ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:52

01:16:34

P

55

51

°

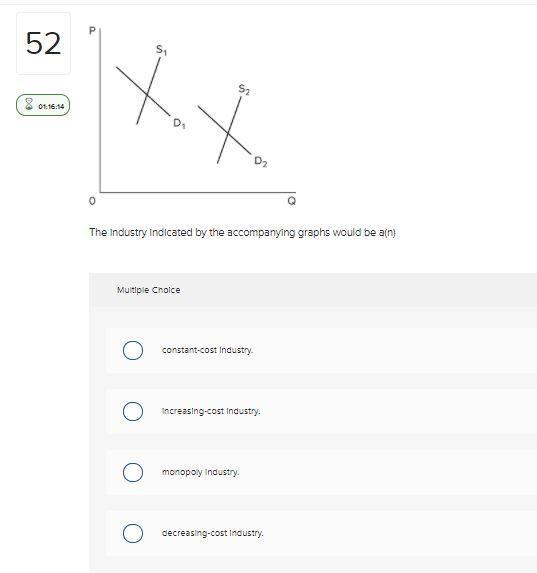

The Industry Indicated by the accompanying graphs would be a(n)

Multiple Choice

о

constant-cost Industry.

Increasing-cost Industry.

monopoly Industry.

decreasing-cost Industry.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Answer choices are first blank: negative, positive, zero second blank: an equal number of, fewer, morearrow_forwardMonopolistic competitive firms' profit maximization decisions are similar to those of a perfectly competitive firm. a monopoly firm. both monopoly and perfectly competitive firms. neither monopoly nor perfectly competitive firms.arrow_forwardAssume an oligopolist confronts two possible demand curves for its own output, as illustrated below. The first (A) prevails if other oligopolists don't match price changes. The second (B) prevails if rivals do match price changes. Price (dollars per unit) 19- 17 Demand B 15- Demand A 13- 11. 8 10 12 14 16 18 20 Quantity (units per period) (a) By how much does quantity demanded increase if price is reduced from $11 to $9 and Instructions: Enter your responses rounded to the nearest whole number. (i) Rivals match the price cut? (ii) Rivals don't match the price cut? (b) By how much does quantity demanded decrease when price is raised from $11 to $15 and Instructions: Enter your responses rounded to the nearest whole number (do not include negative signs). (i) Rivals match the price hike? (ii) Rivals don't match the price hike?arrow_forward

- (1C) Individual profit earned by Dave, the oligopolist, depends on which of the following? (i) (ii) (iii) The quantity of output that Dave produces The quantities of output that the other firms in the market produce The extent of collusion between Dave and the other firms in the market a. (i) and (ii) b. (ii) and (iii) c. (iii) only d. (i), (ii), and (iii) Answer for Question 1C: (1D) Cameron lives in an apartment building and gets a $700 benefit from playing his stereo. Renee, who lives next door to Cameron and often loses sleep due to the music coming from Cameron's stereo, bears a $1,000 cost from the noise. At which of the following offers from Renee could both Renee and Cameron benefit from the silencing of Cameron's stereo? a. $250 b. $550 c. $750 d. $1,020 Answer for Question 1D: (1E) The market for Wellesley-branded refrigerator magnets has the following demand and supply curves respectively: QD = 16 – P and Q$ = 2*P – 8. The Town of Wellesley decides to impose a price of…arrow_forwardThe graph shown represents the cost and revenue curves faced by a monopoly. 22 P3 P2 P1 PO MC ATC Q1 Q2 MR Which of the following statements is true? 1. The outcome in a monopoly market would be Q1, P1. II. The outcome in a perfectly competitive market would be Q2, P2. III. The efficient outcome is Q2, P2. Multiple Choice I and II only ○ I only II and Ill only I, II, and III barrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education