ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

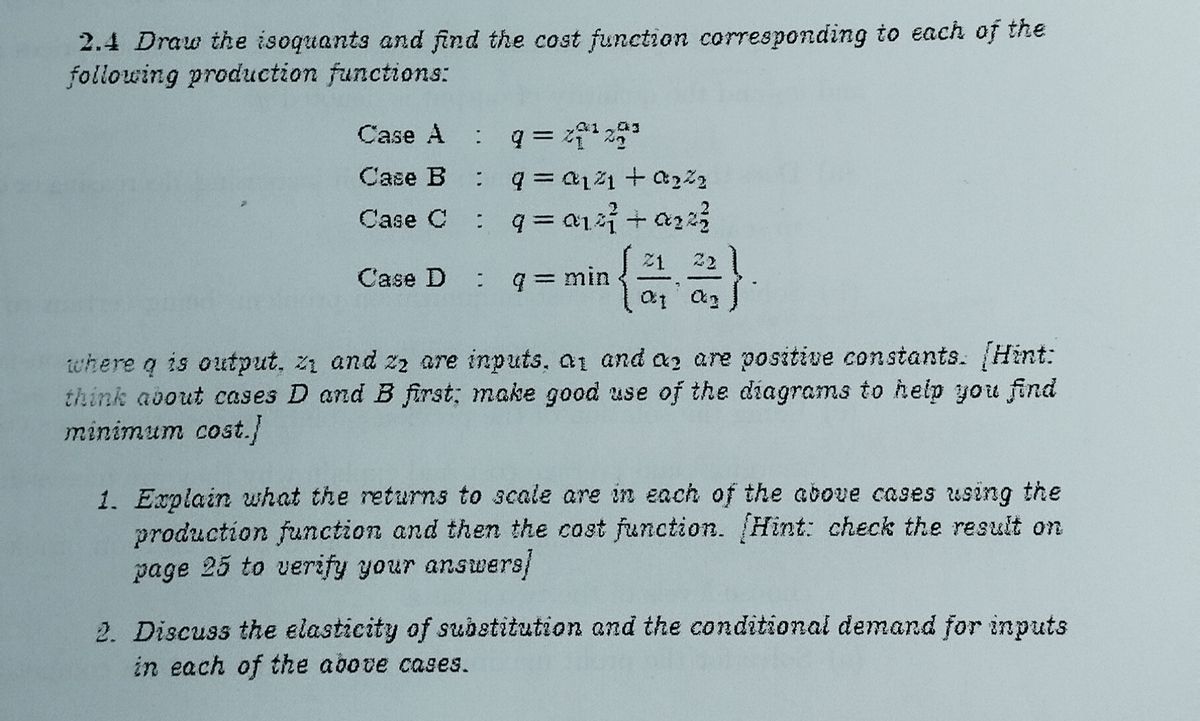

Transcribed Image Text:2.4 Draw the isoquants and find the cost function corresponding to each of the

following production functions:

Case A : q = ²2

Case B : q=0121 + a₂%2

Case C

= q=a1²² +₂²²

Case D : q = min

21

(23)

01 01

where q is output, z₁ and 22 are inputs. a1 and as are positive constants. [Hint:

think about cases D and B first; make good use of the diagrams to help you find

minimum cost.)

1. Explain what the returns to scale are in each of the above cases using the

production function and then the cost function. Hint: check the result on

page 25 to verify your answers/

2. Discuss the elasticity of substitution and the conditional demand for inputs

in each of the above cases.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 25 images

Knowledge Booster

Similar questions

- Give me answerarrow_forward1. The following production function is used to produce wheat, q, from capi- tal, K, and labour, L: q = f(K, L) = «³K/3 + B³L/3 a) Describe the role of a and B in this production function. b) Derive the slope of an isoquant for this production function and in- terpret your result. Draw the isoquant in (K L) space, labeling where appropriate. The drawing does not need to be exact, but the curvature needs to be approximately correct. Explain why under- standing the curvature is so important. | c) Does this production function follow the "Law of Diminishing Marginal Returns"? Show your work and explain your answer.arrow_forwarduppose a Cobb-Douglas Production function is given by the following:P(L,K)=60L^0.8K^0.2where LL is units of labor, KK is units of capital, and P(L,K) is total units that can be produced with this labor/capital combination. Suppose each unit of labor costs $900 and each unit of capital costs $3,600. Further suppose a total of $900,000 is available to be invested in labor and capital (combined).A) How many units of labor and capital should be "purchased" to maximize production subject to your budgetary constraint?Units of labor, LL = Units of capital, KK = B) What is the maximum number of units of production under the given budgetary conditions? (Round your answer to the nearest whole unit.)Max production = unitsarrow_forward

- Q = a,H + a,L +a,H² +a¸L² +a‚HL , where a,>0 2. Q = aH " L, where a, a, y> 0 a) Derive the equation of the relevant Isoquant. b) Find out whether the production function is well behaved.arrow_forward1. Assume a daily production function for a firm is Q= min(3L, 4K) a, If L = 100 and K = 100 what quantity is produced? Explain why. b. What would be the cost-minimizing labor and capital combination for this firm to produce Q = 1200? (show your work) Labor = Capital = At this level of production from part b (Q-1200), if the wage rate is: w- $30 and the rental rate of capital is: r= $100, what is the total cost of production? (show your calculations) C.arrow_forwardPlease indicate which multiple choice awnser is correct for question 1.1)1.2)1.3)Please indicate it correctly as I have had this awnsered with different letters to the awnser I was told 1.1 - A firm trebles its inputs and discovers that its output rises by a factor of four. This is an example of;Select one or more:a. constant returns to scaleb. diminishing returns to a variable factor c. increasing returns to scaled. economies of scale1.2 - Diseconomies of scale are present when.... Select one or more:a. marginalcostsriseb. long run average costs rise as output rises c. totalcostsfallasoutputrisesd. total costs rise as output rises 1.3 - If the demand for a firm’s product is price inelastic, this implies that Select one or more: a. price changes have no impact on quantity demandedb. a fall in price of 3% will lead to a decline in quantity demanded of more than 3%c. a rise in price will raise total expenditure on the goodd. a 5% rise in price will result in a fall in quantity…arrow_forward

- Jeff spends all of his money on housing (H) and other stuff (S) and has a diminishing marginal rate of substitution between housing and stuff. Jeff used to live and work in a small town where housing prices were relatively low. His company has decided to transfer him to a large city where housing prices are higher. (For simplicity, assume that all other prices are the same.) Using a diagram, explain to Jeff's company how to find the amount it needs to raise his salary to keep him just as well after the 2. transfer as he was before. Tridorarrow_forward13. Suppose you have a production technology given by f(x1, x2) = min{2x₁, x2} and you are producing at the point where x₁ = 10 and x₂ = 20. (a) Explain in words what we mean (generally) by the ‘marginal product' of an input in production. (b) For the production technology in this question and the initial point x₁ = 10 and x2 = 20, what is the marginal product of a small increase in input 1? (c) Suppose input 2 increases and you are now at the initial point x₁ = 10 and x2 = 30. Relative to your answer in part (b), does the marginal product of input 1 decrease, increase, or stay constant? Explain briefly.arrow_forwardThe following equations represent the long-run production functions for four different technologies, where capital and labor are both variable inputs. For each function, indicate whether it exhibits increasing, decreasing, or constant returns to scale. Clearly show your derivations. (Note that in parts a and c, the exponents are decimals.) f(L,K)= 8L²K4 b. f(L,K)= L+7K c. f(L,K)= L³K d. f(L,K)= 4L+K? а. с.arrow_forward

- How would you determine that a two-input Cobb-Douglas production function has decreasing returns to scale (DRS), increasing returns to scale (IRS) or constant returns to scale (CRS) depending on whether α1 + α2 is larger than, smaller than, or equal to one?arrow_forwardWhich of the following production functions exhibits increasing returns to scale in the factors of production K and L? a. y = ĀK0.3 L0.75 b. y = Kª(ĀL)-e,0 < a < 1 c. y = ĀKO.3L0.3 d. y = ĀK/4 + L³/4arrow_forwardAssume a Cobb-Douglas production function of the form: 3 What type of returns to scale does this production function exhibit? In this instance, returns to scale equal This production function exhibits q=10L0.28K0.59 (Enter a numeric response using a real number rounded to two decimal places.) OA. increasing returns to scale. OB. constant returns to scale. OC. initially decreasing but then constant returns to scale. O D. decreasing returns to scale. O E. initially constant but then decreasing returns to scale.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education