Cornerstones of Financial Accounting

4th Edition

ISBN: 9781337690881

Author: Jay Rich, Jeff Jones

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Question

Transcribed Image Text:2225

4 points

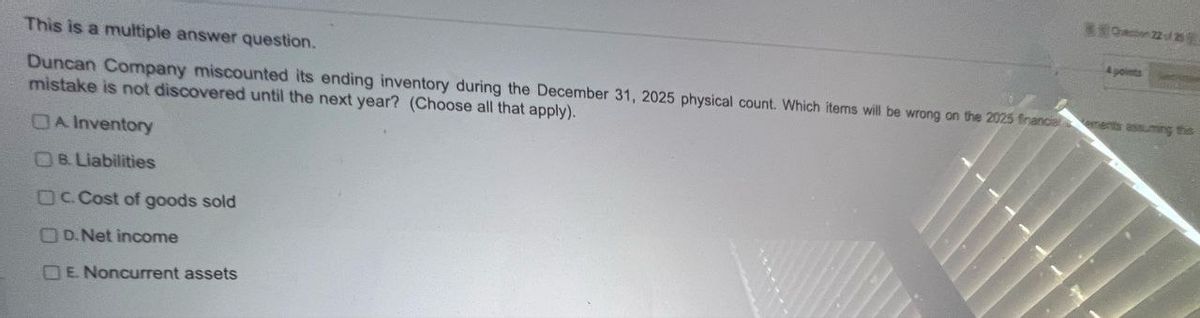

This is a multiple answer question.

Duncan Company miscounted its ending inventory during the December 31, 2025 physical count. Which items will be wrong on the 2025 franciaments assuming this

mistake is not discovered until the next year? (Choose all that apply).

OA Inventory

8. Liabilities

OC. Cost of goods sold

OD.Net income

OE. Noncurrent assets

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- Effects of an Error in Ending Inventory Waymire Company prepared the partial income statements presented below for 2019 and 2018. During 2020, Waymires accountant discovered that ending inventory for 2018 had been understated by $6,500. Required: 1. Prepare corrected income statements for 2019 and 2018. 2. Prepare a schedule showing each financial statement item affected by the error and the amount of the error for that item (ignore the effect of income taxes). Indicate whether each error is an overstatement (+) or an understatement (-).arrow_forwardInventory Errors McLelland Inc. reported net income of $175,000 for 2019 and $210,000 for 2020. Early in 2020, McLelland discovers that the December 31, 2019 ending inventory was overstated by $20,000. For simplicity, ignore taxes. Required: 1. What is the correct net income for 2019? For 2020? 2. Assuming the error was not corrected, what is the effect on the balance sheet at December 31, 2019? At December 31, 2020?arrow_forwardCompany Edgar reported the following cost of goods sold but later realized that an error had been made in ending inventory for year 2021. The correct inventory amount for 2021 was 12,000. Once the error is corrected, (a) how much is the restated cost of goods sold for 2021? and (b) how much is the restated cost of goods sold for 2022?arrow_forward

- Assuming a companys year-end inventory were overstated by $5,000, indicate the effect (overstated/understated/no effect) of the error on the following balance sheet and income statement accounts. A. Income Statement: Cost of Goods Sold B. Income Statement: Net Income C. Balance Sheet: Assets D. Balance Sheet: Liabilities E. Balance Sheet: Equityarrow_forwardAssuming a companys year-end inventory were understated by $16,000, indicate the effect (overstated/understated/no effect) of the error on the following balance sheet and income statement accounts. A. Income Statement: Cost of Goods Sold B. Income Statement: Net Income C. Balance Sheet: Assets D. Balance Sheet: Liabilities E. Balance Sheet: Equityarrow_forwardIf a group of inventory items costing $15,000 had been omitted from the year-end inventory count, what impact would the error have on the following inventory calculations? Indicate the effect (and amount) as either (a) none, (b) understated $______, or (c) overstated $______. Table 10.1arrow_forward

- At the end of 2019, Manny Company recorded its ending inventory at 350,000 based on a physical count. During 2020, the company discovered that the correct inventory value at the end of 2019 should have been 400,000 because it made a counting error. Upon discovery of this error in 2020, what correcting journal entry will Manny make? Ignore income taxes.arrow_forwardThe following are independent errors made by a company that uses the periodic inventory system: a. Goods in transit, purchased on credit and shipped FOB destination, 10,000, were included in purchases but not in the physical count of ending inventory. b. Purchase of a machine for 2,000 was expensed. The machine has a 4-year life, no residual value, and straight-line depreciation is used. c. Wages payable of 2,000 were not accrued. d. Payment of next years rent, 4,000, was recorded as rent expense. e. Allowance for doubtful accounts of 5,000 was not recorded. The company normally uses the aging method. f. Equipment with a book value of 70,000 and a fair value of 100,000 was sold at the beginning of the year. A 2-year, non-interest-bearing note for 129,960 was received and recorded at its face value, and a gain of 59,960 was recognized. No interest revenue was recorded and 14% is a fair rate of interest. Required: 1. Next Level Indicate the effect of each of the preceding errors on the companys assets, liabilities, shareholders equity, and net income in the year in which the error occurs. State whether the error causes an overstatement (+), an understatement (), or no effect (NE). 2. Prepare the correcting journal entry or entries required at the beginning of the year for each of the preceding errors, assuming the company discovers the error in the year after it was made. Ignore income taxes.arrow_forwardThe following items were included in Venicio Corporations inventory account on December 31, 2019: What amount should Venicio report as inventory at December 31, 2019? a. 21,000 b. 20,400 c. 26,000 d. 35,000arrow_forward

- Refer to the information provided in RE8-4. If Paul Corporations inventory at January 1, 2019, had a cost and net realizable value of 300,000, prepare the journal entry to record the reductions to NRV for Paul Corporation assuming that Paul uses a periodic inventory system and the allowance method. Paul Corporation uses FIFO and reports the following inventory information: Assuming Paul uses a perpetual inventory system and the direct method, prepare the journal entry to record the write-down of inventory.arrow_forwardIf Barcelona Companys ending inventory was actually $122,000, but the cost of consigned goods, with a cost value of $20,000 were accidentally included with the company assets, when making the year-end inventory adjustment, what would be the impact on the presentation of the balance sheet and income statement for the year that the error occurred, if any?arrow_forwardKoopman Company began operations on January 1, 2018, and uses they FIFO inventory method for financial reporting and the average cost inventory method for income taxes. At the beginning of 2020, Koopman decided to switch to the average cost inventory method for financial reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the FIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Koopman is subject to a 21% income tax rate in all years; it pays the income taxes payable of a current year in the first quarter of the next year. Koopman had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Koopman had cash of 10,000, inventory of 24,000, other assets of 70,800, accounts payable of 4,500, and income taxes payable of 6,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in methods at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning