ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

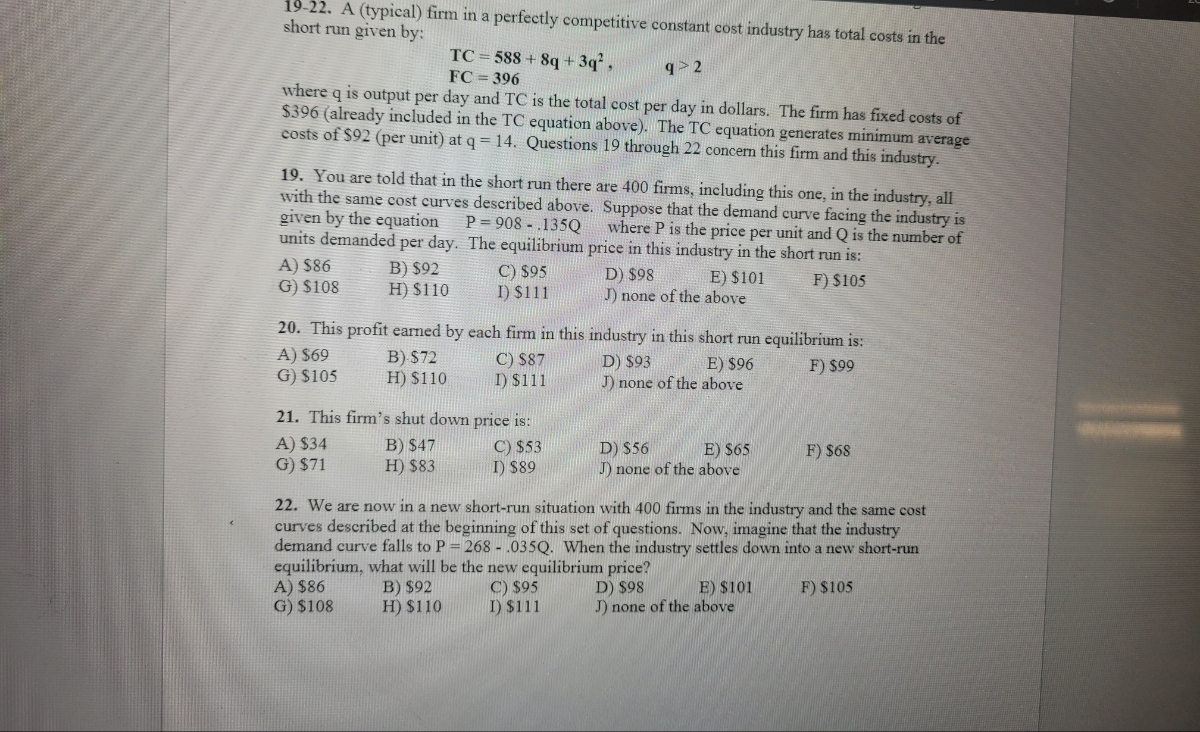

Transcribed Image Text:19-22. A (typical) firm in a perfectly competitive constant cost industry has total costs in the

short run given by:

TC 588 +8q+3q², 9 2

FC=396

where q is output per day and TC is the total cost per day in dollars. The firm has fixed costs of

$396 (already included in the TC equation above). The TC equation generates minimum average

costs of $92 (per unit) at q = 14. Questions 19 through 22 concern this firm and this industry.

19. You are told that in the short run there are 400 firms, including this one, in the industry, all

with the same cost curves described above. Suppose that the demand curve facing the industry is

given by the equation P=908.135Q where P is the price per unit and Q is the number of

units demanded per day. The equilibrium price in this industry in the short run is:

F) $105

A) $86

G) $108

B) $92

H) $110

A) $34

G) $71

C) $95

I) $111

20. This profit earned by each firm in this industry in this short run equilibrium is:

A) $69

B) $72

F) $99

G) $105

H) $110

21. This firm's shut down price is:

C) $53

I) $89

A) $86

G) $108

B) $47

H) $83

C) $87

I) $111

D) $98

J) none of the above

E) $101

C) $95

I) $111

D) $93

E) $96

J) none of the above

D) $56

E) $65

J) none of the above

22. We are now in a new short-run situation with 400 firms in the industry and the same cost

curves described at the beginning of this set of questions. Now, imagine that the industry

demand curve falls to P = 268 - .035Q. When the industry settles down into a new short-run

equilibrium, what will be the new equilibrium price?

B) $92

D) $98

F) $105

H) $110

F) $68

E) $101

J) none of the above

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The manager of Greene Enterprises, Inc., recently estimated its average variable cost (AVC) function to be AVC = 88−0.026Q + 0.000003Q2 Greene Enterprises faces total fixed costs (TFC) of $300,000. At what level of output does average variable cost (AVC) reach its minimum value for Greene Enterprises?arrow_forwardThe company AffordableStuff sells cell phones. The marginal cost for each cell phone is given by the equation C(x) = 0.01x² – 3x + 229. a is the number of cell phones manufactured and sold. The marginal revenue function is R(x) = 429 – 2.x. Both C(x) and R(x) are given in dollars. a) Where do these curves intersect? What do those intersection points mean? b) Find the area between the curves, using end points that make sense. Round to the nearest cent. c) What does the area under the curve mean in this case?arrow_forwardp=D(x)=71.5−0.02xp=D(x)=71.5−0.02x dollars. The total cost for these coffee makers is given by C(x)=0.05x2+5.5x+6200C(x)=0.05x2+5.5x+6200 dollars. Determine the marginal profit for 118 coffee makers.arrow_forward

- A firm’s long-run total cost curve is given by: C(q) = 40q − 10q2 + q3 . Over what range of output does this technology exhibit decreasing returns to scale? Group of answer choices q>8 q<5 None of the above are correct. q>10 q>5 Note: don't use chat botarrow_forwardGiven the total cost equation: TC = 144 +2Q+Q² what is the average cost when the firm produces at the level of Q that yields the minimum average cost?arrow_forwardAt an output level of 100 units a firm has average total costs of $80 and average variable costs of $50. Its total fixed costs are:arrow_forward

- Demand function is given by Q=84-2P and cost function is C(q)=25+2q+q2 1) What are the qualitative features of the costs of this cost function? i.e. average, marginal, variable, properties, and what are the key prices – shut price, breakeven price, revenue maximizing and profit maximizing price? 2) Using this cost structure and demand - how many firms are likely to operate in the long run (note: that in the long run firms tend to operate close to minimum average cost)?arrow_forwardHey need correct answerarrow_forward1a) A firm’s estimated long-run total cost function is LRTC = 160Q - .6Q2 + .002Q3. Suppose the firm is producing 100 units of output. The cost elasticity is ____ You can use Excel spreadsheet or otherwise to answer this question. b) A research study published in Social Science Medicine, “Production Functions for General Hospitals,” estimated the following general hospital production function in the Netherlands: Q = 5*Staff.34*Beds.64*Drugs.04*Specialists.02, where Q is a measure used by the authors for patient care. Suppose a hospital currently utilizes the following inputs: Staff =20, Beds = 120, Drugs = 60, Specialists =10. Use a spreadsheet to find the following or otherwise. If the hospital increases its specialists by one (1), that is, employs an 11th specialist, the increase in Q (marginal product) will be: c) A study published in Social Science Medicine, “Production Functions for General Hospitals,” estimated the following general hospital production function: Q =…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education