ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

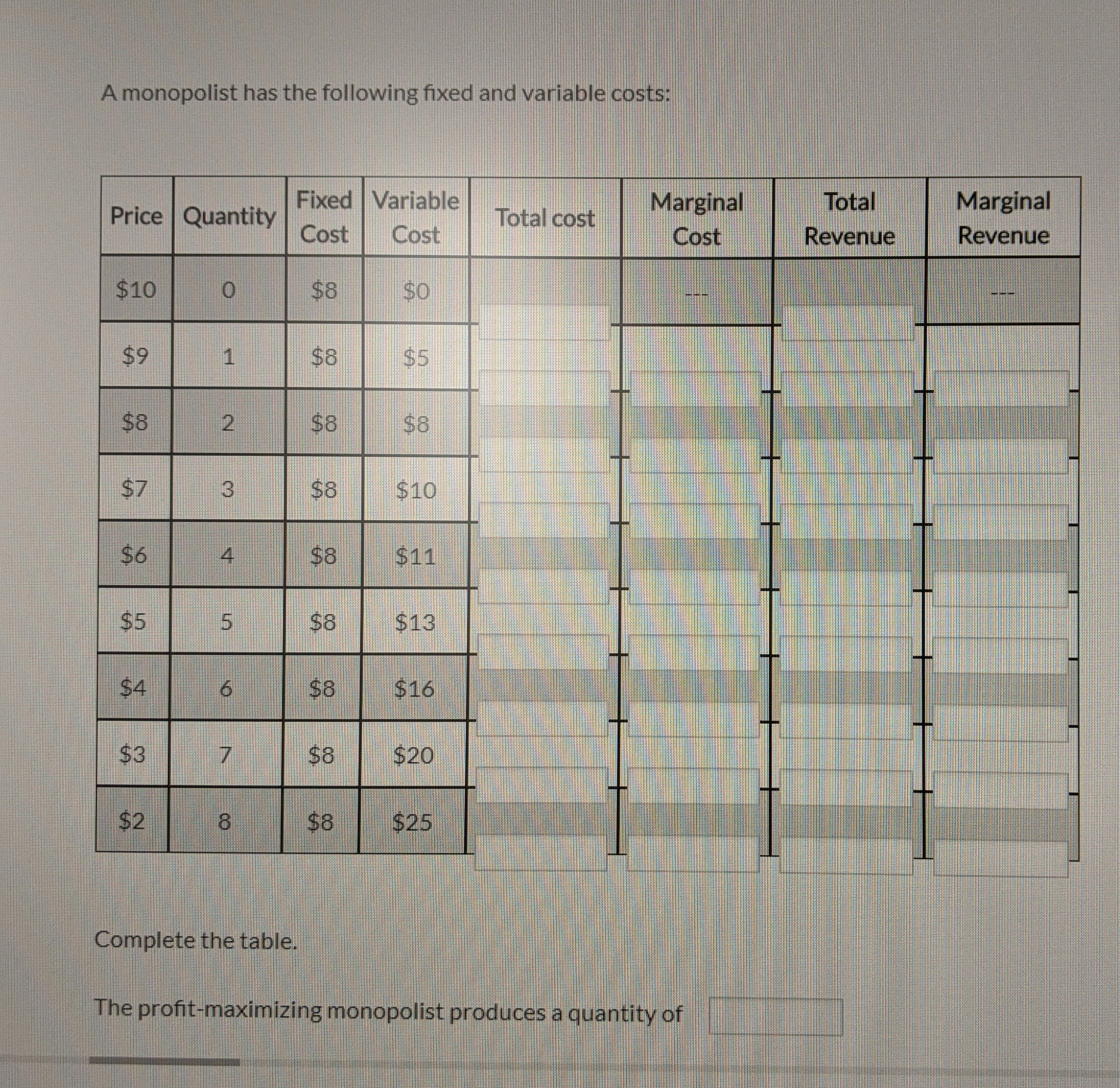

Transcribed Image Text:A monopolist has the following fixed and variable costs:

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Assume quantities need not be integers. Assume a profit maximizing monopolist with marginal cost equal to $4 faces demand MWTP(Q) = 14 - 2Q. Assuming it must charge the same price for each unit it sells, what is elasticity of demand at the price it chooses?arrow_forwardA single-price monopolist has the following equations representing its marginal cost and demand curves: Qd=800-1/3 P MC = 2Q What is the deadweight loss caused by this single-price monopoly?arrow_forwardWhat is a likely reason that a small but growing firm may experience economies of scale? Selected answer will be automatically saved. For keyboard navigation, press up/down arrow keys to select an answer. a b C Question 29 d The firm starts to pay its workers less. Managers become less effective at oversight. The firm has to create an HR department. Larger-volume equipment can be used.arrow_forward

- A monopolist firm faces a demand with constant elasticity of -2.0. It has a constant marginal cost of $20 per unit and sets a price to maximize profit. If marginal cost should increase by 25 percent, would the price charged also rise by 25 percent?arrow_forwardA monopolist has four distinct groups of customers: group A has an elasticity of demand of 0.2, group B has an elasticity of demand of 0.8, group C has an elasticity of demand of 1.0, and group D has an elasticity of demand of 2.0. The group paying the highest price for the product will be group: a) D. b) C. c) B. d) A.arrow_forwardFind the economic profit of a monopolist using the following information: Demand: p = 110-2Q Fixed cost: FC = 120 Marginal cost: MC = 10arrow_forward

- A single-price monopolist is only one seller in the market by definition. This means that the monopolist sets the price and the quantity in order to maximize its profit, regardless of the elasticity of the demand. True Falsearrow_forwardA monopolist has decreasing average costs as output increases. If the monopolist sets price equal to average cost, it will produce too little output from the standpoint of efficiency. maximize its profits. lose money. produce too much output from the standpoint of efficiency.arrow_forwardHow, if at all, will a monopolist respond to a rise in the price of an input? (provide explanation with graphs)arrow_forward

- The supply curve for a monopolist is always positively sloped.arrow_forwardGiven the same costs, the monopolist produces less output and charges a higher price compared to the purely competitive industry. What makes this possible for the monopolist and not the purely competitive industry? What is the impact on the society of each?arrow_forwardA monopolist maximizes profit by producing: Group of answer choices on the inelastic portion of the demand curve at the level where average cost is minimized at the point where the cost of producing the last unit of output equals price. at the output level where marginal revenue equals marginal cost at the level where the deadweight loss is minimized.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education