FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

Do not give image format

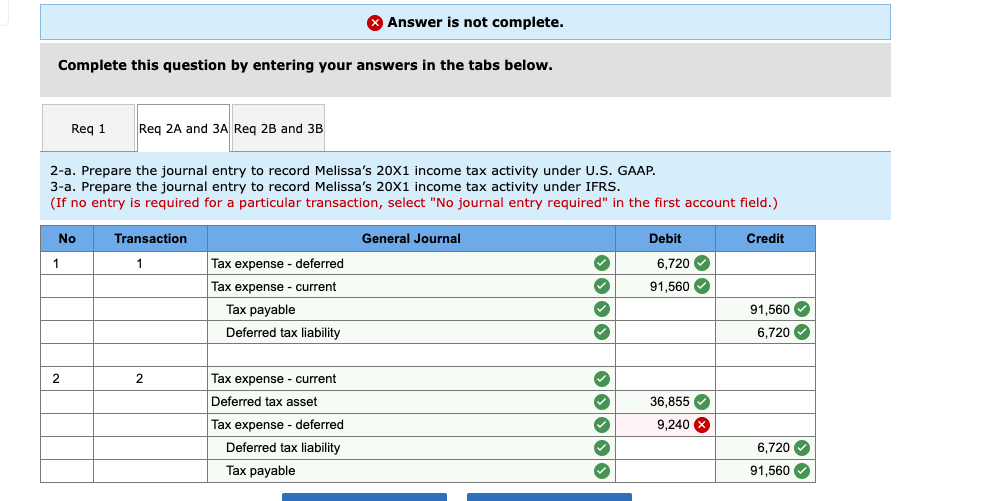

Transcribed Image Text:Complete this question by entering your answers in the tabs below.

Req 1

No

1

2-a. Prepare the journal entry to record Melissa's 20X1 income tax activity under U.S. GAAP.

3-a. Prepare the journal entry to record Melissa's 20X1 income tax activity under IFRS.

(If no entry is required for a particular transaction, select "No journal entry required" in the first account field.)

2

Req 2A and 3A Req 2B and 3B

Transaction

1

2

Answer is not complete.

Tax expense - deferred

Tax expense - current

Tax payable

Deferred tax liability

Tax expense - current

Deferred tax asset

Tax expense - deferred

Deferred tax liability

Tax payable

General Journal

✓

✓

✓

✓

Debit

6,720✔

91,560

36,855✔

9,240 X

Credit

91,560

6,720✔

6,720✔

91,560

Transcribed Image Text:Melissa Corporation is domiciled in Germany and is listed on both the Frankfurt and New York Stock Exchanges. Melissa has chosen to

prepare consolidated financial statements in accordance with U.S. GAAP for filing with the U.S. Securities and Exchange Commission

but must also prepare consolidated financial statements in accordance with IFRS in accordance with European Union regulations.

On December 31, 20X0, Melissa Corporation purchased a small office building for $1,380,000. For tax and financial reporting

purposes, Melissa estimates that the building has a useful life of 40 years with an estimated residual value of $100,000. Melissa uses

straight-line depreciation for financial reporting. Assume that, for tax purposes, Melissa is permitted to deduct 5% of an asset's

depreciable base in 20X1. This is the only building that Melissa owns.

At the end of 20X1, Melissa had the building appraised by a qualified real estate appraiser, who estimated the fair value of the building

to be $1,172,500. Melissa intends to occupy the building itself, and, therefore, the building is classified as property, plant, and

equipment under both U.S. GAAP and IFRS. After being revalued under IFRS, the Building account has a balance of $1,172,500 and the

Accumulated depreciation account has a balance of zero. Assume Melissa will have sufficient income in the future to recover any

deferred tax assets that might be recognized.

Model used for subsequent measurement

Pre-tax income before depreciation and revaluation charge

Enacted tax rate

U.S. GAAP

Cost

$500,000

21%

Required:

1. Calculate Melissa's taxable income in 20X1.

2. Prepare the journal entry to record Melissa's 20X1 income tax activity under U.S. GAAP.

3. Prepare the journal entry to record Melissa's 20X1 income tax activity under IFRS.

IFRS

Revalued at

fair value

$500,000

21%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education