ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

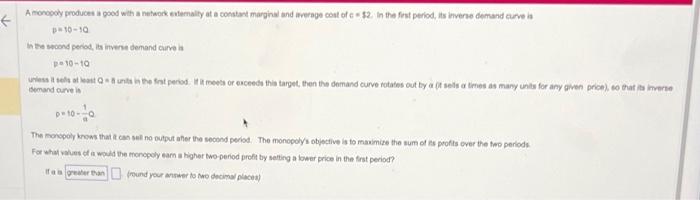

Transcribed Image Text:A monopoly produces a good with a network externality at a constant marginal and average cost of c-$2. In the first period, its inverse demand curve is

←

p10-10

in the second period, its inverse demand curve is

p-10-10

unless it sels at least Q 8 units in the first period. If it meets or exceeds this target, then the demand curve rotates out by a (t sells a times as many units for any given price), so that its inverse

demand curve is

The monopoly knows that it can sell no output after the second period. The monopoly's objective is to maximize the sum of its profits over the two periods.

For what values of it would the monopoly earn a higher two-period profit by setting a lower price in the first period?

Ifa is greater than

(round your answer to two decimal places)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A healthcare provider - that is a monopoly - faces the following market demand schedule: P 100 90 80 70 60 50 40 30 20 10 0 Q 2000 2500 3000 3500 4000 4500 5000 5500 6000 6500 7000 What is the maximum profit assuming that each unit costs $30 for the firm to produce and there are no other costs of production?arrow_forwardFigure 15-4 Price Curve C Curve D P5 P4 P3 P2 P1 PO Curve B Curve A +d ed tdid Quantity Refer to Figure 15-4. A profit-maximizing monopoly's total revenue is equal to Р3 х Q4. (P4-P2) x Q3. Р4х Q3. P5 x Q1.arrow_forwardWhat is the deadweightloss?Explain how monopoly creates a deadweightloss. b) Draw and compare the price and the output of a monopoly with the competitive market. Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forward

- There is an efficiency in the monopoly market. Define why. Pls explain in easy words.arrow_forwardReview the graph at right for a monopoly market (enter all of your responses as whole numbers). Price 100- How much is the consumer surplus? S 90- MC How much is the producer surplus? s 80- 70- How much is the deadweight loss? S 60 80- Monopoly total surplus is $ 50- Monopoly total surplus is V competitive total surplus. 40- 30- 20- 10- MR D 10 30 40 50 60 70 90 100 Quantityarrow_forwardFigure 15-3 ↑ Price P4 P3 P2 Pl PO Curve C Curve B Curve D Curve A 20/1/02 03 04 Refer to Figure 15-3. The marginal cost curve for a monopoly firm is depicted by curve a. D. b. A. c. B. d. C. Quantityarrow_forward

- Only typed answer and don't use chatgpt . B) A monopoly has two production plants with cost functions C1 = 50 + 0.1Q12 and C2 = 30 + 0.05Q22. The demand it faces is Q = 500 - 10P. What is the profit-maximizing price?arrow_forwardDON'T COPY FROM CHEGG OR I WLL GIVE YOU A DISLIKE AND REPORT YOU,arrow_forwardExercise A.9. Define natural monopoly. What does the size of the market have to do with whether an industry is a natural monopoly?arrow_forward

- For the monopoly shown above, which of the following best describes its practices? Price, Costs MC ATC D P3. P2. P1 MR Q2 Q1 Demand Quantity OA Operating with profit of area AP1ED OB. Operating at a loss of area ABEC C. Shutting down OD, Breaking even, with a deadweight loss to society of area DCE DE. Operating with profit area ADEP1 and deadweight loss to society of area DCEarrow_forwardShow that a monopoly will not necessarily lower its price by the same percentage as its constant marginal cost drops: 1.) Use the point drawing tool to indicate the initial equilibrium price and quantity. Label this point 'E'. 2.) Use the line drawing tool to show a 50 percent decrease in marginal cost. Label this line 'MC₁'. 3.) Use the point drawing tool to indicate the new equilibrium price and quantity. Label this point 'E,'. Carefully follow the instructions above, and only draw the required objects. What is the percentage change in the price given a 50 percent decrease in marginal cost? The price decreased by percent. (round your answer to two decimal places) 50- 45- 40 35- 30- 25- 20-1 15- 10- 5 Price, P 10 20 30 -MC MR D 40 50 60 70 80 90 100 Quantity, Qarrow_forwardWhy is this true?: When a monopoly chooses a quanity or price combination that is on the price inelastic portion of the linear market demand cuve, it is not maximizing profit. Explain why.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education