Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

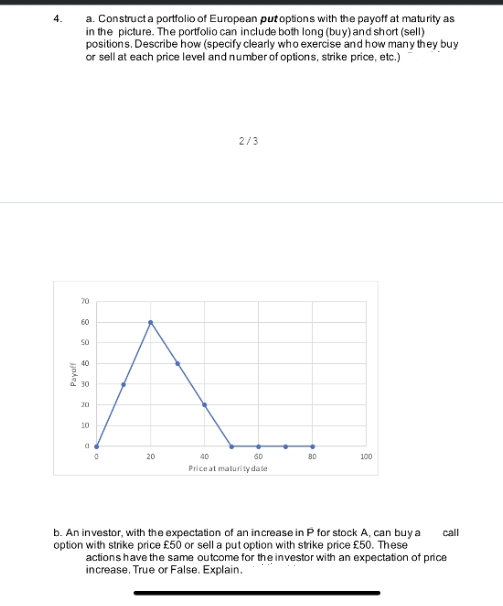

Transcribed Image Text:a. Constructa portfolio of European put oplions with the payoff at maturity as

in the picture. The portfolio can include both long (buy) and short (sell)

positions. Describe how (specify clearly who exercise and how many they buy

or sell at each price level and number of options, strike price, etc.)

2/3

70

60

50

40

30

20

10

20

40

60

80

100

Price at maturitydate

b. An investor, with the expectation of an increase in P for stock A, can buy a

option with strike price £50 or sell a put option with strike price £50. These

actions have the same outcome for the investor with an expectation of price

increase. True or False. Explain.

call

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- 4. Which of the below represents the value of an American option in each state? max(Payoff if exercised, Value if held) Payoff if exercised Risk-neutral probability min(Payoff if exercised, Value if held)arrow_forward4. Answer the following questions on exotic options: (a) Discuss the differences between a combination and a spread when constructing portfolios of options. (b) Define a long strangle and represent the profit function. (c) Design a forward contract on a stock with a particular delivery price and delivery date as a combination of options on the same underlying asset.arrow_forward3. A bear spread payoff has the form g(ST) = max(K₂- ST, 0) - max(K₁ – ST, 0), where 0 < K₁ < K₂. (a) (b) Sketch the payoff diagram. Use the general formula for the European option pricing function to find the time-zero option price of a bear spread.arrow_forward

- Real Options & Game Theory: The value of a call option and a put option is influenced by the following variables: - Underlying asset value- Strike Price- Variance of Underlying asset- Time to Expiration What effect would an increase in each of these variables have on the value of a calloption and a put option?arrow_forwardOptions have a unique set of terminology. Definethe following terms:(3) Strike price or exercise pricearrow_forwardi)identify, analyze and discuss the following characteristics of an American put option: maximum value, intrinsic value, time value, lower bound, and payoff at expiration. ii) analyze and discuss the following factors on an American put option: time to expiration, exercise price, interest rate, volatility, and dividends. iii) identify, analyze, and discuss the following characteristics of a European call option: maximum value, intrinsic value, time value, lower bound, and payoff at expiration. iv) analyze and discuss the following factors on a European call option: time to expiration, exercise price, interest rate,arrow_forward

- 11.) Define Futures Contracts, and Options. How are these products commonly used as portfolio diversification mechanisms?arrow_forwardplease give me answerarrow_forwarda)analyze and discuss the following factors on a European call option: time to expiration, exercise price, interest rate, volatility, and dividends. b) identify, analyze, and discuss the following characteristics of a European put option: maximum value, intrinsic value, time value, lower bound, and payoff at expiration. c) analyze and discuss the following factors on a European put option: time to expiration, exercise price, interest rate, volatility, and dividends. d) discuss the relationship between American and European option prices. e) derive the put-call parity and discuss its implications. f) discuss the characteristics of a currency option.arrow_forward

- Describe how a typical stock option plan works. What are someproblems with a typical stock option plan?arrow_forwardIdentify the key parameters that influence option price. Discuss the impact of a rise and fall in the value of each parameter on the prices of put and call options.arrow_forwardConsider a portfolio consisting of one share and several European call options with the same expiry, but different strike prices. The payoff diagram of the portfolio is given by the following figure. Find the strike prices and the positions of each call option. Portfolio payoff 25 20 15 10 15 20 25 30 Stock price Payoffarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education