Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Solve a and b part only in one hour plz solve this now in one to 2 hour if u can't solve then reject this now in 2 hours so that I can't wait for your answer plz

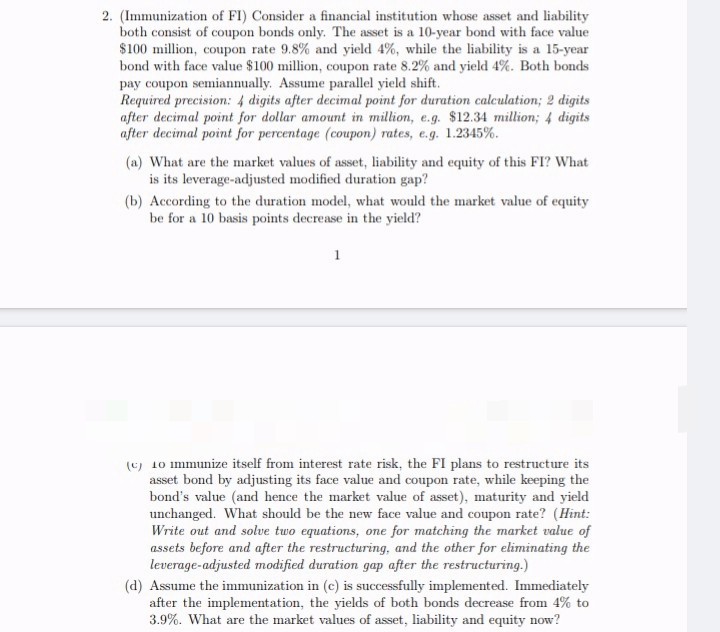

Transcribed Image Text:2. (Immunization of FI) Consider a financial institution whose asset and liability

both consist of coupon bonds only. The asset is a 10-year bond with face value

$100 million, coupon rate 9.8% and yield 4%, while the liability is a 15-year

bond with face value $100 million, coupon rate 8.2% and yield 4%. Both bonds

pay coupon semiannually. Assume parallel yield shift.

Required precision: 4 digits after decimal point for duration calculation; 2 digits

after decimal point for dollar amount in million, e.g. $12.34 million; 4 digits

after decimal point for percentage (coupon) rates, e.g. 1.2345%.

(a) What are the market values of asset, liability and equity of this FI? What

is its leverage-adjusted modified duration gap?

(b) According to the duration model, what would the market value of equity

be for a 10 basis points decrease in the yield?

1

(c) 10 immunize itself from interest rate risk, the FI plans to restructure its

asset bond by adjusting its face value and coupon rate, while keeping the

bond's value (and hence the market value of asset), maturity and yield

unchanged. What should be the new face value and coupon rate? (Hint:

Write out and solve two equations, one for matching the market value of

assets before and after the restructuring, and the other for eliminating the

leverage-adjusted modified duration gap after the restructuring.)

(d) Assume the immunization in (c) is successfully implemented. Immediately

after the implementation, the yields of both bonds decrease from 4% to

3.9%. What are the market values of asset, liability and equity now?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- 88 MULTIPLE CHOICE Question 4 Listen A swim club is interested in its members' swim times for each distance. The data analysts gathered data and plotted it on a scatterplot with the x-axis represent- ing the distance swam and the y-axis representing the swim time. A linear re- gression was used to model the data where r=0.83. What is the value and interpretation of r²? Hint: Calculate r2 by squaring the r value. The explanatory variable is on the x-axis. The response variable is on the y-axis. Interpret r² as: About percent of the variation in the response variable can be ex- plained by the explanatory variable. A r²=0.9110 About 91.1% of the variation in the change of swim time can be ex- plained by the distance swam. B r²=0.6889 About 68.89% of the variation in the change of swim time can be explained by the distance swam. C r²=0.6889 About 68.89% of the variation in the change of the distance swam can be explained by the swim time. Pointsarrow_forwardQUESTION 2 S = 48 X = 50 C=$4 P = $3 A straddle requires purchasing one call and one put on the same asset with the same strike price. For this data the payoff for a straddle is a. $2 O b.-$1 Oc. $0 O d.-$7 O e. -$5arrow_forwardplease answer in text form and in proper format answer with must explanation , calculation for each part and steps clearlyarrow_forward

- Vijayarrow_forwardX Cut LB Copy Format Painter Clipboard 1 Calibri 11 V Font Α Α΄ BIU A V Conditional Format as Cell Formatting Table Styles ✓ Styles Alignment 3. A bank offers to pay you a stated annual rate of 5%, compounded daily. How many years will it take you to double your money in this acc Wrap Text Merge & Center S General S $%9588-00 Number 4 ← V Insert A 1. You plan to invest $1,000 today in an investment that you expect will earn a stated annual rate of 9% compounded semi-annually. How much will your investment be worth in 10 years? ato of 5% compounded daily. How many years will it take you to double warrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education