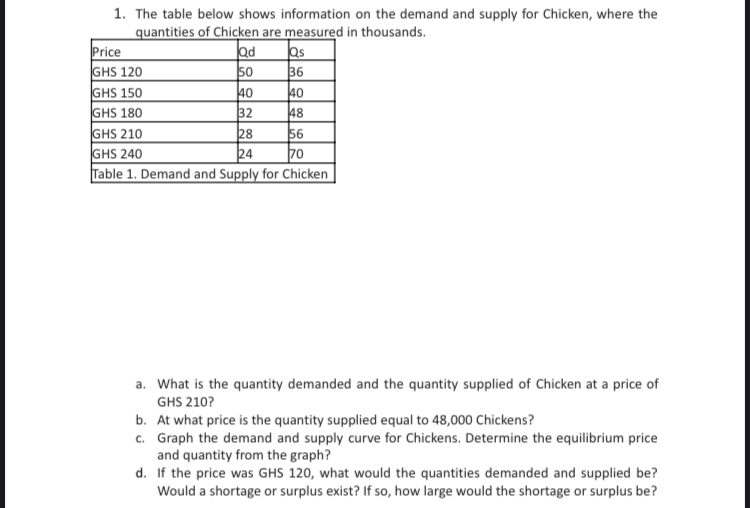

Transcribed Image Text:1. The table below shows information on the demand and supply for Chicken, where the

quantities of Chicken are measured in thousands.

Price

GHS 120

GHS 150

GHS 180

GHS 210

GHS 240

Table 1. Demand and Supply for Chicken

Qd

Qs

36

50

40

40

32

48

56

70

28

24

a. What is the quantity demanded and the quantity supplied of Chicken at a price of

GHS 210?

b. At what price is the quantity supplied equal to 48,000 Chickens?

c. Graph the demand and supply curve for Chickens. Determine the equilibrium price

and quantity from the graph?

d. If the price was GHS 120, what would the quantities demanded and supplied be?

Would a shortage or surplus exist? If so, how large would the shortage or surplus be?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- What is the difference between the demand and the quantity demanded of a product, say milk? Explain in words and show the difference on a graph with a demand curve for milk.arrow_forwardExplain why the following statement is false: In the goods market, no seller would be willing to sell for less than the equilibrium price.arrow_forwardTable 3.9 illustrates the markets demand and supply for cheddar cheese. Graph the data and find the equilibrium. Next, create a table showing the change in quantity demanded or quantity supplied, and a graph of the new equilibrium, in each of the following situations: The price of milk, a key input for cheese production, rises, so that the supply decreases by 80 pounds at every price. A new study says that eating cheese is good for your health, so that demand increases by 20 at every price.arrow_forward

- Review Figure 3.4. Suppose the price of gasoline is 1.60 per gallon. Is the quantity demanded higher or lower than at the equilibrium price of 1.40 per gallon? What about the quantity supplied? Is there a shortage or a surplus in the market? If so, how much? Figure 3.4 Demand and Supply of Gasolinearrow_forwardHow can you locate the equilibrium point on a demand and supply graph?arrow_forwardSuppose the cross-price elasticity of apples with respect to the price of oranges is 0.4, and the price of oranges falls by 3. What will happen to the demand for apples?arrow_forward

- How does one analyze a market where both demand and supply shift?arrow_forwardWhat does a downward-sloping demand curve mean about how buyers in a market will react to a higher price?arrow_forwardWhat is the relationship between quantity Demanded and quantity supplied at equilibrium? What is the relationship when there is a shortage? What is the relationship when them is a surplus?arrow_forward

- In an analysis of the market for paint, an economist discovers the facts listed below. State whether each of these changes will affect supply or demand, and in what direction. There have recently been some important cost-saving inventions in the technology for making paint. Paint is lasting longer so that property owners need not repaint as often. Because of severe hailstorms, many people need to repaint now. The hailstorms damaged several factories that make paint, forcing them to close down for several months.arrow_forwardThe following table summarizes information about the market for principles of economics textbooks: Price Quantity Demanded per Year Quantity Supplied per Year $45 4,300 300 55 2,300 700 65 1,300 1,300 75 800 2,100 85 650 3,100 What is the market equilibrium price and quantity of textbooks? To quell outrage over tuition increases, the college places a $55 limit on the price of textbooks. How many textbooks will be sold now? While the price limit is still in effect, automated publishing increases the efficiency of textbook production. Show graphically the likely effect of this innovation on the market price and quantity.arrow_forwardWould you expect supply to play a more significant role in determining the price of a basic necessity like food or a luxury like perfume? Explain. Hint: Think about how the price elasticity of demand will differ between necessities and luxuries.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning  Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Microeconomics: Principles & PolicyEconomicsISBN:9781337794992Author:William J. Baumol, Alan S. Blinder, John L. SolowPublisher:Cengage Learning

Microeconomics: Principles & PolicyEconomicsISBN:9781337794992Author:William J. Baumol, Alan S. Blinder, John L. SolowPublisher:Cengage Learning

Principles of Economics 2e

Economics

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:OpenStax

Brief Principles of Macroeconomics (MindTap Cours...

Economics

ISBN:9781337091985

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:9781337091992

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Microeconomics: Principles & Policy

Economics

ISBN:9781337794992

Author:William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:Cengage Learning