ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

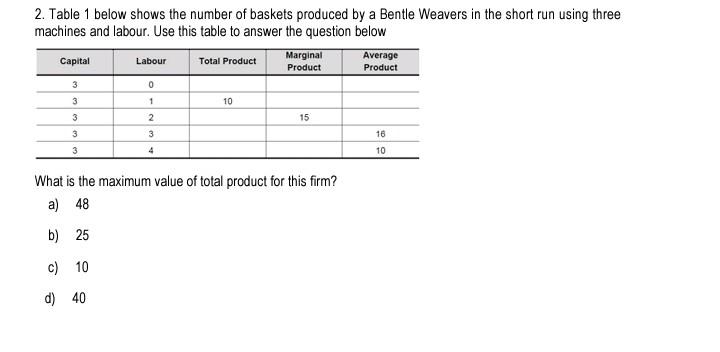

Transcribed Image Text:2. Table 1 below shows the number of baskets produced by a Bentle Weavers in the short run using three

machines and labour. Use this table to answer the question below

Capital

3

3

3

3

3

Labour

0

1

2

3

4

Total Product

10

Marginal

Product

15

What is the maximum value of total product for this firm?

a) 48

b)

25

c) 10

d) 40

Average

Product

16

10

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 2. Short Run Production Function and Total Product curve. You will need words, a chart and a graph here. Next, be sure to do the same for average and marginal product of labor. Explain what is going on in your graphs.arrow_forwardNote: The answer should be typed.arrow_forward3. We often work with production technologies that give rise to initially increasing marginal product of labor that eventually decreases. Are the following statements then True or False? Explain.The marginal product of labor becomes negative when the slope of the production frontier begins to get shallower as we move toward more labor input.arrow_forward

- 5) can i get help with this questionarrow_forward20arrow_forwardshows the long-run average costs for three firms. Quantity Ali's Hats 1 2 3 4 5 6 7 $110 60 90 115 150 220 300 Bodi's Bats $110 80 70 70 70 70 90 Cody's Mats $110 90 80 70 50 20 30 a) In which industry, Hats, Bats or Mats, would there likely be many small firms? Industry: (Click to select) · b) In which industry, Hats, Bats or Mats, would there likely be firms of many different sizes? Industry: (Click to select) - c) Which industry Hats Bats or Mats, would likely be dominated by a few large firms? Industry (Click to select) Hats Bats Matsarrow_forward

- (Figure: Determining Marginal Returns) Based on both the table and the figure, adding a third worker leads to marginal returns. Average Product and Marginal Product Output 1 2 3 14 Labor 5 6 17 12 10 8 6 4 8 9 10 0 -2 BAY constant 2 Total Product O negative 5 12 21 31 40 48 54 57 57 increasing 54 diminishing 4 MP 5 7 9 10 9 8 6 3 0 3 6 Workers AP 5 6 7 7.75 8 8 7.71 7.12 6.33 5.4 8 10 12arrow_forward4. At Alan's landscaping firm, labor is fixed in the short run. Increasing his use of capital always leads to additional output and his production function exhibits both increasing and diminishing marginal returns to capital at different points. Using a two-panel diagram, sketch the marginal, average, and total product of canital at Alan's firm. Your diagram does not need to be to scale, but must be internally consistent and consistent with both the information given and economic theory. Explain your diagram and the relationship between the different curves.arrow_forwardQuestion When do firms decide to shut down production in the short run? Explain it. How is the short run average cost curve and the long run average cost curve shaped? What is the difference between them? Graphical representation of the short-run total cost curve showing total cost, fixed cost, variable cost: and The marginal cost and average total cost:arrow_forward

- Please kindly provide solution for b & Carrow_forwardLabor (workers) Output 0 20 50 70 80 85 OAN 345 0 The table above shows a total product schedule. Suppose that labor costs $20 per worker and fixed costs are $60. The total cost of producing 80 units equals O less than $5. O more than $5 and less than $110. O more than $110 and less than $120. O more than $120 and less than $150. DIS O more than $150.arrow_forward7. A firm can build a plant of three different sizes. The short-run average total cost curves of each size plant are as follows: Plant A Plant B Plant C Output Average Total Cost Output Average Total Cost Output Average Total Cost 1 20 20 30 20 50 5 18 40 20 50 20 10 15 60 10 400 3 20 20 80 20 600 8 25 40 100 50 800 20 What is the long-run average cost of producing 20 units of output? Why?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education