ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Fill in blanks in picture...

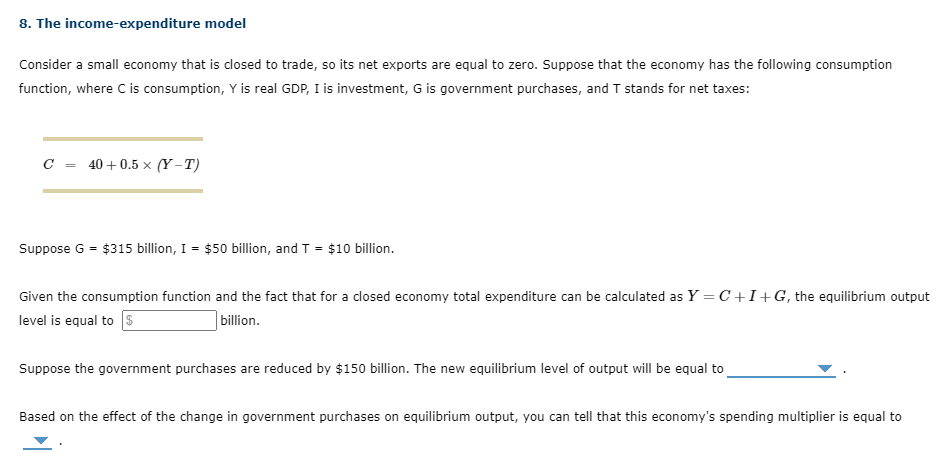

Transcribed Image Text:8. The income-expenditure model

Consider a small economy that is closed to trade, so its net exports are equal to zero. Suppose that the economy has the following consumption

function, where C is consumption, Y is real GDP, I is investment, G is government purchases, and T stands for net taxes:

C = 40+0.5 ×x (Y –T)

Suppose G = $315 billion, I = $50 billion, and T = $10 billion.

Given the consumption function and the fact that for a closed economy total expenditure can be calculated as Y =C +I+G, the equilibrium output

level is equal to s

billion.

Suppose the government purchases are reduced by $150o billion. The new equilibrium level of output will be equal to

Based on the effect of the change in government purchases on equilibrium output, you can tell that this economy's spending multiplier is equal to

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Classkick Dashboard M about the teen hype - musami M Inbox - rashid.tasnim2005.15 x + A app.classkick.com/#/student/ZHEQZS/tasnim%20rashid/2 A ZHE QZS Supply Practice T 2/4 6. Make a prediction: What would happen to the graph if the price of shampoo doubled? A 5:33arrow_forwardUsing the three-point curved line drawing tool, draw the Engel curve for food. Label this curve 'Engel Curve'. Carefully follow the instructions above, and only draw the required object.arrow_forwardThe question says Olivias favorite Mexican snacks include flautas and sopapitas. If her $12 budget is represented in the graph The price of flauta is ___ and sopapitas is ___? Select one a. $2 ; $4 b.$3 ; $4 c.$4 ; $3 d.$6 ; $3 Graph is given.arrow_forward

- One Analyze the effect of each scenario on the price of khaki pants. Consider the following scenarios. Think about how each scenario would affect the price of khaki pants. A new technology reduces the time it takes to make a pair of khaki pants. The price of the cloth used to make khaki pants falls. The wage rate paid to garment workers increases. The price of jeans increases. People's incomes increase.arrow_forwardThere is a market for Purses. There is a decrease in the cost of leather. Describe and graph the next scenario.arrow_forwardWhat is the difference between a "need" and a "value?"arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education