Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Q15

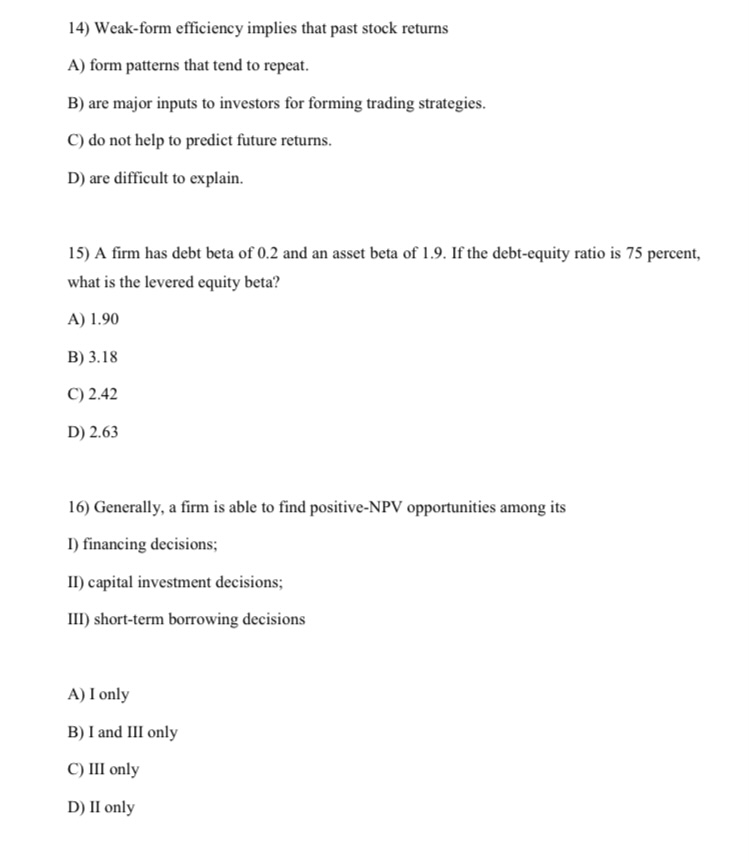

Transcribed Image Text:14) Weak-form efficiency implies that past stock returns

A) form patterns that tend to repeat.

B) are major inputs to investors for forming trading strategies.

C) do not help to predict future returns.

D) are difficult to explain.

15) A firm has debt beta of 0.2 and an asset beta of 1.9. If the debt-equity ratio is 75 percent,

what is the levered equity beta?

A) 1.90

B) 3.18

C) 2.42

D) 2.63

16) Generally, a firm is able to find positive-NPV opportunities among its

I) financing decisions;

II) capital investment decisions;

III) short-term borrowing decisions

A) I only

B) I and III only

C) III only

D) II only

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You want to estimate the cost of equity of firm A using CAPM. Firm A has a beta of 1.3. Assume that the return on the market portfolio is 8.52%, and the risk-free rate is 3%. What is the cost of equity of firm A? Group of answer choices There is not enough information to answer this question. 10.17% 11.74% 14.21% 12.11%arrow_forwardWhen estimating the cost of equity by use of the CAPM, three potential problems are (1) whether to use long-term or short-term rates for rRF, (2) whether or not the historical beta is the beta that investors use when evaluating the stock, and (3) how to measure the market risk premium, RPM. These problems leave us unsure of the true value of rs. a. true b. falsearrow_forwardWhich of the following is NOT a potential problem when estimating and using betas, i.e., which statement is FALSE? a. Sometimes, during a period when the company is undergoing a change such as toward more leverage or riskier assets, the calculated beta will be drastically different from the "true" or "expected future" beta. b. The beta of an "average stock," or "the market," can change over time, sometimes drastically. c. Sometimes the past data used to calculate beta do not reflect the likely risk of the firm for the future because conditions have changed. d. All of the statements above are true. e. The fact that a security or project may not have a past history that can be used as the basis for calculating beta.arrow_forward

- Can you show how this is donearrow_forwardAssume a firm has a beta of 1.2. All else held constant, the cost of equity for this firm will increase if the: A.beta decreases. B.decreases as the beta of the firm's stock increases C.either the risk-free rate or the market rate of return decreases. D.must equal the market rate of returnarrow_forwardCan you please solve these accounting question?arrow_forward

- 1. If a company has a Beta = 1.7, this stock is riskier than the S&P 500 index. That means its price fluctuates more than the market average. We can also say that the company’s stock price is more volatile than average. What’s good about a Beta > 1 and what’s bad about it? 2. T or F? Higher risk investments give the investor a higher return. If this is true, why don’t we all invest in the riskiest investments we can find? What’s the difference between fundamental analysis and technical analysis? Don’t simply define them both. Figure out what’s different. 3. If the value > price, then BUY according to value investors If the value < price, the DON’T BUY or maybe sell or hold according to value investors Would “momentum” investors say Buy or Don’t Buy? What would “income investors” want to know in order to make a BUY decision?arrow_forwardQ1. A price weighted index places more weight on stocks with a higher price, whilst a value weighted index places more weight on stocks with a higher market capitalization. Discuss. Q2. Price weighted indices have been criticized because they introduce a downward bias by reducing the weight of growing companies whose stock split. What does this mean and why does the underweighting occur? Q3. What should be the risk premium and return on a stock with a Beta of zero under the Capital Asset Pricing Model (CAPM)? What about the risk premium and return on a stock with a Beta of 1? Q4. In a world of certainty, investors will always invest in the asset with the highest return. In the real world, investors hold a diversified portfolio of securities. Why is this the case?arrow_forwardWhich statement is NOT correct? The distribution of returns does not affect the expected average rate of return. To find the dividend yield, we can subtract the capital gain yield from the total stock return. Average geometric return is a better indicator than the average arithmetic return for the growth. Wider the distribution of return, riskier is the investment. The current risk premium for U.S. Treasury bills is 0%.arrow_forward

- Which of the following statements is true? A. Because of flotation costs, dollars raised by retaining earnings must work harder than dollars raised by selling new shares. B. All other things being equal, a call option price will increase, and a put option price will decrease if an exercise price increases. C. Security market line (SML) plots return against total risk which is measured by the standard deviation of returns. D. Because potential long-term returns, income from rent-payments, diversification, and inflation hedge, real-estate would be a good investment.arrow_forwardPlease correct answer and don't use hand raitingarrow_forwardPlease do a and b separate (Question 2) a) Plot the Security Market Line (SML)b) Superimpose the CAPM’s required return on the SMLc) Indicate which investments will plot on, above and below the SML? d) If an investment’s expected return (mean return) does not plot on the SML, what doesit show? Identify undervalued/overvalued investments from the graph.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education