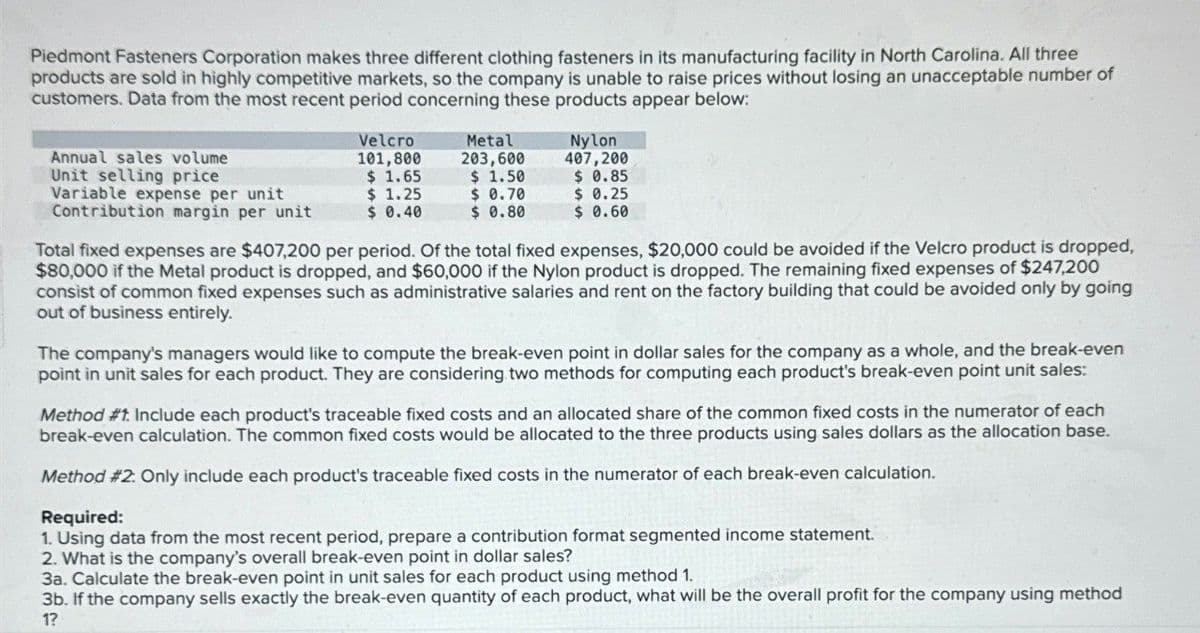

Piedmont Fasteners Corporation makes three different clothing fasteners in its manufacturing facility in North Carolina. All three products are sold in highly competitive markets, so the company is unable to raise prices without losing an unacceptable number of customers. Data from the most recent period concerning these products appear below: Annual sales volume Velcro 101,800 Metal 203,600 Nylon 407,200 Unit selling price $ 1.65 $ 1.50 $ 0.85 Variable expense per unit $ 1.25 $ 0.70 Contribution margin per unit $ 0.40 $ 0.80 $ 0.25 $ 0.60 Total fixed expenses are $407,200 per period. Of the total fixed expenses, $20,000 could be avoided if the Velcro product is dropped, $80,000 if the Metal product is dropped, and $60,000 if the Nylon product is dropped. The remaining fixed expenses of $247,200 consist of common fixed expenses such as administrative salaries and rent on the factory building that could be avoided only by going out of business entirely. The company's managers would like to compute the break-even point in dollar sales for the company as a whole, and the break-even point in unit sales for each product. They are considering two methods for computing each product's break-even point unit sales: Method #1. Include each product's traceable fixed costs and an allocated share of the common fixed costs in the numerator of each break-even calculation. The common fixed costs would be allocated to the three products using sales dollars as the allocation base. Method #2: Only include each product's traceable fixed costs in the numerator of each break-even calculation. Required: 1. Using data from the most recent period, prepare a contribution format segmented income statement. 2. What is the company's overall break-even point in dollar sales? 3a. Calculate the break-even point in unit sales for each product using method 1. 3b. If the company sells exactly the break-even quantity of each product, what will be the overall profit for the company using method 1?

Piedmont Fasteners Corporation makes three different clothing fasteners in its manufacturing facility in North Carolina. All three products are sold in highly competitive markets, so the company is unable to raise prices without losing an unacceptable number of customers. Data from the most recent period concerning these products appear below: Annual sales volume Velcro 101,800 Metal 203,600 Nylon 407,200 Unit selling price $ 1.65 $ 1.50 $ 0.85 Variable expense per unit $ 1.25 $ 0.70 Contribution margin per unit $ 0.40 $ 0.80 $ 0.25 $ 0.60 Total fixed expenses are $407,200 per period. Of the total fixed expenses, $20,000 could be avoided if the Velcro product is dropped, $80,000 if the Metal product is dropped, and $60,000 if the Nylon product is dropped. The remaining fixed expenses of $247,200 consist of common fixed expenses such as administrative salaries and rent on the factory building that could be avoided only by going out of business entirely. The company's managers would like to compute the break-even point in dollar sales for the company as a whole, and the break-even point in unit sales for each product. They are considering two methods for computing each product's break-even point unit sales: Method #1. Include each product's traceable fixed costs and an allocated share of the common fixed costs in the numerator of each break-even calculation. The common fixed costs would be allocated to the three products using sales dollars as the allocation base. Method #2: Only include each product's traceable fixed costs in the numerator of each break-even calculation. Required: 1. Using data from the most recent period, prepare a contribution format segmented income statement. 2. What is the company's overall break-even point in dollar sales? 3a. Calculate the break-even point in unit sales for each product using method 1. 3b. If the company sells exactly the break-even quantity of each product, what will be the overall profit for the company using method 1?

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter10: Decentralization: Responsibility Accounting, Performance Evaluation, And Transfer Pricing

Section: Chapter Questions

Problem 34P

Related questions

Question

Transcribed Image Text:Piedmont Fasteners Corporation makes three different clothing fasteners in its manufacturing facility in North Carolina. All three

products are sold in highly competitive markets, so the company is unable to raise prices without losing an unacceptable number of

customers. Data from the most recent period concerning these products appear below:

Annual sales volume

Velcro

101,800

Metal

203,600

Nylon

407,200

Unit selling price

$ 1.65

$ 1.50

$ 0.85

Variable expense per unit

$ 1.25

$ 0.70

Contribution margin per unit

$ 0.40

$ 0.80

$ 0.25

$ 0.60

Total fixed expenses are $407,200 per period. Of the total fixed expenses, $20,000 could be avoided if the Velcro product is dropped,

$80,000 if the Metal product is dropped, and $60,000 if the Nylon product is dropped. The remaining fixed expenses of $247,200

consist of common fixed expenses such as administrative salaries and rent on the factory building that could be avoided only by going

out of business entirely.

The company's managers would like to compute the break-even point in dollar sales for the company as a whole, and the break-even

point in unit sales for each product. They are considering two methods for computing each product's break-even point unit sales:

Method #1. Include each product's traceable fixed costs and an allocated share of the common fixed costs in the numerator of each

break-even calculation. The common fixed costs would be allocated to the three products using sales dollars as the allocation base.

Method #2: Only include each product's traceable fixed costs in the numerator of each break-even calculation.

Required:

1. Using data from the most recent period, prepare a contribution format segmented income statement.

2. What is the company's overall break-even point in dollar sales?

3a. Calculate the break-even point in unit sales for each product using method 1.

3b. If the company sells exactly the break-even quantity of each product, what will be the overall profit for the company using method

1?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 6 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT