ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

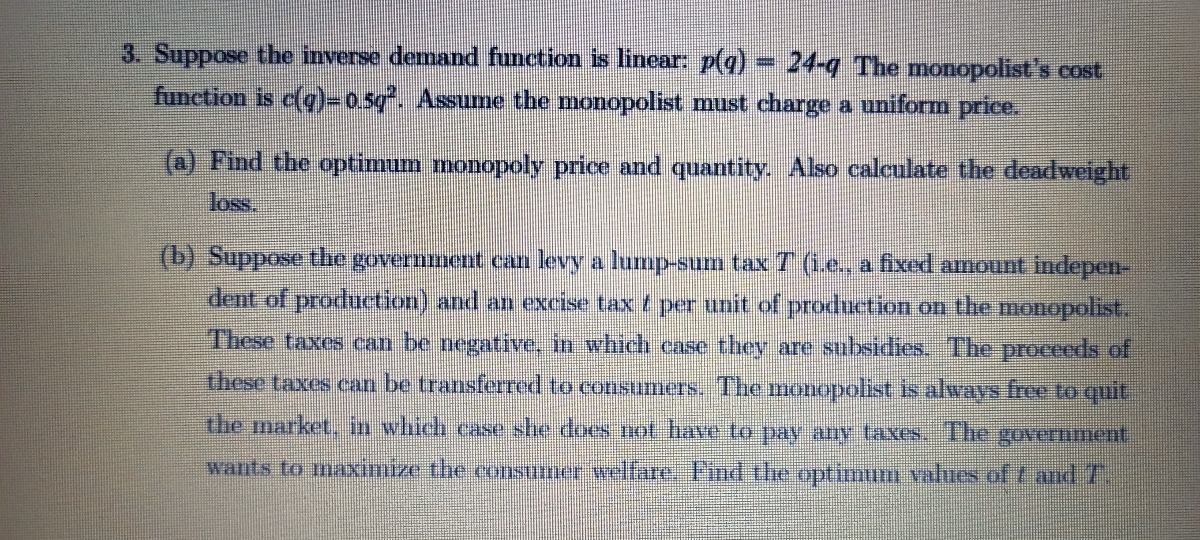

Transcribed Image Text:3. Suppose the inverse demand function is linear: p(q) = 24-q The monopolist's cost

%3D

function is c(g)-0.5g*. Assume the monopolist must charge a uniform price.

(a) Find the optimum monopoly price and quantity. Also calculate the deadweight

loss.

(b) Suppose the governmet can levy a lump-sum tax T (i.e., a fixed amount indepen-

dent of produetion) and an excise tax t per unit of production on the monopolist.

These taxes can be negative, in which case they are subsidies. The proceeds of

these taxes can be transferred to consumers. The monopolist is always free to quit

the market, in which case she does not have to pay any taxes. The government

wants to maximize the ensumer welfare: Pind the optimum vaues of t and

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A monopolist has a cost function given by C(y)=y2 and faces a demand curve given by P(y) = 120-y. If you impose a lump sum tax of £100 on this monopolist, what will be the impact on output? Explain your calculations and the intuition behind your result.arrow_forwardA monopolist faces a demand curve Q(p) = 13p-4. The marginal cost (MC) is constant at 4 and there is no fixed cost. What is the monopolist's margin m = p-MC? Р (a) m (b) m || - m = 62 334 4 (d) m = 1/1/5 (e) None of the above.arrow_forwardA monopolist sells its product in two di§erent countries. The demand in country 1 is Q1 = 50-0.5P1, whereas the demand in country 2 is Q2 = 25-0.25P2. The firm's cost function is C(Q)=10+0.5Q2, where Q = Q1 + Q2.a) Calculate the amount of the product that the profit maximizing monopolist should sell in each country. Q1*=?, Q2*=?b) The determinantal test suggests that the firm's profit function (which one is correct) is locally concave around the critical point, but not elsewhere is globally concave is locally convex around the critical point, but not elsewhere is globally convex has a saddle point at the critical pointarrow_forward

- Can I get someone to answer these questions for me?arrow_forwardA monopolist has discovered that the inverse demand function of a person with income Y for the monopolist’s product is P = 0.002Y-Q where P is the price, Y the income, and Q is the output. The monopolist can observe the incomes of its consumers and hence vary its price accordingly. The monopolist has a total cost function C(Q) = 100Q. A. Calculate the profit maximising price as a function of the consumer’s income Y carefully explaining all the steps in the derivation of the formula. B. A monopolist has a constant marginal cost of £2 per unit and no fixed costs. He faces two separate markets in the United States and in the UK. The goods sold in one market are never resold in the other. He sets one price P1 for the US market and another price P2 for the UK market (both measured in £). The demand in the United States is given by Q1=7,000-700P1 and the demand in the UK is given by Q2=1,200-200P1. Calculate the profit maximising output produced and price charged in each country by the…arrow_forwardSuppose a monopolist is characterized as follows: P= 1200-5Q C = 8600 + 28Q+Q² MC 28 + 2Q demand curve for the monopolist total cost function for the monopolist marginal cost function for the monopolist To maximize its profit, the monopolist should produce units of output. (Enter your response rounded to two decimal places.) The company's profit-maximizing price is $ (Enter your response rounded to two decimal places.) The monopolist's profit is $ (Enter your response rounded to two decimal places.) Suppose the government imposes a specific tax of $150 per unit on the monopolist. To maximize profit, the monopolist should now produce units of output. (Enter your response rounded to two decimal places.) When the tax is imposed, the monopolist's profit-maximizing price becomes $ (Enter your response rounded to two decimal places.) As a result of the tax, the monopolist raises its price byarrow_forward

- 4) A monopolist faces a market inverse demand function: P = 250 – 5Q and marginal cost function: ATC = MC = 10. Answer the following. If the monopolist employs a single price strategy, what is the optimal quantity produced and price charged. What is the market up and contribution margin from the strategy in part a if Ed = -1.0833. If other firms trying to enter this market had slightly higher cost structures, what would be a good price & quantity mix to limit entry of competition and why (no math needed). If the monopolist could create a bundled good instead of the strategy in part a, what price would it charge and how many units would be sold in the bundle. What are the profits from part a & part d? Which pricing strategy is preferred. EC: Briefly explain why a firm that offers a buy 2 get the 3rd free deal, does not just offer that same product at a 33.33% discount of the normal stated price. Need help with number 2.arrow_forwardSuppose a monopolist faces a demand equation given by P=20-Q, and a marginal revenue equation given by MR = 20-2Q, and MC=AVC=ATC=$6. What is the deadweight loss associated with the monopolist? a) $8.5 b) $33.25 c) $24.5 d) $12.5arrow_forwardConsider an incumbent/monopolist with the following demand and marginal cost: P=300–Q; MC=$50. a. What is the profit maximizing price and output for the monopolist? What is the monopolist’s profit? b. Suppose there is a potential entrant, but the entrant has a cost disadvantage. The entrant’s MC = $75. Solve for the residual demand curve for the potential entrant (the entrant assumes that the monopolist will not change their total quantity from part a). c. What is the entrant’s output, price, and profit? What is the monopolist’s profit? d. What is the limit price that the monopolist could charge to deter entry? e. Is the threat/promise of the monopolist to charge the limit price a credible threat, or is the monopolist better off accommodating entry? Explain briefly.arrow_forward

- = 240 + 0.5Q², and face 4. A monopolist has the cost function TC(Q) market demand P = 45 – Q. (a) Find the monopoly equilibrium price and output. Find the monopolist's profit.arrow_forwardSuppose the market demand function (expressed in dollars) for a normal product is P= 90-q, and the marginal cost (in dollars) of producing it is MC = 1q, where P is the price of the product and q is the quantity demanded and/or supplied 1. Compute the consumer surplus and the producer surplus assuming this same product was supplied by a monopolist. Note that the monopolist’s marginal revenue curve has twice the slope of the demand curve. 2. Compare and contrast economic surpluses under monopoly market vs competitive market. 3.arrow_forwardAll 20 consumers are alike and each has a demand curve for a monopolist's product of p=15 -3q. The cost of production C(Q) =2Q. Let the monopolist charge a price of $PM for qM unit purchased. Find the menu prices that maximize profits? (The buyer pays menu price PM for quantity qM) What is the maximum profit the monopolist can earn in this market? (pi)?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education