ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

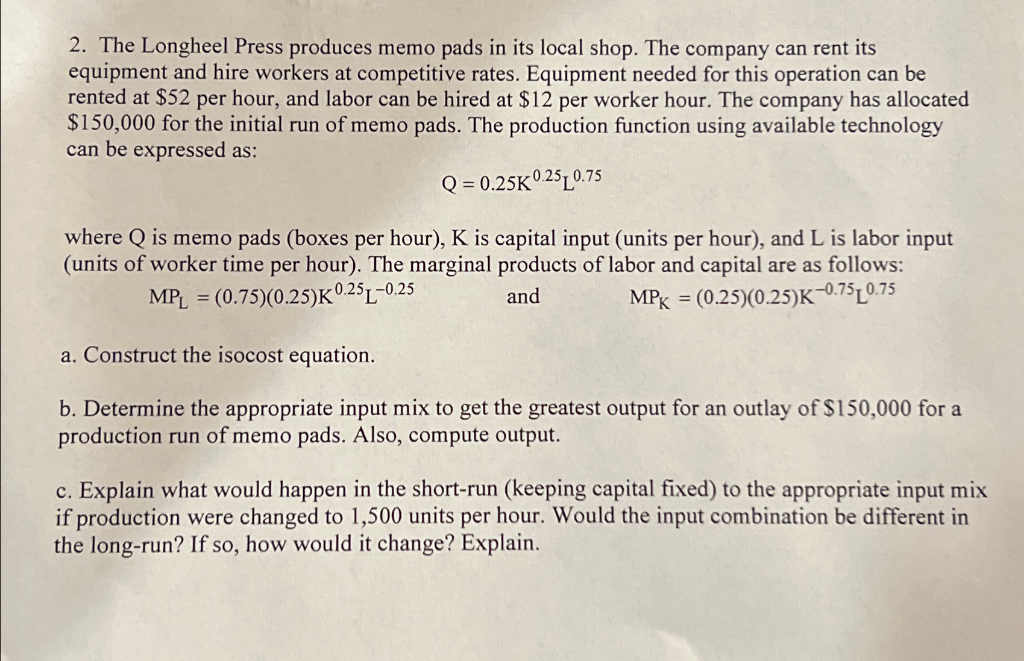

Transcribed Image Text:2. The Longheel Press produces memo pads in its local shop. The company can rent its

equipment and hire workers at competitive rates. Equipment needed for this operation can be

rented at $52 per hour, and labor can be hired at $12 per worker hour. The company has allocated

$150,000 for the initial run of memo pads. The production function using available technology

can be expressed as:

Q=0.25K 0.25 0.75

where Q is memo pads (boxes per hour), K is capital input (units per hour), and L is labor input

(units of worker time per hour). The marginal products of labor and capital are as follows:

MPL = (0.75)(0.25)K 0.25-0.25

a. Construct the isocost equation.

and

MPK = (0.25)(0.25)K-0.750.75

b. Determine the appropriate input mix to get the greatest output for an outlay of $150,000 for a

production run of memo pads. Also, compute output.

c. Explain what would happen in the short-run (keeping capital fixed) to the appropriate input mix

if production were changed to 1,500 units per hour. Would the input combination be different in

the long-run? If so, how would it change? Explain.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 5 steps with 11 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The Mini-Case "Economies of Scale at Google describes economies of scale for Google Cloud Storage. The cost function for this service is well-approximated by K C(q)-F+cq where C is total cost, F is fixed cost, c is a constant and q is output. What is marginal cost for this cost function? What are the average fixed cost, average variable cost, and average cost? Over what range of output does Google have economies of scale? The marginal cost function (MC) is The average fixed cost function (AFC) is AFC- The average variable cost function (AVC) is AVC- MC-C The average cost function (AC) is AC- (Property format your expressions using the tools in the palette. Hover over tools to see keyboard shortcuts. Eg, a fraction can be created with the character) Time Remaining: 02.09.09arrow_forwardSuppose a firm has the following production function Q = f(K,L) = (1/2)L(2/3)K(1/3) and a total cost function TC = wL + rK The rental cost of capital is 2 euros per hour and the labor wage is 4 euros per hour. Suppose also that in the short-run, the firm uses 8 machines in the production process. (a) Show that the firm’s short-run average cost (SRAC) is SRACK=8 = (16/Q)+ 4√? (b) Draw the SRAC curve(c) By solving the first order conditions that the global minimum of production is 4(d) Show that the firm’s long-run average cost (LRAC) is 12. Hint: Start by obtaining the firm’s long-run expansion path(e) Draw both the SRAC and the LRAC and explain why the SRAC is always equal or above the LRAC.arrow_forward4. Ikea Inc., a home remodeling business. The number of square feet they can remodel in a day is described by the Cobb-Douglas production function Q= F (L,K)= 4K5L0.5 where L is their number of workers and K is units of capital. The wage rate is $5 a day, and a unit of capital costs $20 a day. What is their minimum cost input combination for remodeling (Q=200) 200 square feet a day? What is the total minimum cost level? (15p)arrow_forward

- A firm estimates its production function as Q = -2.4 + 20*L -.5*L2 + 30*K -1.00*K2 + 15*F -.3*F2. Total cost is TC = $2*L + $2.5*K + $1.75*F. The firm wishes to produce 400 units of output. Use Excel to find the cost minimizing amounts of L, K and F. How much F (Fuel) should the firm use?arrow_forwardAnswer the question on the basis of the following cost data. Average Fixed Average Variable Output Cost Cost 1 $ 50.00 $ 100.00 2 25.00 80.00 3 16.67 66.67 4 12.50 65.00 5:35 5 10.00 68.00 6 8.37 73.33 7 7.14 80.00 8 6.25 87.50 The marginal cost of the sixth unit of output is Multiple Choice О $440.00. $8.37.arrow_forwardsuppose a company has two production facilities with two different TC functions. in facility A total costs are given by $600,000+0.4Q^2 in facility B total costs are given by $300,000+0.5Q^2 The firm needs to produce 900 units how many units should they produce in facilities a and b to minimize total costsarrow_forward

- A firm produces plastic bins using labor (measured in man-hours) and capital (measured in machine-hours), according to the production function Q = f(L,K) = LK, where Q is the number of plastic bins produced. Suppose that the cost of labor is $20 per worker-hour and the cost of capital is $10 per machine-hour. What is the cost minimizing input combination if the firm wants to produce 28,800 plastic bins? Hint: The marginal products are MP, = K and MPg = L.arrow_forwardYummy Gummies, Inc. makes boxes of individually packaged gummies. The company has a cost function given by C(x) dollars when x boxes of Yummy Gummies are made. If C '(100) = $3.50 per box, which of the following can we conclude from this information? %3D O The approximate cost of making the 100" box of Yummy Gummies is $3.50. O The exact cost of making the 99h box of Yummy Gummies is $3.50. The approximate cost of making the 101“ box of Yummy Gummies is $3.50. O The approximate cost of making the 99 box of Yummy Gummies is $3.50. O The exact cost of making the 101st box of Yummy Gummies is $3.50.arrow_forwardNo hand written solution and no imagearrow_forward

- Jaskier can only produce output in integer units. His Fixed cost is $200 and his Total Cost of production for every quantity is given in the table below. What is his minimum Average Variable Cost? Q TC 1 322.31 2 344.24 3 380.79 4 406.53 5 511.2 6 578.16 7 800 8 782.84 9 907.11 10 1046arrow_forward30. The production function is f(L, M) = 4L1/2 M¹2, where L is the number of units of labor and M is the number of machines used. If the cost of labor is $49 per unit and the cost of machines is $16 per unit, then what is the total cost of producing 5 units of output?arrow_forwardA firm has the following information on production and costs from past data: Output (Y) 0 12 18 6 Total Cost (TC) 9 2775 5361 8199 If the total cost function is known to be TC = aY' + bY ² + kY + ƒ , and the demand for the product of the firm is Y = 320-(1/2). P answer the following: • Determine the coefficients of the cubic cost function. • Derive all cost and revenue curves and the profit function. Show that the MC cuts the AVC when AVC is at its minimum point. Plot the relevant graph indicating all points. Calculate the break even and profit maximizing levels of output and price. • What is the relationship between price, marginal revenue and own price elasticity of demand at the profit maximization point.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education