FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

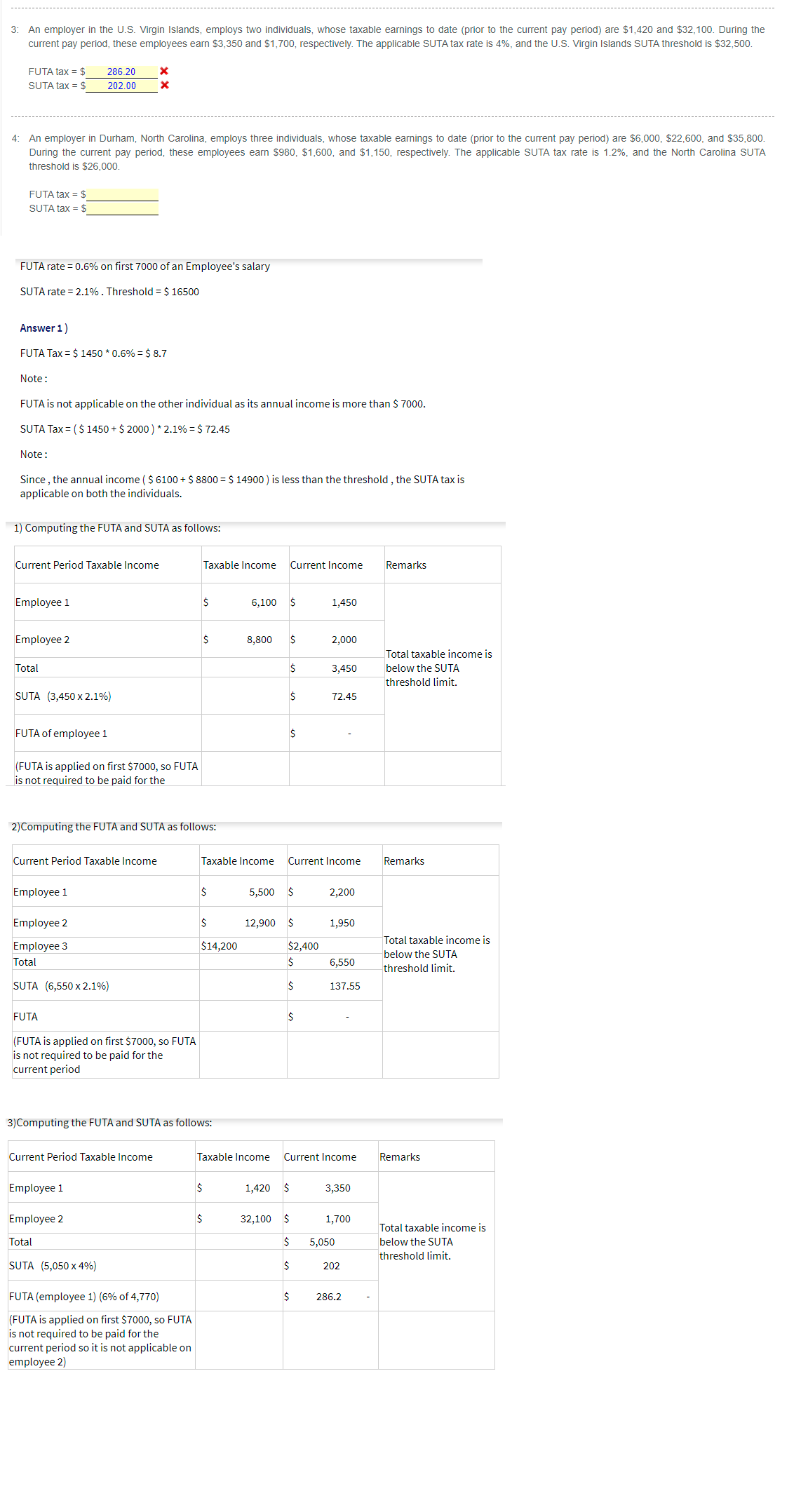

Transcribed Image Text:3: An employer in the U.S. Virgin Islands, employs two individuals, whose taxable earnings to date (prior to the current pay period) are $1,420 and $32,100. During the

current pay period, these employees earn $3,350 and $1,700, respectively. The applicable SUTA tax rate is 4%, and the U.S. Virgin Islands SUTA threshold is $32,500.

FUTA tax = $

286.20

SUTA tax = $

202.00

4: An employer in Durham, North Carolina, employs three individuals, whose taxable earnings to date (prior to the current pay period) are $6,000, $22,600, and $35,800.

During the current pay period, these employees earn $980, $1,600, and $1,150, respectively. The applicable SUTA tax rate is 1.2%, and the North Carolina SUTA

threshold is $26,000.

FUTA tax = $

SUTA tax = $

FUTA rate = 0.6% on first 7000 of an Employee's salary

SUTA rate = 2.1%. Threshold = $ 16500

Answer 1)

FUTA Tax = $ 1450 * 0.6% = $ 8.7

Note:

FUTA is not applicable on the other individual as its annual income is more than $ 7000.

SUTA Tax = ($ 1450 + $ 2000 ) * 2.1% = $ 72.45

Note:

Since , the annual income ( $ 6100 + $ 8800 = $ 14900 ) is less than the threshold , the SUTA tax is

applicable on both the individuals.

1) Computing the FUTA and SUTA as follows:

Current Period Taxable Income

Taxable Income

Current Income

Remarks

Employee 1

6,100

1,450

Employee 2

$

8,800

2,000

Total taxable income is

Total

3,450

below the SUTA

threshold limit.

SUTA (3,450 x 2.1%)

72.45

FUTA of employee 1

(FUTA is applied on first $7000, so FUTA

is not required to be paid for the

2)Computing the FUTA and SUTA as follows:

Current Period Taxable Income

Taxable Income

Current Income

Remarks

Employee 1

2$

5,500

2$

2,200

Employee 2

2$

12,900

1,950

Total taxable income is

Employee 3

$14,200

$2,400

below the SUTA

Total

6,550

threshold limit.

SUTA (6,550 x 2.1%)

137.55

FUTA

(FUTA is applied on first $7000, so FUTA

is not required to be paid for the

current period

3)Computing the FUTA and SUTA as follows:

Current Period Taxable Income

Taxable Income

Current Income

Remarks

Employee 1

1,420 $

3,350

Employee 2

32,100 $

1,700

Total taxable income is

Total

5,050

below the SUTA

threshold limit.

SUTA (5,050 x 4%)

202

FUTA (employee 1) (6% of 4,770)

286.2

(FUTA is applied on first $7000, so FUTA

is not required to be paid for the

current period so it is not applicable on

employee 2)

Transcribed Image Text:PSb 5-5 Calculate FUTA and SUTA Tax

For each of the following independent circumstances calculate both the FUTA and SUTA tax owed by the employer:

NOTE: For simplicity, all calculations throughout this exercise, both intermediate and final, should be rounded to two decimal places at each calculation.

1: An employer in Delaware City, Delaware, employs two individuals, whose taxable earnings to date (prior to the current pay period) are $6,100 and $8,800. During the

current pay period, these employees earn $1,450 and $2,000, respectively. The applicable SUTA tax rate is 2.1%, and the Delaware SUTA threshold is $16,500.

FUTA tax = $

0.00

SUTA tax = $

72.45

2: An employer in Bridgeport, Connecticut, employs three individuals, whose taxable earnings to date (prior to the current pay period) are $5,500, $12,900, and $14,200.

During the current pay period, these employees earn $2,200, $1,950, and $2,400, respectively. The applicable SUTA tax rate is 4.9%, and the Connecticut SUTA

threshold is $15,000.

FUTA tax = $

0.00

SUTA tax = $

137.55

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Mr. See Pag’s is a Filipino citizen working as a sales agent in EchpiComputer Accessories Store in Las Piñas City. He earns P26,000 a month basic salary and transportation allowance of P2,000. His deductions per month include SSS P1,630, PhilHealth P350, Pag-IBIG P100 and Union Dues P50. How much is Mr. Pag’s taxable income? Answer the questions briefly.1. Is Mr. Pag liable to pay taxes in the Philippines? Why? 2. How much is his total deductions? 3. How much is his taxable income?arrow_forwardHow much should be the income tax withheld on compensation income? Mr. B, married, is a citizen and resident of the Philippines. He had the following data on income and expenses: Salaries, net of P7,000 SSS, Philhealth, Pagibig contributions, and labor union dues Thirteen month pay Allowances Gain on sale of asset P88,000 8,000 16,000 10,000arrow_forwardPURELY COMPENSATION INCOME EARNER Instructions: 1. Download BIR Forms 1700 AND 2316 Version 2018 at www.bir.gov.ph. Compute the income tax payable, if any. Relevant information: YOU, single and a Filipino citizen, and a resident of Brgy. Talipapa, Quezon City is employed by PA-MINE Corp. located in N. Reyes St., Sampaloc, Manila for the calendar period 2021. During your employment, PA-MINE Corp. was able to apply for your TIN where BIR RDO No. 032 – Manila assigned you Taxpayer Identification No. 123-456-789-0000. PA-MINE Corp.’s TIN No. is 987-654-321-0000. Additional information: Your basic salary is Php 30,000 per month In addition to your basic pay, you received the following: Holiday pay – Php 10,000 Hazard pay – Php 20,000 Overtime pay – Php 20,000 Fixed transportation allowance – Php 10,000 Cost of Living Allowance – Php 20,000 13th month pay – Php 30,000 Other benefits – Php 20,000 De minimis benefit of Php – 20,000 PA-MINE Corp. has deducted the following…arrow_forward

- 1: An employer in Cleveland, OH, employs two individuals, whose taxable earnings to date (prior to the current pay period) are $5,000 and $12,000. During the current pay period, these employees earn $1,850 and $2,260, respectively.FUTA tax = $ 2: An employer in Nesconset, NY, employs three individuals, whose taxable earnings to date (prior to the current pay period) are $6,900, $1,000, and $24,200. During the current pay period, these employees earn $2,200, $1,950, and $2,800, respectively.FUTA tax = $ 3: An employer in The U.S. Virgin Islands employs two individuals, whose taxable earnings to date (prior to the current pay period) are $8,500, and $3,400. During the current pay period, these employees earn $870 and $525, respectively.FUTA tax = $ 4: An employer in Cary, NC, employs three individuals, whose taxable earnings to date (prior to the current pay period) are $5,900, $8,900, and $6,600. During the current pay period, these employees earn $960, $1,070, and $820,…arrow_forwardDetermine the taxable income for the year. (PHILIPPINES)arrow_forwardAn employer in Cincinnatti, Ohio employs two individuals, whose taxable earnings to date (prior to the current pay period) are $4,900 and $7,700. During the current pay period, these employees earn $2,700 and $1,800, respectively. The applicable SUTA tax rate is 2.5%, and the Ohio SUTA threshold is $9,000. FUTA Tax________ SUTA Tax _____arrow_forward

- Badges of trade are used to determine A. if an individual is UK resident or not B. whether or not a trade exists C. how much tax an individual should pay D. the age of a taxpayer 10. Unused pension allowance can be carried forward up to A. 1 year B. 3 years C. 2 years D. 6 years.arrow_forward4:An employer in Durham, North Carolina, employs three individuals, whose taxable earnings to date (prior to the current pay period) are $5,900, $8900 and $6600 During the current pay period, these employees earn $940, $1,020, and $850, respectively. FUTA TAX?arrow_forwardAn employer in Newark, New Jersey employs three individuals, whose taxable earnings to date (prior to the current pay period) are $27,800, $33,200, and $6,850. During the current pay period, these employees earn $3,200, $2,950, and $1,620, respectively. The applicable SUTA tax rate is 3.4%, and the New Jersey SUTA threshold is $35,300. FUTA Tax _____ SUTA Tax _____arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education