ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

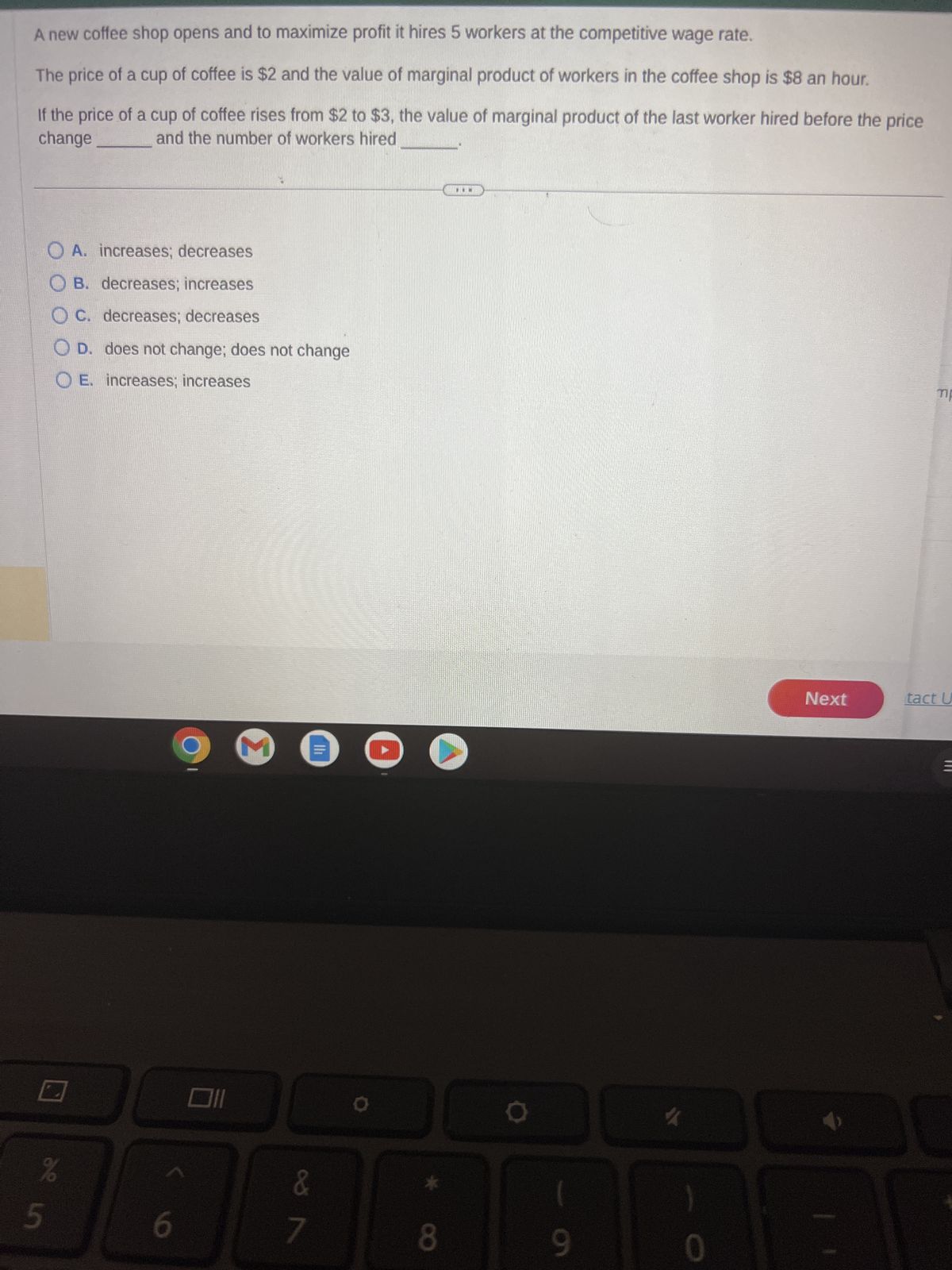

Transcribed Image Text:A new coffee shop opens and to maximize profit it hires 5 workers at the competitive wage rate.

The price of a cup of coffee is $2 and the value of marginal product of workers in the coffee shop is $8 an hour.

If the price of a cup of coffee rises from $2 to $3, the value of marginal product of the last worker hired before the price

change

and the number of workers hired

de in

%

5

A. increases; decreases

B. decreases; increases

C. decreases; decreases

D. does not change; does not change

E. increases; increases

C

6

M

&

7

8

O

1

9

0

Next

TIP

tact U

=

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider a perfectly competitive firm that uses labor as an input. The firm faces a market price of $10 for each unit of its output. The total product, and the marginal product of labor that the firm receives from hiring 1 to 5 workers are reported in the table below. What is the value of the marginal product of labor (VMP) for the first worker? Value of the Marginal Product of Labor Labor input (# workers) Total product (# goods) Marginal Product of Labor (MPL) 1 17 18 13 |22 4 25 3 26 Provide your answer below:arrow_forwardLabor (workers per day) Total Product (per day) 10 4000 11 4389 12 4752 13 5083 14 5376 15 5625 The firm can hire as many workers as they want at the prevailing market wage of $150 a day per worker. In addition, the firm pays $200 a day for equipment. Enter ONLY numbers. No comma, units, or decimals. 1. What is the marginal product of the 12th worker? 2. What is the average product of hiring 12 workers? 3. What is the total variable cost per day if 12 workers are hired ? 4. What is the total fixed cost per day if 12 workers are hired?arrow_forwardSuppose Kara maximizes her profits by hiring workers to produce hand-made soaps. Her soaps sell for $1 each. How should Kara decide on how many workers she should hire? a.Hire workers up to the point when the price of her soaps starts to fall from $1 b.Hire workers up to the point when the total product of all her workers is at its maximum c.Hire up to the point when the wage rate equals to the value of the marginal product of the last worker hired d.Hire up to the point when the marginal product of the last worker hired is equal to zeroarrow_forward

- I need it in one hourarrow_forwardRead the "Clear it Up: Do Profit Maximizing Employers Exploit Labor" Do Profit Maximizing Employers Exploit Labor? (Source: OER) If you look back at the labor dynamics of supply and demand, you will see that only the firm pays the last worker it hires what they’re worth to the firm. Every other worker brings in more revenue than the firm pays him or her. This has sometimes led to the claim that employers exploit workers because they do not pay workers what they are worth. Let’s think about this claim. The first worker is worth $x to the firm, and the second worker is worth $y, but why are they worth that much? It is because of the capital and technology with which they work. The difference between workers’ worth and their compensation goes to pay for the capital, technology, without which the workers wouldn’t have a job. The difference also goes to the employer’s profit, without which the firm would close and workers wouldn’t have a job. The firm may be earning excessive profits,…arrow_forwardNonearrow_forward

- You own a farm, you hire labor and capital to produce apples. The marginal product of the last unit of labor input is 15 and the marginal product of the last unit of capital input is 45. The market wage for labor is SB. If you are using the optimal combination of inputs, then the price of capital is? Select one: a. $45 Ob. $24 c. $360 Od. $3arrow_forwardplease also do the graph thank youarrow_forwardOnly typed answerarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education