Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

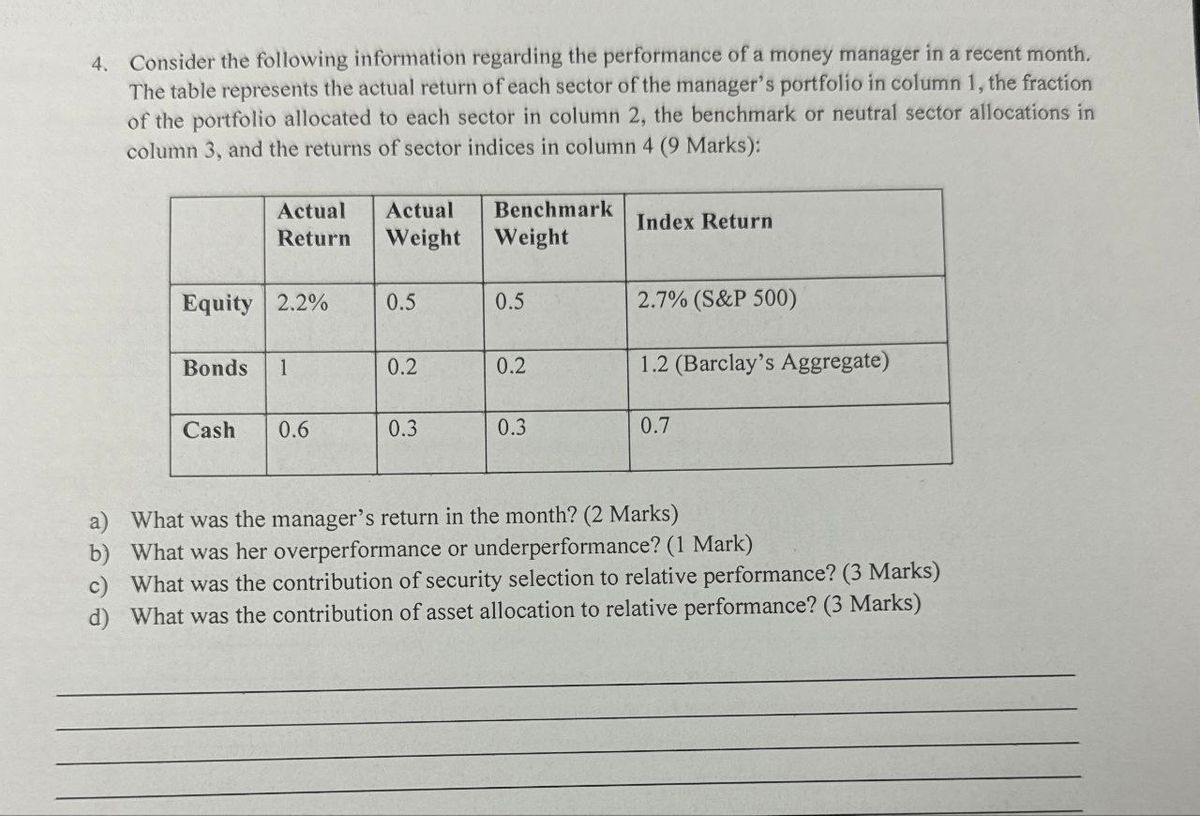

Transcribed Image Text:4. Consider the following information regarding the performance of a money manager in a recent month.

The table represents the actual return of each sector of the manager's portfolio in column 1, the fraction

of the portfolio allocated to each sector in column 2, the benchmark or neutral sector allocations in

column 3, and the returns of sector indices in column 4 (9 Marks):

Actual

Return

Actual

Weight

Benchmark

Weight

Index Return

Equity 2.2% 0.5

0.5

2.7% (S&P 500)

Bonds 1

0.2

0.2

1.2 (Barclay's Aggregate)

Cash

0.6

0.3

0.3

0.7

a) What was the manager's return in the month? (2 Marks)

b) What was her overperformance or underperformance? (1 Mark)

What was the contribution of security selection to relative performance? (3 Marks)

d) What was the contribution of asset allocation to relative performance? (3 Marks)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- Consider the following performance attribution data. Weight Style Category Large-cap growth Mid-cap growth Small-cap growth What is the Allocation Effect? Primo 0.60 0.15 0.25 Benchmark 0.50 0.40 0.10 Primo 17% 24 20 Return Benchmark 16% 26 18arrow_forwardAn insurance company’s projected loss ratio is 79.53 percent, and its loss adjustment expense ratio is 7.51 percent. It estimates that commission payments and dividends to policyholders will add another 13.96 percent. What is the minimum yield on investments required in order to maintain a positive operating ratio? (Do not round intermediate calculations. Round your answers to 2 decimal places. (e.g., 32.16))arrow_forwardi need the answer quicklyarrow_forward

- Consider the following information regarding the performance of a money manager in a recent month. The table represents the actual return of each sector of the manager's portfolio in column 1 , the fraction of the portfolio allocated to each sector in column 2 , the benchmark or neutral sector allocations in column 3 , and the returns of sector indices in column 4. \table[[,Actual,Benchmark],[Return,Actual Weight,Weight,Index Return,],[Equity,2.2%,0.4,0.5,2.7%arrow_forwardI need helparrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education