FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

TRUE OR FALSE

Please answer all.

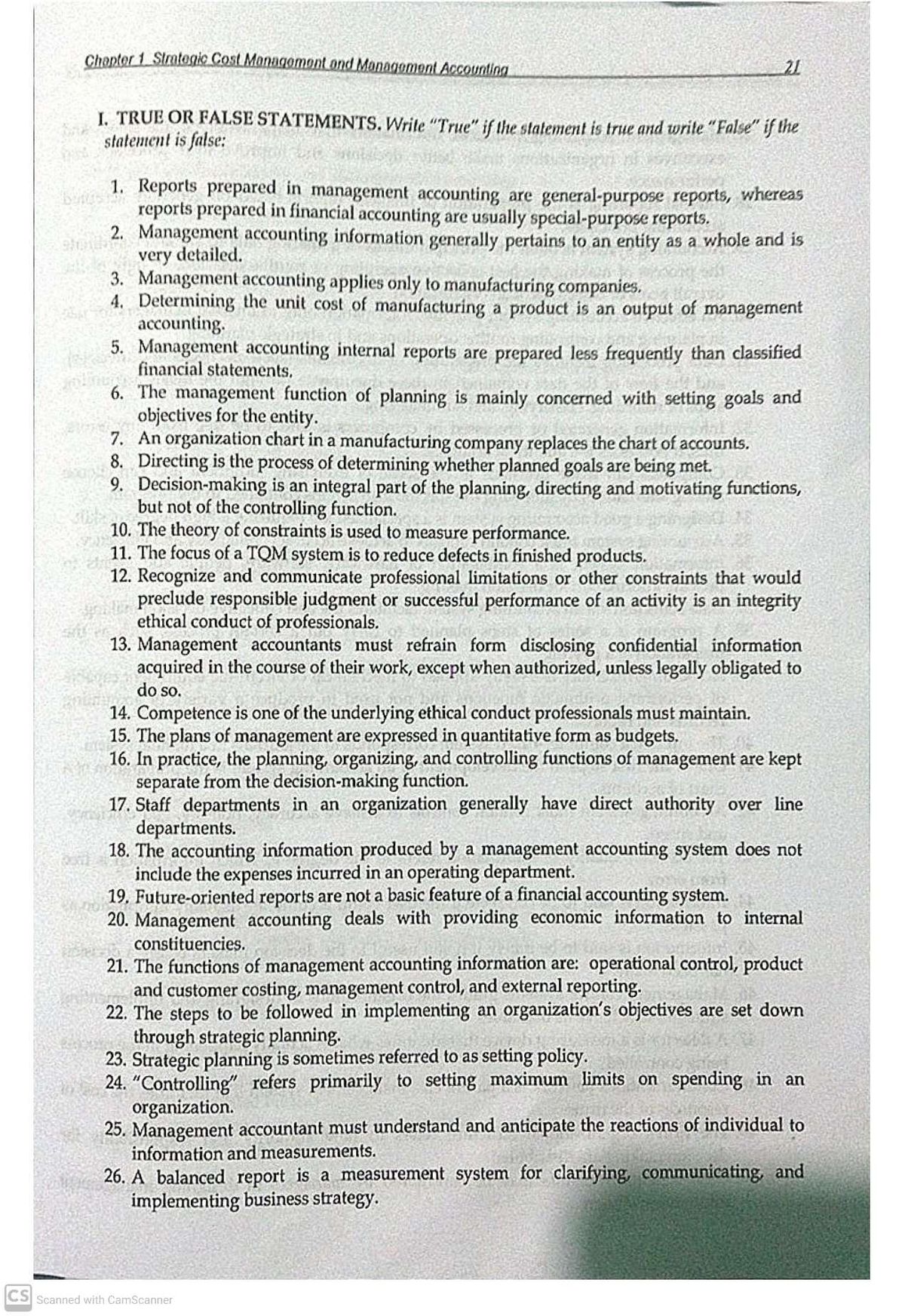

Transcribed Image Text:Chapter 1 Stratogic Cost Managomont ond Monagoment Accounting

21

I. TRUE OR FALSE STATEMENTS. Write "True" if the statement is true and write "False" if the

statement is false:

1. Reports prepared in management accounting are general-purpose reports, whereas

reports prepared in financial accounting are usually special-purpose reports.

2. Management accounting information generally pertains to an entity as a whole and is

very detailed.

3. Management accounting applies only to manufacturing companies.

4. Determining the unit cost of manufacturing a product is an output of management

accounting.

5. Management accounting internal reports are prepared less frequently than classified

financial statements.

6. The management function of planning is mainly concerned with setting goals and

objectives for the entity.

7. An organization chart in a manufacturing company replaces the chart of accounts.

8. Directing is the process of determining whether planned goals are being met.

9. Decision-making is an integral part of the planning, directing and motivating functions,

but not of the controlling function.

10. The theory of constraints is used to measure performance.

11. The focus of a TQM system is to reduce defects in finished products.

12. Recognize and communicate professional limitations or other constraints that would

preclude responsible judgment or successful performance of an activity is an integrity

ethical conduct of professionals.

13. Management accountants must refrain form disclosing confidential information

acquired in the course of their work, except when authorized, unless legally obligated to

do so.

14. Competence is one of the underlying ethical conduct professionals must maintain.

15. The plans of management are expressed in quantitative form as budgets.

16. In practice, the planning, organizing, and controlling functions of management are kept

separate from the decision-making function.

17. Staff departments in an organization generally have direct authority over line

departments.

18. The accounting information produced by a management accounting system does not

include the expenses incurred in an operating department.

19. Future-oriented reports are not a basic feature of a financial accounting system.

20. Management accounting deals with providing economic information to internal

constituencies.

21. The functions of management accounting information are: operational control, product

and customer costing, management control, and external reporting.

22. The steps to be followed in implementing an organization's objectives are set down

through strategic planning.

23. Strategic planning is sometimes referred to as setting policy.

24. "Controlling" refers primarily to setting maximum limits on spending in an

organization.

25. Management accountant must understand and anticipate the reactions of individual to

information and measurements.

26. A balanced report is a measurement system for clarifying, communicating and

implementing business strategy.

CS Scanned with CamScanner

Transcribed Image Text:Chacter tStroteak Cost Meneaement.and Menment Accoutog

27. Management accounting produces information that helps workers, manager, and

executives in organizations make better decisions and improve their processes and

performance.

28. Internal reporting is the preparation of financial reports based on generally accepted

accounting principles

29. Accounting system is often the principal means of gathering data to aid and coordinate

the process of making the best collective operating or routine decisions in light of the

overall goals or objectives of an organiration.

30. An effective accounting system provides information only to internal managers for use

in planning and controlling routine operations and in strategic planning.

31. Data processing includes the preparation of documents (such as checks and invoices),

and the flow of the data contained in these documents through the major accounting

steps of recording, classifying, and summarizing.

32. Information generated or processed by computers is said to be free from any errors,

thus, it possesses the quality of accuracy.

33. Computers can make decisions in the sense of exercising judgment and can choose

among alternatives by following the specific instructions contained in the program.

34. Designing a good accounting system is a specialized job requiring a high degree of skill.

35. Accounting system must contain controls to achieve accuracy, reliability and efficiency.

36. Information system is

provide information for decision making.

37. Data collection via an accounting system facilitates the best collective decision making.

38. A program is a series of steps planned to carry out a certain process, such as the

preparation of a payroll.

39. Accounting machines is usually applied to mechanical or electronic equipment capable

of performing arithmetic functions and not used to produce a variety of accounting

records and reports.

40. The input in a computer-based system corresponds to the journals in a manual system.

41. One of the first steps in the development of an accounting system is the preparation of a

chart of accounts.

42. Accounting system must contain controls to achieve accuracy, honesty, and efficiency,

and speed.

43. The accuracy quality of information refers to the degree to which information is free

from error.

44. Information is said to be complete if the user could accumulate as many information as

possible.

45. Information is said to be timely if it still useful to the decision makers before a decision

has been made.

combination of hardware, software, people and events to

46. Management control systems guides the organizations in designing and implementing

strategies to achieve its objectives

47. A detector is a measuring device that identifies what is actually happening in the

being controlled.

48. Communications network is a part of cost management system that identifies the cost of

process

resources of the firms.

a fo 49. The firm's organizational structure refers to how authority and responsibility for

decision making are distributed.

50. Costs-benefits trade-offs may be considered by managers in designing management

information system.

CS Scanned with CamScanner

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Zina Manufacturing Company started and completed Job 501 in December with the following Job Cost Sheet and transferred it to the warehouse. Direct Materials Date Dec 17 Dec 30 Total Direct Labor Amount Date Amount $2,000 Dec 20 $4,000 8,000 Dec 30 3,800 Total Job Cost Sheet - Job No. 501 Total Cost The journal entry to record the transaction is A) WIP Inventory FG Inventory B) Cost of Goods Sold WIP Inventory C) FG Inventory WIP Inventory D) FG Inventory WIP Inventory Debit Credit 35,800 17,800 17,800 Manufacturing Overhead Date Amount Dec 24 $10,000 Dec 30 8,000 Total 35,800 35,800 17,800 17,800 35,800arrow_forwardHh1.arrow_forwardStill need answers and details for B and C?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education