Principles of Macroeconomics (MindTap Course List)

8th Edition

ISBN: 9781305971509

Author: N. Gregory Mankiw

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Related questions

Question

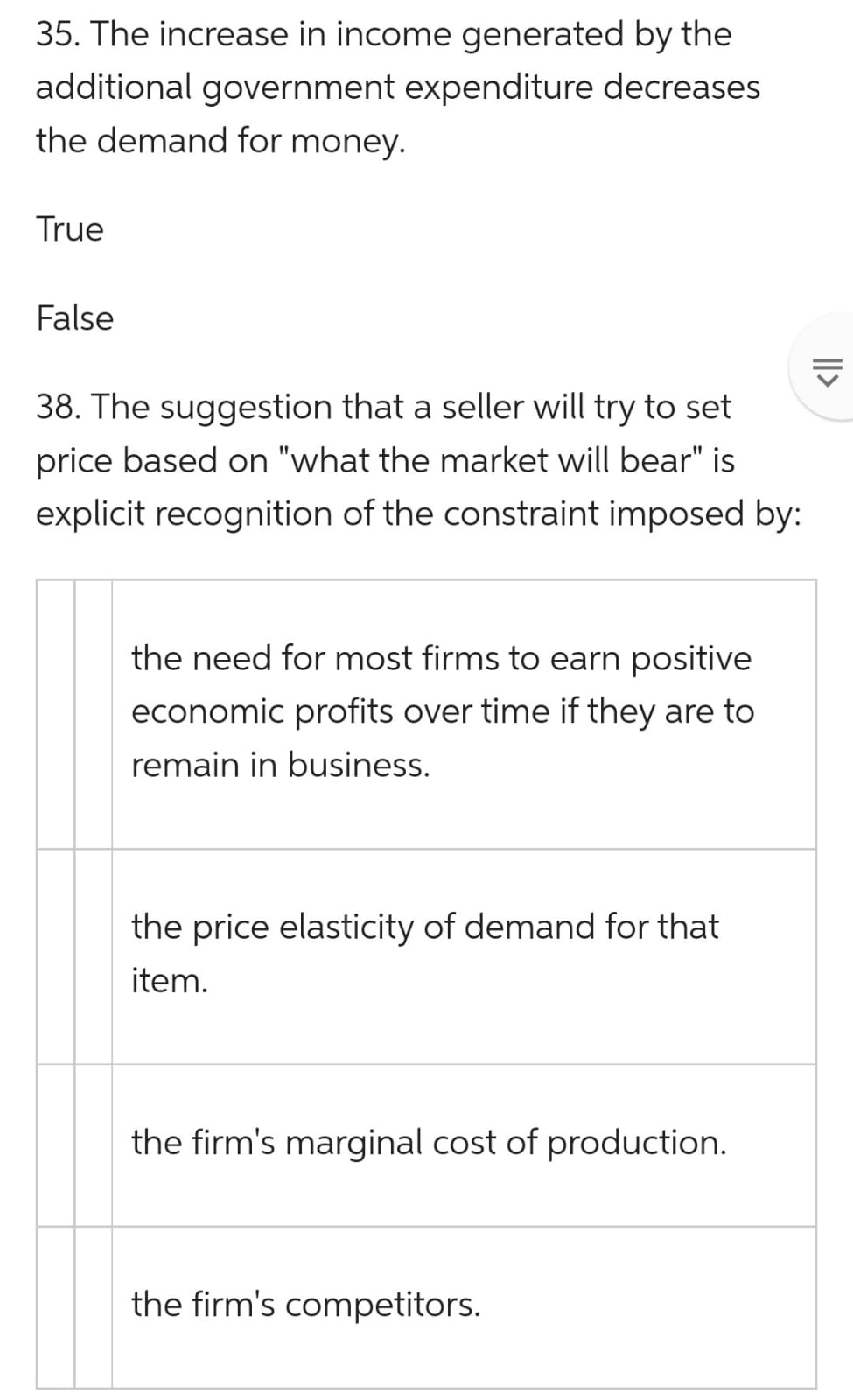

Transcribed Image Text:35. The increase in income generated by the

additional government expenditure decreases

the demand for money.

True

False

38. The suggestion that a seller will try to set

price based on "what the market will bear" is

explicit recognition of the constraint imposed by:

the need for most firms to earn positive

economic profits over time if they are to

remain in business.

the price elasticity of demand for that

item.

the firm's marginal cost of production.

the firm's competitors.

||>

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 14. Demand for factors of production is A. O Derived demand B. O Joint demand C. O Composite demand D. O None of the abovearrow_forwardThe DoorCo Corporation is a leading manufacturer of garage doors. All doors are manufactured in their plant in Carmel, Indiana, and shipped to distribution centers or major customers. DoorCo recently acquired another manufacturer of garage doors, Wisconsin Door, and is considering moving its wood door operations to the Wisconsin plant. Key considerations in this decision are the transportation, labor, and production costs at the two plants. Complicating matters is the fact that marketing is predicting a decline in the demand for wood doors. The company developed three scenarios and determined the total costs under each decision and scenario, which are given in the accompanying tables. Complete parts a through c. Click here to view the scenarios. Click here to view the total costs. a. What decision should DoorCo make using the aggressive strategy? Select the correct choice below and fill in the answer box to complete your choice. O A. DoorCo should move to Wisconsin because it has the…arrow_forwardQuestion 3 Question 6 $19 16 Question 16 13 10 30 0 Total Product Assume that supply of a product increases while the demand for it decreases. Then, the equilibrium quantity will, 100 160180 210 Quantity In order to maximize profits, this firm should charge $ Average Fixed Average Variabile Cost Cost $100.00 33.33 25.00 Question 11 2.5 points Save An Paris has a weekly income that she spends on two goods: fast food meals and sugary drinks. If she spends all her money on fast food meals, she can buy 8 of them. If she spends all her money on sugary drinks, she can buy 9 of them. Calculate the opportunity cost of one y drink (in terms of fast food meals) your answers as a number with 2 c (like 2.38 or 1.00 or 9.35) as your answer. 16.01 14.2% 12.50 11.11 10.00 $17.00 16.00 15.00 14.00 14.00 15.71 17.50 19.44 Average Total Cost $117.00 66.00 MC 34.00 30.67 SO 30.00 30.55 31.60 33.09 MR Marginal Cost $17 ATC 1.5 points (choose one and write it out exactly as it is written: increase,…arrow_forward

- 15.Over time, housing shortages caused by r ent control AREA MAJID A increase, because the demand and su PAREA MAJID pply curves for housing are more inela stic in the long run. MAJID B decrease, because the demand and s MAJID upply curves for housing are more inel astic in the long run. C change very little since price is not all owed to adjust. AD D increase, because the demand and su pply curves for housing are more elas tic in the long run.arrow_forwardD. the supply curve for the producl a business produces shifts to the left 6. If wages decreased in the labor market, what likely caused it? * A. a surplus of workers O B. a shortage of workers -C. increased union membership OD. unemployment rates decreased 7.If the government were to increase the minimum wage, what might be al unintended consequence? O Oarrow_forwardomework 4 - Compatibility Mode O Seah Joseph References Mailings Review View Help Table Design Layout A A Aa A 三 T AaBbCcI AaBbCcI AaBbC AaB AaBbCcC A D- A 三三三三|三。 田 1 Normal 1 No Spac. Heading 1 Title Subtitle Paragraph Styles 3. The supply and demand schedules below describe the market for compact fluorescent lightbulbs (CFLS). Demand Same Supply Q now at higher price with tax (millions) 200 Price + Supply (millions) Price (millions) tax $2.00 400 200 $2.50 350 250 250 $3.00 300 300 300 $3.50 250 350 350 $4.00 200 400 400 $4.50 150 450 450 $5.00 100 500 500 a. Graph the supply and demand curves, drawing them to scale. i. What is the equilibrium price? ii. What is the equilibrium quantity? Focus hp ho fg 144arrow_forward

- i need help graphing the revenue in 2019 the purple thing on the graph, and using the black pont cross symbol indicating the point of demand curve at 100$ Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism.Answer completely.You will get up vote for sure.arrow_forward* Mind Tap - Cengage Learng ck here to access Mindtap E MINDTAP cer 3 S/D shifts ment: HWK 4 Chapter 3 S/D shifts Assignment Score: 0.00% Save Submit Assignment for Grading ns a2ec13r.03.084 Question 1 of 10 » An increase in the expected price of corn would likely do the following to the current supply and demand for corn: a. increase the demand, but decrease the supply. b. decrease both the demand and the supply. c. increase both the demand and the supply. d. increase the supply, but decrease the demand.arrow_forward4. Mr. Mullet’s Carnival Mr. Mullet runs a traveling carnival that hires local workers in each city it vis- its. The demand for carnival activities is uncertain, with low or high demand equally likely in any given city. At the end of the year, Mr. Mullet reviews his financial records and discovers some puzzling differences between his experi- ences in small and large cities. He always paid the same wage in large cities ($9), but paid different wages in small cities ($6 or $12). He always hired the same quantity of labor in small cities (20 workers), but different quantities in big cities (10 or 30 workers). a. Using Figure 3–3 as a model, illustrate with two graphs, one for the typical small city and one for the typical big city. Assume that the demand curves for labor are linear and parallel, with vertical intercepts of $18 (high de- mand) and $12 (low demand). In the typical big city with high demand, profit is In the typical big city with low demand, profit is…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Principles of Macroeconomics (MindTap Course List)EconomicsISBN:9781305971509Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Macroeconomics (MindTap Course List)

Economics

ISBN:9781305971509

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Principles of Economics 2e

Economics

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:OpenStax

Essentials of Economics (MindTap Course List)

Economics

ISBN:9781337091992

Author:N. Gregory Mankiw

Publisher:Cengage Learning