Exercise 15-19 (LO. 3, 4) In 2020, Henry Jones works as a freelance driver, finding customers using various platforms like Uber and Grubhub. He is single and has no other sources of income. In 2020, Henry's qualified business income from driving is $61,200. Assume Henry takes the standard deduction of $12,400. Click here to access the 2020 individual tax rate schedule to use for this problem. Assume the QBI amount is net of the self-employment tax deduction. Compute Henry's QBI deduction and his tax liability for 2020. QBI deduction: $fill in the blank 1 Tax liability (round to the nearest dollar): $fill in the blank 2

Exercise 15-19 (LO. 3, 4) In 2020, Henry Jones works as a freelance driver, finding customers using various platforms like Uber and Grubhub. He is single and has no other sources of income. In 2020, Henry's qualified business income from driving is $61,200. Assume Henry takes the standard deduction of $12,400. Click here to access the 2020 individual tax rate schedule to use for this problem. Assume the QBI amount is net of the self-employment tax deduction. Compute Henry's QBI deduction and his tax liability for 2020. QBI deduction: $fill in the blank 1 Tax liability (round to the nearest dollar): $fill in the blank 2

Chapter24: Multistate Corporate Taxation

Section: Chapter Questions

Problem 26P

Related questions

Question

Exercise 15-19 (LO. 3, 4)

In 2020, Henry Jones works as a freelance driver, finding customers using various platforms like Uber and Grubhub. He is single and has no other sources of income. In 2020, Henry's qualified business income from driving is $61,200. Assume Henry takes the standard deduction of $12,400.

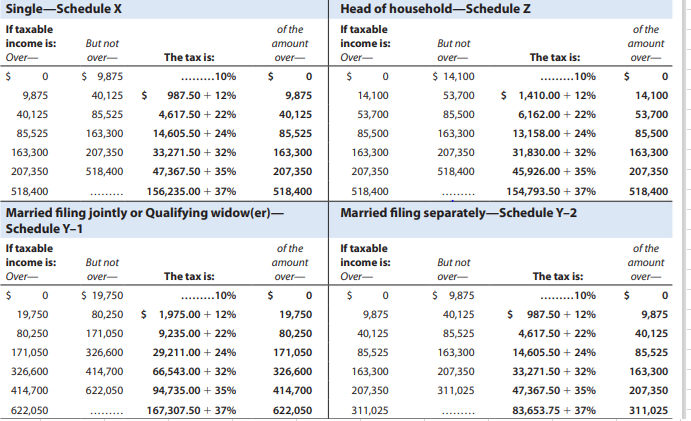

Click here to access the 2020 individual tax rate schedule to use for this problem.

Assume the QBI amount is net of the self-employment tax deduction.

Compute Henry's QBI deduction and his tax liability for 2020.

QBI deduction: $fill in the blank 1

Tax liability (round to the nearest dollar): $fill in the blank 2

Transcribed Image Text:Single-Schedule X

Head of household-Schedule Z

If taxable

of the

If taxable

of the

income is:

But not

аmount

income is:

But not

amount

Over-

over-

The tax is:

over-

Over-

over-

The tax is:

over-

$ 9,875

.........10%

$

$ 14,100

.....10%

9,875

40,125

$

987.50 + 12%

9,875

14,100

53,700

$ 1,410.00 + 12%

14,100

40,125

85,525

4,617.50 + 22%

40,125

53,700

85,500

6,162.00 + 22%

53,700

85,525

163,300

14,605.50 + 24%

85,525

85,500

163,300

13,158.00 + 24%

85,500

163,300

207,350

33,271.50 + 32%

163,300

163,300

207,350

31,830.00 + 32%

163,300

207,350

518,400

47,367.50 + 35%

207,350

207,350

518,400

45,926.00 + 35%

207,350

518,400

156,235.00 + 37%

518,400

518,400

154,793.50 + 37%

518,400

Married filing jointly or Qualifying widow(er)–

Schedule Y-1

Married filing separately-Schedule Y-2

If taxable

of the

If taxable

of the

income is:

But not

атount

income is:

But not

amount

Over-

over-

The tax is:

over-

Over-

over-

The tax is:

over-

$ 19,750

.... 10%

$

$ 9,875

.... 10%

19,750

80,250

$ 1,975.00 + 12%

19,750

9,875

40,125

987.50 + 12%

9,875

80,250

171,050

9,235.00 + 22%

80,250

40,125

85,525

4,617.50 + 22%

40,125

171,050

326,600

29,211.00 + 24%

171,050

85,525

163,300

14,605.50 + 24%

85,525

326,600

414,700

66,543.00 + 32%

326,600

163,300

207,350

33,271.50 + 32%

163,300

414,700

622,050

94,735.00 + 35%

414,700

207,350

311,025

47,367.50 + 35%

207,350

622,050

167,307.50 + 37%

622,050

311,025

83,653.75 + 37%

311,025

.........

.........

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT