ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

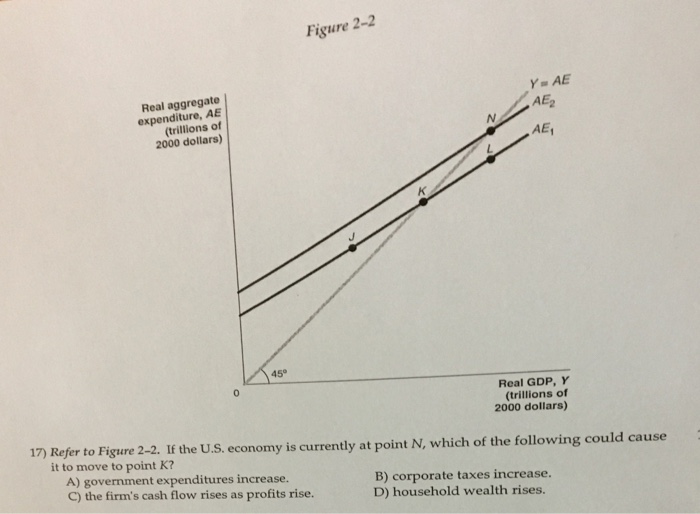

Transcribed Image Text:Real aggregate

expenditure, AE

(trillions of

2000 dollars)

0

45°

Figure 2-2

N

A) government expenditures increase.

C) the firm's cash flow rises as profits rise.

Y = AE

AE₂

AE₁

Real GDP, Y

(trillions of

2000 dollars)

17) Refer to Figure 2-2. If the U.S. economy is currently at point N, which of the following could cause

it to move to point K?

B) corporate taxes increase.

D) household wealth rises.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Question 1: Specific Factors Model Let assume, you live in an economy where two goods are being produced (say x and y) and labor can be allocated in the production of either good freely, but the other factor is specific. For your more information, good “x” can be produced with labor and capital and good “y” can be produced with labor and land. Given the situation, a) How much does the each good the economy produced? b) How much labor will be employed in each sector?arrow_forwardScenario 1: The economy enters a recession driving down the demand for homes nationwide.arrow_forward1. Supply and demand in the neoclassical economy Consider an economy in which the consumption, investment and production functions are as follows. C = 90 + 0.7(Y − T) I = 250 − 20r F(K, L) = AK0.5L0.5 The capital and labor supply are equal to 100 each, A=10, G = 200 and T = 200. Compute the equilibrium values of output, overall labor income, consumption, public savings, national savings, investment, and the interest rate. Suppose now government spending increases to G=300 (everything else stays the same). What happens to output, consumption, savings, investment and the interest rate? Compute the new values for these variables.arrow_forward

- The tax cuts of 2008 and 2009 reduced the disposable income of U.S. consumers. True or Falsearrow_forward(b) Assume that household income increases as a result of recent economic prosperity in Country X. On your graph in part (a), show the effect of the increase in household income on real output and the price level.arrow_forwardPlease provide answer in 1 hrarrow_forward

- Exercise 4. You are a manager at a certain factory that designs small gadgets. The factory has been quite successful in the past years. Your CEO is wondering whether or not it is a good idea to expand the factory this year. The cost to expand the factory is $1.5M. Doing nothing will result in expected $3M in revenue if the economy stays good and people continue to buy plenty of gadgets, but only $1M in revenue is expected if the economy is bad. On the other hand, expanding the factory carries an expected $6M in revenue if economy is good and $2M if the economy is bad. Assume there is a 40% chance of a good economy and a 60% chance of a bad economy. Also, assume the costs of operating the factory account to $.5M if the factory is expanded and $.3M if not. a. Illustrate a Decision Tree showing these choices. b. What should you do?arrow_forwardQUESTION 5 (a) What are some criticisms against the Keynesian model? How do post Keynesian models try to address? (b) Graphically illustrate and explain the conditions for a competitive general equilibrium (c) Graphically illustrate and explain the effect of an increase in government spending on general equilibrium conditions.arrow_forwardThe figure below shows the average share of total household expenses for a good and the inflation-adjusted price of the same good. The share of all expenses line is calculated as expenditures on this good (that is the price of this good multiplied by the quantity of this good purchased) divided by total household expenses. This line shows how expenditures on this good changes over time, holding total spending constant. The other line is the price of this good adjusted for inflation (i.e., the increase in the price level for all goods). The specific units are obscured on purpose. Use these data to characterize the price elasticity of demand. Explain using the definitions of price elasticity of demand and total expenditure. Notice that I am not asking you to calculate the price elasticity of demand. Use the data to talk about the size of price elasticity of demand in general terms. Is demand elastic or inelastic? Is the price elasticity of demand very large? Very small? Close to 1?…arrow_forward

- Suppose we start with a general equilibrium, and the economy experience an improvement in payment technology. Which of the following statements correctly describes the goods market response in the short term? 1. The IS curve remains unchanged 2. The IS curve shifts to the left 3. The IS curve shifts to the right 4. None of the abovearrow_forwardWhich of the following questions would be studied in the area of microeconomics? Select one: a. What determines the number of hours an individual works? b. Do interest rates affect net exports? c. Will an increase in government spending cause inflation? d. What portion of total spending comes from households in the economy?arrow_forwardWhich of the following statements is true? An individual's future spending decreases when she lends money. An individual's future spending increases when she borrows money. An economic agent borrows to move her spending from the future to the present. An economic agent borrows to move her spending from the present to the future. Loss aversion refers to the idea that people ________. generally tend to avoid risky activities are more prone to making losses than gains in day-to-day transactions psychologically weight a loss more heavily than they psychologically weight a gain are unwilling to undertake expenditures that reduce the probability of future losses Which of the following is an example of adverse selection? Overgrazing of a common piece of land A passenger traveling in a subway without a ticket A customer buying a defective appliance from a used goods market The generation of hazardous waste by the production of a good More people started building houses in the…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education