ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

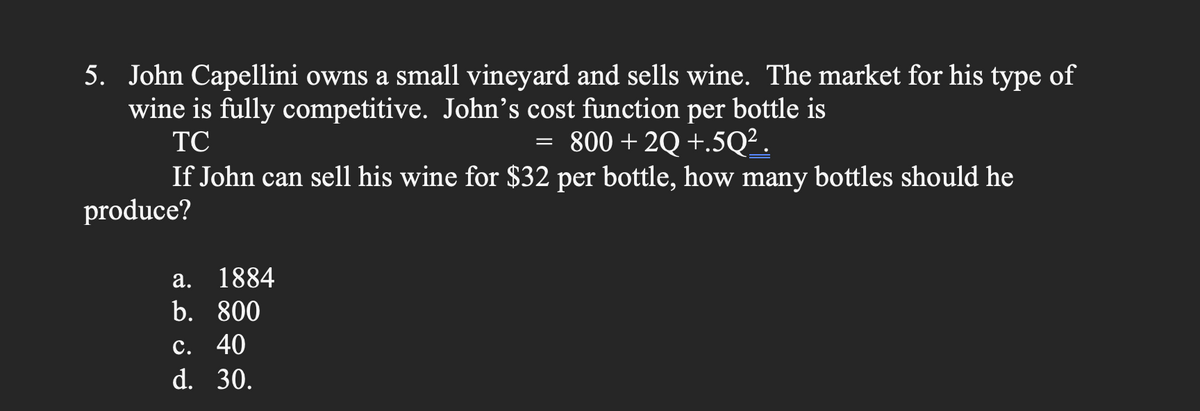

Transcribed Image Text:5. John Capellini owns a small vineyard and sells wine. The market for his type of

wine is fully competitive. John's cost function per bottle is

TC

= 800 +2Q +.5Q².

If John can sell his wine for $32 per bottle, how many bottles should he

produce?

a. 1884

b. 800

c. 40

d. 30.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- $11.00 MC| $10.00 $9.00 ATC $8.00 $7.00 TRAVCI $6.00 $5.00 $4.00 $3.00 2 3 7 9 10 Quantity of Output (q) Pierre is a photographer in a perfectly competitive market. The graph shown above gives his MC, ATC and AVC curves. Suppose the market price is $10.50. How much profit does Pierre make? 22.5 24 20 O18 S per unitarrow_forwardOnly typed answerarrow_forwardA firm is selling apples is profit-maximizing, but they're in a constant cost industry. The industry is perfectly competitive and currently in long-run equilibrium. Assume apples are a normal good and consumer income falls, and the firm continues to produce. 1. Illustrate the decrease in income in the short run with a cost curves graph. Make sure to highlight the area of loss.arrow_forward

- Gg.227.arrow_forward10. Read this excerpt from the October 18, 2022, Wall Street Journal. KINDERHOOK, N.Y.—Golden Harvest Farms has grown from a small apple-growing operation when Doug Grout’s grandfather opened it after World War II, to a multipronged business that includes a retail stand, cider press, distillery, tasting room and barbecue restaurant. But Mr. Grout said he sees a cloudier future for the business due to new state regulations that will require him to increasingly pay more overtime to the farmworkers who pick his apples in the coming years, raising one of his primary costs. “We were looking to buy another orchard, and that whole thing is tabled,” said Mr. Grout, 52 years old, who co-owns Golden Harvest with his father, as he drove between rows of Honeycrisp trees. “We’re stepping away. You’re going to see farms go out of business. This is very shortsighted.” For the apple market in New York, the new regulations will: Cause supply to shift to the left, leading to higher prices and a…arrow_forwardPlease follow instructions and follow graph. Show workarrow_forward

- Hello, this is a microeconomics question. Please use a drawing of a relevant graph to explain how does perfect competition ensure allocative efficiency? Not sure if I'm supposed to use this graph, but if i am please use it as reference when making your explantion to the question of how does perfect competition ensure allocative efficiencyarrow_forward5 MC MR ← PREVIOUS 50 Answer here ATC D What is the profit-maximizing level of output? 10arrow_forwardO Farmer Brown grows peaches in Georgia. Suppose the market for peaches is perfectly competitive and that the market price for a box of peaches is $32 per box. Farmer Brown's marginal cost of production is illustrated in the table. Boxes of Peaches Market Price (per box) Marginal Cost (MC) 0 $32 1 32 10.00 2 32 5.00 3 32 15.00 4 32 30.00 5 32 60.00 6 32 90.00 What price will farmer Brown charge when maximizing profit? Farmer Brown will charge a price of $☐ per box of peaches. (Enter your response as an integer.) What is farmer Brown's profit-maximizing level of output? Farmer Brown maximizes profit when producing boxes of peaches. (Enter your response as an integer.) Time Remaining: 01:15:52 Nextarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education