Related questions

Concept explainers

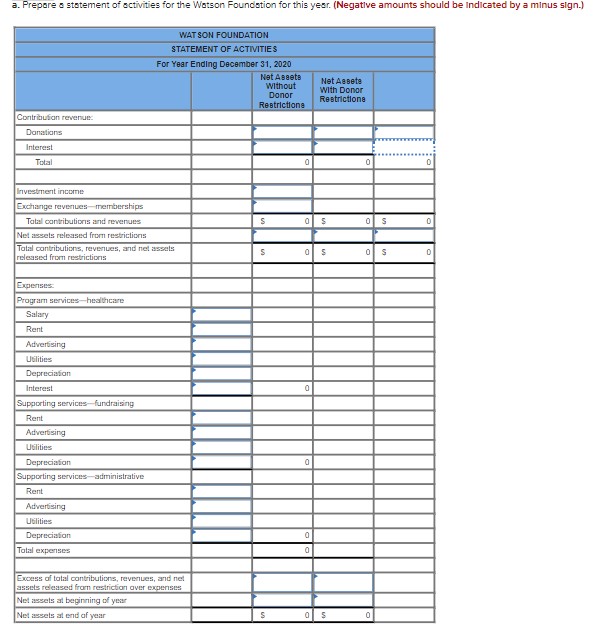

The Watson Foundation, a private not-for-profit entity, starts 2020 with cash of $100,000, contributions receivable (net) of $200,000, investments of $300,000, and land, buildings, and equipment (net) of $200,000. Net assets without donor restrictions were reported as $400,000, the same figure as the net assets with donor restrictions. Of the restricted net assets, $300,000 was purpose restricted whereas the other $100,000 had to be held permanently, although the subsequently earned income is without restriction. Fifty percent of the purpose restricted net assets had to be used to help pay for a new building. The remainder was restricted to the payment of officer salaries. Donors made no stipulations about the eventual reporting of buildings and other long-lived assets when acquired. Watson has one program service (health care) and two supporting services (fundraising and administrative).

During the current year, Watson Foundation has the following transactions.

- Computed interest of $20,000 on the unrestricted contribution receivable.

- Received cash of $100,000 from the contributions receivable and wrote off another $4,000 as uncollectible.

- Received unrestricted cash donations of $180,000.

- Received $23,000 in cash that must be spent for a particular type of office machine within the next year or the money must be returned.

- Paid salaries of $90,000. Of that amount, $19,000 came from restricted funds. The payment was made to individuals doing health care work.

- Spent the $23,000 in (4) for the appropriate office machine.

- Received a cash gift of $12,000 that Watson must convey to another specified charity. However, Watson has the right to give this money to a different organization if officials so choose.

- Bought a building for $500,000 by signing a long-term note for $450,000 and using restricted funds for the remainder.

- Collected annual membership dues of $30,000. Individuals receive substantial benefits from their memberships. By the end of the year, two-thirds of the time for the average membership has passed.

- Received unrestricted income of $44,000 generated by net assets that must be held permanently.

- The board of directors of the Watson Foundation vote to set aside $9,000 of its investments for emergency purposes.

- Paid rent of $12,000 for the past month, advertising of $15,000, and utilities of $16,000. These were half for the program service and one-fourth each for the two supporting services.

- Received an unrestricted pledge of $200,000. Watson will collect the money in five years and does not expect any part to be uncollectible. Present value at inception is $149,000, but interest for the year to date is $6,000.

- Computed

depreciation of $40,000, 60 percent for health care, 30 percent for administrative, and 10 percent for fundraising. - Paid $15,000 in interest on the note signed in (8). All of this cost is assumed to be related to health care.

Required:

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

- N2. Accountarrow_forwardAt the end of 2015, Learning Tree, a not-for-profit organization, received a $5 million contribution (fair value), consisting entirely of investment securities. The contribution is required to be used to establish a permanent endowment, the income from which must be used exclusively to provide free “chapter books” to elementary school children. The endowment specifies that both realized and unrealized gains may be used for this purpose in addition to investment income. Learning Tree applies FASB accounting standards for not-for-profit organizations. At the start of 2016, Learning Tree had $600,000 in unrestricted net assets. During 2016, the endowment earns $100,000 in dividends and interest. Learning Tree spends the entire amount on books and distribution costs. At year-end, the value of the endowment portfolio is $5.5 million. During 2017, the endowment earns $100,000 in dividends and interest. The entire amount is spent on books. At year-end, the fair value of the endowment…arrow_forwardAssume that the City of Coyote has produced its financial statements for December 31, 2020, and the year then ended. The city's general fund was only used to monitor education and parks. Its capital projects funds worked in connection with each of these functions at times during the current year. The city also maintained an enterprise fund to account for its art museum. The government-wide financial statements provide the following figures: • Education reports net expenses of $742,000. • Parks reports net expenses of $140,000. • Art museum reports net revenues of $73,250. • General government revenues for the year were $987,750 with an overall increase in the city's net position of $179,000. The fund financial statements provide the following for the entire year: • The general fund reports a $52,250 increase in its fund balance. • The capital projects fund reports a $62,500 increase in its fund balance. • The enterprise fund reports a $73,500 increase in its net position. The city asks…arrow_forward

- At the beginning of the year, the Baker Fund,a nongovernmental not-for-profit corporation,received a $125,000 contribution restrictedto youth activity programs. During the year,youth activities generated revenues of$89,000 and had program expenses of$95,000. What amount should Baker reportas net assets released from restrictions forthe current year?arrow_forwardSnow Inc., a calendar year, accrual basis corporation, wants to make a $20,000 donation to the Wild Bird Sanctuary, a qualified charitable organization, but does not have adequate funds to make the contribution in 2023. On December 28, 2023, Snow's board of directors authorizes a $20,000 contribution to the Wild Bird Sanctuary. The donation is made on April 10, 2024. Based on these facts: a. Snow's 2023 income is reduced by $10,000 and Snow's 2024 income is reduced by $10,000. b. Snow gets no tax benefit in either 2023 or 2024 for the charitable contribution. c. Snow must pay $4,200 in Federal income taxes in 2023. d. Snow must deduct the $20,000 contribution in 2024, the year of the payment. e. Snow defers payment of $4,200 in Federal income taxes in 2023.arrow_forwardScofield City received a donation from the estate of the late Lisa O’Reilly to be used to support the city’s public library. The gift consisted of $200,000 cash and a portfolio of securities with a market value of $350,000. The securities have a book value of $250,000. The donor stipulated that the principal of the gift, including investment gains (realized and unrealized) but excluding investment losses, must be kept intact. The income must be used to care for and maintain the book collection at the newly renamed O’Reilly Public Library. All appropriate costs, including investment losses, may be charged against the revenues yearly to determine the amount available for the specified purposes. During the year, the city engaged in the following transactions on behalf of the library. Prepare the appropriate entries in the city’s permanent fund. a) Accepted the donation. b) Received dividends and interest of $18,000. c) Purchased securities for $200,000. d) Sold securities that were part…arrow_forward

- 10-15. Jefferson Animal Rescue is a private not-for-profit clinic and shelter for abandoned domesticated animals, chiefly dogs and cats. At the end of 2019, the organization had the following account balances: [See attached image] The following took place during 2020: 1. Additional supplies were purchased on account in the amount of $16,050.2. Unconditional (and unrestricted) pledges of support were received totaling $95,000. In light of a declining economy, 4 percent is expected to be uncollectible. The remainder is expected to be collected in the current year.3. Supplies used for animal care amounted to $17,200.4. Payments made on accounts payable amounted to $17,100.5. Cash collected from pledges totaled $90,500.6. Salaries were paid in the amount $47,500. Included in this amount is the accrued wages payable at the end of 2019. (The portion of wages expense attributable to administrative expense is $15,000 and fund-raising expense is $2,000. The remainder is for animal care.)7.…arrow_forwardThe following selected transactions occurred for a nongovernmental, not-for-profit organization. 1. Received a contribution of stock to establish an endowment fund. The income from the endowment is unrestricted. The donor had acquired the stock for $23 about 20 years earlier. Its estimated fair value when donated was $250. 2. Pledges receivable at year end were $100, all from pledges received during the year. The pledges are unrestricted and 5% of the pledges are estimated to be uncollectible. The pledges expect to be collected early next year. For questions 3-5, assume that the organization has adopted a policy that restrictions on donations made for capital purposes are met when the capital item is purchased. A cash gift of $200 was received restricted for the purchase of equipment. Equipment of $80 was purchased from the gift restricted for this purpose. Depreciation expense for the year on the equipment purchased is $10. Required: Prepare the journal entries for the above…arrow_forwardEarly in 2018, a not-forprofit organization received a $4,000,000 gift from a wealthy benefactor. This benefactor specified that the gift be invested in perpetuity with income restricted to provide speaker fees for a lecture series named for the benefactor. The not-for-profit is permitted to choose suitable investments and is responsible for all other costs associated with initiating and administering this series.Neither the donor’s stipulation nor the law addresses gains and losses on this permanent endowment. In 2018, the investments purchased with the gift earned $100,000 in dividend income. The fair value of the investments increased by $300,000. The not-for-profit’s accounting policy is to record increases in net assets, for which a donor-imposed restriction is met in the same accounting period as gains and investment income are recognized, as increases in unrestricted net assets.Five presentations in the lecture series were held in 2018. The speaker fees for the five…arrow_forward

- Assume that Saint Clair Nature Center, a private not-for-profit organization, started the fiscal year beginning January 1, 2013, with $205,000 in temporarily restricted net assets. The amounts are restricted for the following: (1) restricted for educational programs relating to preservation of wetlands: $25,000; (2) restricted for future building expansion: $145,000, and (3) restricted for use in future years including long-term pledges: $35,000. A)Expenses related to educational programs on preservation of wetlands were incurred and paid in the amount of $23,000. - 2 entries B)Equipment for use in Center’s routine activities was donated on July 1, 2013. The equipment had a historical cost to the donor of $100,000 and accumulated depreciation to date of $75,000. It’s current value is $30,000 and it has a 3-year remaining useful life. Include entry for depreciation (assuming straight line). - 2 entries C)Saint Clair Nature Center receives a gift of $5,000 to acquire the Zeron 5000, a…arrow_forwardIn 2022, OCC Corporation made a charitable donation of $400,000 to the International Rescue Committee (a qualifying charity). For the year, OCC reported taxable income of $1,500,000 before deducting any charitable contributions, before deducting its $20,000 dividends-received deduction, and before deducting its $40,000 NOL carryover from last year. Required: a. What amount of the $400,000 donation is OCC allowed to deduct for tax purposes in 2022, what is the carryover to 2023, and when does the carryover expire? b. Assume that in 2023, OCC did not make any charitable donations and that it is allowed to deduct its full charitable contribution carryover, if any, from 2022. What book-tax difference associated with the charitable contributions will OCC report in 2023? Is the difference favorable or unfavorable? Is it permanent or temporary? Answer is complete but not entirely correct. Complete this question by entering your answers in the tabs below. Required A Required B What amount of…arrow_forwardFruits & Veggies, a nonprofit, conducts two types of programs: education and research. It does not use fund accounting. During the fiscal year, the following transactions and events took place. Prepare journal entries for these transactions, identifying increases and decreases by net asset classification as appropriate. 1. Pledges amounting to amount pledged. $180,000 were received, to be used for any purpose designated by the trustees. Fruits & Veggies normally collects 90 percent of the amount pledged.2. Fruits & Veggies collected $171,000 in cash on the amount pledged in the previous transaction. It wrote off the balance as uncollectible.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education