ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

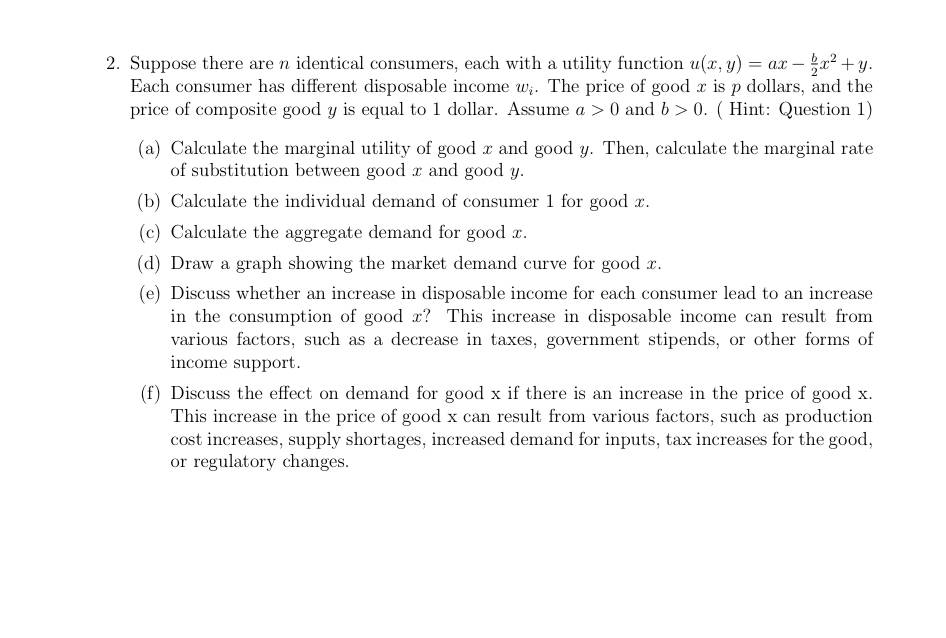

Transcribed Image Text:2. Suppose there are n identical consumers, each with a utility function u(x, y): = ax = x²+y.

Each consumer has different disposable income w. The price of good x is p dollars, and the

price of composite good y is equal to 1 dollar. Assume a > 0 and b > 0. (Hint: Question 1)

(a) Calculate the marginal utility of good x and good y. Then, calculate the marginal rate

of substitution between good x and good y.

(b) Calculate the individual demand of consumer 1 for good x.

(c) Calculate the aggregate demand for good x.

(d) Draw a graph showing the market demand curve for good x.

(e) Discuss whether an increase in disposable income for each consumer lead to an increase

in the consumption of good x? This increase in disposable income can result from

various factors, such as a decrease in taxes, government stipends, or other forms of

income support.

(f) Discuss the effect on demand for good x if there is an increase in the price of good x.

This increase in the price of good x can result from various factors, such as production

cost increases, supply shortages, increased demand for inputs, tax increases for the good,

or regulatory changes.

SAVE

AI-Generated Solution

info

AI-generated content may present inaccurate or offensive content that does not represent bartleby’s views.

Unlock instant AI solutions

Tap the button

to generate a solution

to generate a solution

Click the button to generate

a solution

a solution

Knowledge Booster

Similar questions

- Suppose your utility for goods x1 and x2 is represented by the following utility function: U(x1,x2)= x11/5 x24/5 a) What is your marginal rate of substitution, MRS12? b) If the price for good x1 is p1 = 2, the price for good x2 is p2 = 4, and your available income is m = 20, write down your budget constraint. c) Using the prices and income given at b) above, find your optimal consumption choice bundle (Marshallian demand) and its corresponding utility level. d) Illustrate your optimal consumption choice on a graph. e) For the prices given in b), what income would you need to achieve a utility level of 25?arrow_forwardA consumer has a utility function U(X,Y ) = X1/2 Y1/2 . Prices of the goods are pX = £10 and pY = £5, respectively, and the consumer has income M = £200 to spend on X and Y. Currently, she buys 2 units of good X and spends the rest of her income on good Y.a) Determine this consumer’s current utility level. b) Compute the consumer’s marginal utilities of goods X and Y. c) Explain why the consumer’s current consumption of goods X and Y is not optimal. Should she substitute X for Y or vice versa? The consumer’s marginal rate of substitution is MRS = Y/X.d) Determine this consumer’s optimal consumption of both goods. e) By how much does the consumer’s utility increase when she consumes the optimal bundle?arrow_forwardSuppose your utility for goods x1 and x2 is represented by the following utility function: U(x1,x2)= x11/5 x24/5 a) What is your marginal rate of substitution, MRS12? b) If the price for good x1 is p1 = 2, the price for good x2 is p2 = 4, and your available income is m = 20, write down your budget constraint. c) Using the prices and income given at b) above, find your optimal consumption choice bundle (Marshallian demand) and its corresponding utility level. d) Illustrate your optimal consumption choice on a graph. e) For the prices given in b), what income would you need to achieve a utility level of 25? PLEASE ONLY ANSWER PART C, D AND Earrow_forward

- Suppose your income is 200, the price of good x is 2, and the price of good y is 3. You know that your utility function is U= 2(xy)^3. (A) What amounts of x and y do you choose? (B) Can you generalize your choices to demand curves for x and y for any prices and income?arrow_forwardrefer to question 1 but answer question 2arrow_forwardConsider the single-good utility function u(x) = 3x². du(x) a) Find the marginal utility of x, MUx = dx b) Plot the utility function and marginal utility function on two separate graphs. c) Does this utility function satisfy the law of diminishing marginal utility? Explain.arrow_forward

- Assume that a person’s utility depends on two products, x and y. The utility function is given by U(x, y) = (x + 2)^2(y + 3)^3. Find the marginal utility of x and marginal utility of y.arrow_forward3*. Ms Smith likes to drink wine; in particular, a french bordeaux (f) at $40 per bottle and a California varietal wine (c) priced at $8. She allocates $600 to these two each month; and her utility is: U(ƒ, c) = ƒ²/³ c¹/³ (a) Write out her (constrained) utility maximization problem. Solve for the optimal consumption of wine f and c.arrow_forwardA consumer consumption bundle contains good X and Y. Suppose the price of good X goes up and a consumer goes on consuming the exact same amount of X as before. Check the correct statement(s).A) Both X and Y are inferior. B) X is an inferior good.C) In the special case where X is Leisure, and Y is "all other goods", X is an inferior good.D) The consumption of Y decreases.E) It is impossible that the consumption of X remains unchanged when the price of × goes up.F) The substitution effect is negativearrow_forward

- 2) Which of the following utility functions represent the same preferences? Explain. a) U (x₁, x₂) = X₁ X₂ b) W (x₁, x₂) = 5lnx₁ +5lnx₂ c) V (x₁, x₂) = x₁¹/3x₂ ¹/3 - 0.8 d) Z(x₁, x₂) = 0.5x₁ + 0.5x₂arrow_forwardConsider a person who consumes two goods, x and y, and has a utility function given by U(x, y) = In(x)+y. This person has an income of $100 and faces a price of $0.50 for good x and $1 for good y. Price of x then rises to $0.60. Solve for the compensating variation (CV) and equivalent variation (EV) of this price change. Show your work.arrow_forwardA consumer has utility (see image) on ice creams (x) and cakes (y). (a) Are the indifference curves bowed towards the origin? (b) Derive his demand function (as a function of prices px, py and budget I) for ice cream (x). (c)(Looking at the demand function you found in (b), Is ice cream a normal good? Are ice cream and cakes substitutes or complements? Calculate the income elasticity of market demand at the point px = 2, py = 1 and I = 12.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education