ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

1. Answer the following questions:

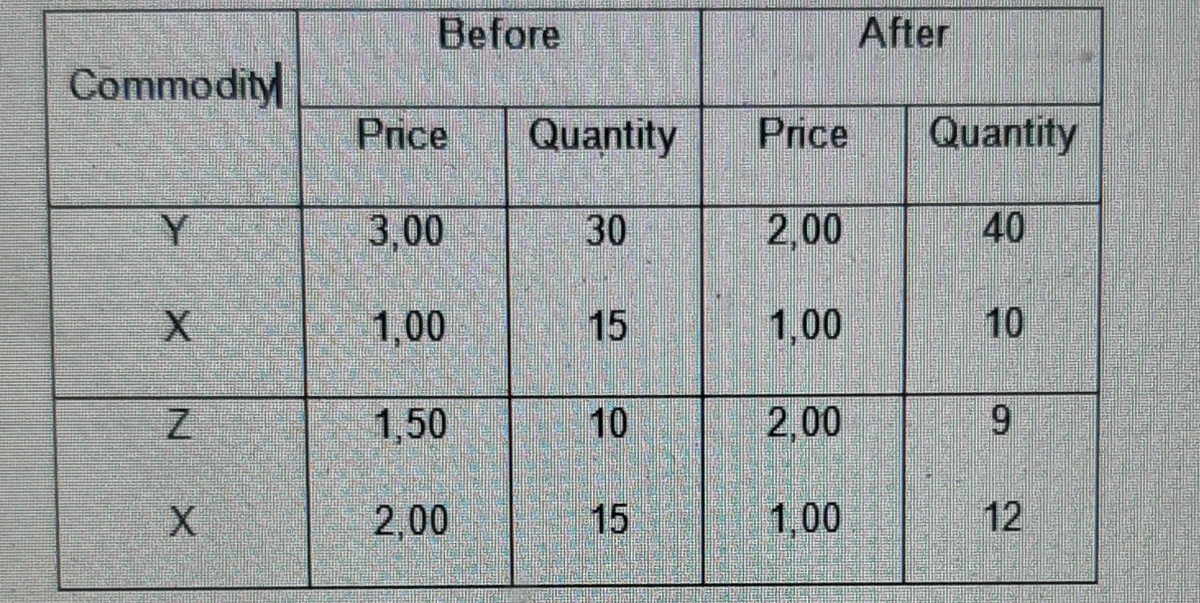

a. Find the cross elasticity of demand between X and Y, and X and Z with the following data:(in the image)

b. Are these commodities substitution or complementary?

Transcribed Image Text:Before

After

Commodity

Price

Quantity

Price

Quantity

Y.

3,00

30

2,00

40

1,00

15

1,00

1,50

10

2,00

2,00

15

1,00

12

10

9,

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Timmy is selling his toy dinos again. The consumer demand curve for thedinos is given by: x=(50-3p)^2 where p is the price per dino, and x is the demand in weekly sales. a.) Find the Elasticity of Demand function E(p) and evaluate it at the price p = $5.Is the demand elastic, inelastic, or does it have unit elasticity? Explain what this means inyour own words. b.) Find the price Timmy needs to charge for his dinos in order to maximize revenue.(Round your answer to the nearest cent.)arrow_forwardIf Good C increases in price by 3030% a pound, and this causes the quantity demanded for Good D to increase by 40%40%, what is the cross-price elasticity of the two goods? Round your answer to one decimal place.arrow_forwardIn a study of the demand for automobiles in Canada, economists Blomqvist and Hassel distinguished between large and small cars and estimated the price and cross- price elasticities as well as the effects of the price of gasoline on the demands for small and large cars. Their results were as follows: a. C. New large cars New small cars d. Own price elasticity 1.26 2.30 Cross price elasticity 0.86 1.73 Elasticity with respect to gasoline price Note: The cross-price elasticities show that the demand for new small cars is more responsive to changes in the price of new large cars than the demand for new large cars is to changes in the price of new small cars. Do the cross-price elasticities have the expected sign? Briefly explain. b. If the price of new small cars went up by, say, 5 percent, by what percentage would new small car purchases change? {Note: In your answer to this and all of the remaining parts of this question, please indicate whether the change is an increase or a decrease.}…arrow_forward

- Does this imply that ice cream and frozen yogurt are complements or substitutes and does that answer match your intuition for whether or not ice cream and frozen yogurt are complements or substitutes? If not, how can you account for the value of the cross price elasticity implied by the data?arrow_forwardalso with the questions in the picture : good 1 and 2 can be described as what : substitutes, elastic goods, unit elastic goods, inferior goods, complements, normal goods, inelastic goods. More than one answer is rightarrow_forwardAssume the market demand for tuna cans may be written as Qtc = 45 - 2 x Ptc + Psc+ 0.3y (where Ptc = price of tuna cans and Psc = price of sardine cans, and y = income). Further assume that both tuna cans and sardine cans sell for $1 and income is $25. Calculate cross - price elasticity for tuna cans and identify whether the goods are substitutes or complements.arrow_forward

- 1. Consider the market for Widgets. Suppose that the equation for the supply curve is: Qs = 1,000P – 10,000, and the equation for the demand curve is: Qa = 50,000 – 2,000P. It turns out that the equilibrium price is 20, while the equilibrium quantity is 10,000. a. Use a 10% increase in quantity to estimate (crudely) both the elasticity of supply and the elasticity of demand at the equilibrium quantity. i) Categorize supply and demand as elastic or inelastic at the equilibrium quantity. ii) Is supply or demand relatively more inelastic at the equilibrium quantity? b. If the government enacted a tax of $3, the loss in consumer surplus would be 9,000, while the loss in producer surplus would be 18,000 (see Homework 2, question #2.) Compare this information to your answer to part (a). Explain. c. Now estimate (crudely) the elasticity of demand at a quantity of 11,000 by decreasing quantity by 1,000. Compare your estimate of elasticity to the estimate in part (a). Comment.arrow_forwardFor each statement below, tell whether the statement is valid or invalid, and give a short explanation of your answer. Remember that your explanation will be related in some way to elasticity. 1. Coffee and tea should have a positive cross elasticity of demand. 2. Demand for Tide will be more elastic than demand for laundry detergents as a whole. 3. The government will prefer to put excise taxes on jewelry rather than on gasoline.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education