FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

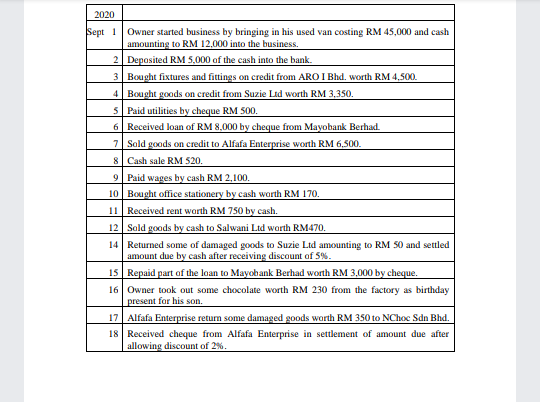

Transcribed Image Text:2020

Sept 1 Owner started business by bringing in his used van costing RM 45,000 and cash

amounting to RM 12,000 into the business.

2 Deposited RM 5,000 of the cash into the bank.

3 Bought fixtures and fittings on credit from ARO I Bhd. worth RM 4.500.

4 Bought goods on credit from Suzie Ltd worth RM 3,350.

5 Paid utilities by cheque RM 500.

6 Received loan of RM 8,000 by cheque from Mayobank Berhad.

7 Sold goods on credit to Alfafa Enterprise worth RM 6.500.

8 Cash sale RM 520.

9 Paid wages by cash RM 2,100.

10 Bought office stationery by cash worth RM 170.

11 Received rent worth RM 750 by cash.

12 Sold goods by cash to Salwani Ltd worth RM470.

14 Returned some of damaged goods to Suzie Ltd amounting to RM 50 and settled

amount due by cash after receiving discount of 5%.

15 Repaid part af the loan to Mayobank Berhad worth RM 3,000 by cheque.

16 Owner took out some chocolate worth RM 230 from the factory as birthday

present for his son.

17 Alfafa Enterprise returm some damaged goods worth RM 350 to NChoc Sdn Bhd.

18 Received cheque from Alfafa Enterprise in settlement of amount due after

allowing discount of 2%.

Transcribed Image Text:Required:

(Dikehendaki:

a) Prepare the general journal.

(Sediakan jurnal am,.)

b) Post all the transactions into the ledger accounts.

[Masukkan semua transaksi ke akaun-akaun lejar.

c) Prepare the Trial Balance as at 30 September 2020.

(Sediakun Iwdangan Duga pada 30 September 2020.)

Filters

Add a caption.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- PA5. LO 8.5 Inner Resources Company started its business on April 1, 2019. The following transactions occurred during the month of April. Prepare the journal entries in the journal on Page 1. A. The owners invested $8,500 from their personal account to the business account. B. Paid rent $650 with check #101. C. Initiated a petty cash fund $550 check #102. D. Received $750 cash for services rendered. E. Purchased office supplies for $180 with check #103. F. Purchased computer equipment $8,500, paid $1,600 with check #104 and will pay the remainder in 30 days. G. Received $1,200 cash for services rendered. H. Paid wages $560, check #105. I. Petty cash reimbursement office supplies S200, Maintenance Expense S140, Miscellaneous Expense S65. Cash on Hand $93. Check #106. J. Increased Petty Cash by S100, check #107.arrow_forwardK Bryson Inc. collects cash from customers two ways: 1. Accrued Revenue. Some customers pay Bryson after Bryson has performed service for the customer. During 2020, Bryson made sales of $53,000 on account and later received cash of $45,000 on account from these customers. 2. Unearned Revenue. A few customers pay Bryson in advance, and Bryson later performs service for the customer. During 2020, Bryson collected $6,500 cash in advance and later earned $5,000 of this amount. Journalize the following for Bryson: a. Earning service revenue of $53,000 on account and then collecting $45,000 on account b. Receiving $6,500 in advance and then earning $5,000 as service revenue a. Journalize Bryson earning service revenue of $53,000 on account and then collecting $45,000 on account. Start by recording earning service revenue on account. (Record debits first, then credits. Explanations are not required.) Date 2020 Accounts Debit Creditarrow_forward

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education